- Mexico: Banxico keeps its monetary stance unchanged

- Peru: BCRP holds key rate for the seventh time and gives signs of start of rate cuts cycle

It was another quiet overnight session with Tokyo closed for holidays and little on the headlines or data front in APac, while in European hours the release of stronger-than-expected UK GDP was followed by very disappointing Chinese credit data after the local close; Chinese equity markets had their worst day since last October on concerns about property developers risking default.

USTs opened in European hours with a steady bid but some of the strength in rates markets is reversing in the past hour or so, where gilts are the worst performer (10s up 10bps) after a strong day yesterday and the GDP data weighing somewhat. SPX futures are unchanged to a touch lower, at writing.

The USD is mixed against the majors with the MXN at the top of the standings with a 0.4% gain that still leaves it around where it traded at this time on Thursday before a short-lived rally to the high-16s. Iron ore up 2% is benefitting from Chinese steel mills reopening after a summer break, while copper falls 1.3% and crude oil is up 0.3% through very choppy trading.

In Latam, today’s data highlights are Brazilian July IPCA data and Mexican industrial/manufacturing production data, all out at 8ET. The latter may not be a major market mover as the focus will remain on the interpretation of yesterday’s Banxico decision (see below) that sticks to guidance that cuts are still a ways away, this is in contrast to the BCRP’s announcement that suggests the bank may begin reference rate reductions (see below, as well).

Brazilian inflation is seen jumping from 3.2% to 4.0% y/y as an unfavourable comparison base kicks in. The BCB is already aware of this and so are economists, as headline inflation drifts towards 5% at year-end. BCB guidance points to three more 50bps cuts this year but if this acceleration in inflation turns out more pronounced it may think again for the December meeting. It’s important to note, however, that prices are projected to have only expanded by about 0.1% m/m last month, a rather low reading for a July month.

Economic activity is not looking great (see miss in services volume yesterday) and the BCB’s real policy rate is still around double digits, so the bank still has a motivation to move at a fast pace. On that front, President Lula and FinMin Haddad speak at 9ET to present details of the PAC (Growth Accelerating Program) that will focus on public infrastructure spending, and the BCB’s Campos Neto speaks at a couple of industry events.

Elsewhere, global markets will focus on US PPI and U Mich consumer survey data at 8.30ET and 10ET, respectively. We may also get some provocative comments from Colombia’s President Petro at an appearance at a Constitutional Court hearing (that starts at 9ET) to defend his social and economic emergency declaration for La Guajira province due to elevated poverty and food insecurity.

—Juan Manuel Herrera

MEXICO: BANXICO KEEPS ITS MONETARY STANCE UNCHANGED

As expected, Banxico held its overnight rate at 11.25% for the third consecutive time in a unanimous decision. Banxico still thinks that the current monetary stance is adequate to reach the inflation target in Q4-23, so the tone of the statement was practically unchanged compared to the last decision.

However, despite the fact that they highlighted that the non-core component is at historically low levels and revised their headline inflation forecasts slightly lower, there were upward revisions to the core inflation forecast (table 1).

Likewise, they highlight that the balance of risks for inflation continues to be biased upwards, for which reason the development of the data will dictate the measures to be taken, bearing in mind that the economic slowdown will not be as pronounced as was forecast a few months ago. Additionally, the board emphasizes that it will be necessary to maintain the rate at a restrictive level for a considerable time. Given the above, we anticipate that the board will keep its monetary policy rate steady until the December decision, where we anticipate a cut of 25 bps.

—Brian Pérez

PERU: BCRP HOLDS KEY RATE FOR THE SEVENTH TIME AND GIVES SIGNS OF START OF RATE CUTS CYCLE

The board of Peru’s Central Bank (BCRP) kept its reference interest rate unchanged at 7.75% on Thursday, for the seventh consecutive time, in a decision expected by the market consensus and by us, although this time we were not so convinced of a hold.

As expected, the focus is on the signals provided in the BCRP’s statement. Unlike the previous statement we see more dovish signals, which was also expected.

A first sign is that it removed the phrase "does not necessarily imply the end of the cycle of rising interest rates”, which suggests that indeed hikes have ended.

A second sign is that the statement incorporated concern about economic weakness, noting that "the shocks derived from social unrest and the coastal El Niño have had a greater than expected impact on economic activity and domestic demand." We expected wording like this in July, but it was not included until yesterday’s statement. The MinFin recently reduced its economic growth forecast for this year from 2.5% to 1.5%, and the market consensus has fallen from 1.8% to 1.3% according to the latest BCRP survey. Economic growth in H1-23 was almost nil, disappointing, and a growth of 3% in the second half will be needed to reach the official estimate. It is hard but not impossible.

The BCRP’s concern about economic weakness could be interpreted as a sign that the BCRP would be willing to bring forward the cycle of interest rate cuts. The BCRP's growth forecast is 2.2% and its voiced worries about the economic outlook suggest that this projection will be revised lower in the September inflation report. That is probably the right time to start the interest rate cutting cycle.

The BCRP ratified in its statement that it expects inflation to reach the target range (between 1% and 3%) at the beginning of next year and emphasized that the transitory effects on inflation have begun to dissipate since June, causing the trajectory in headline/core inflation and 12-month inflation expectations to decrease significantly. This reflects that the evolution of inflation is in line with what was expected by the authorities. The BCRP’s statement considered signs of caution, noting that even headline, core and 12-month inflation expectations are still above the upper limit of the target range (between 1% and 3%), and insisting that there are risks associated with weather factors (El Niño). Sales price and input cost expectations for 3 months posted an increase in July, remaining in bullish territory, according to a BCRP survey.

Inflation expectations for 12 months fell from 3.8% to 3.6%, according to the BCRP survey, reaffirming its downward trajectory, although still above the target range (between 1% and 3%). The survey also showed that 24-month forward inflation expectations fell from 2.9% to 2.8%, within the target range for the second consecutive month, reflecting that consensus still sees inflation returning to the target range could take time. Inflation has remained outside the target range for 26 months, a record period.

Our monitoring of key prices suggests a slower pace for August than in July, although still above the historical average. With this, we believe that year-on-year inflation will be close to 5.5% in August. So far this month, there has been an increase in the prices of perishable foods and local fuels, offset by lower poultry prices. Core inflation in August would be close to that of July (0.29% m/m), with which the annual rate would remain around 3.9%. Our inflation forecast of 5.00% for the end of 2023 has a downward bias going by data at hand, but we maintain our scenario due to the risk presented by the proximity of the El Niño.

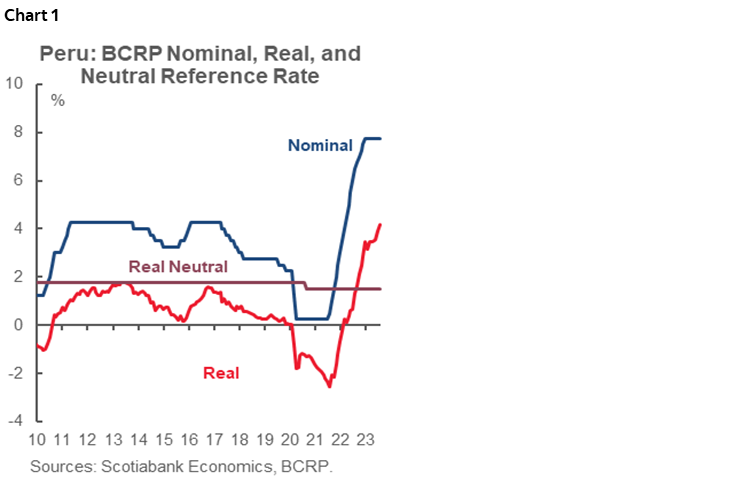

Although the BCRP maintained its policy rate at 7.75%, the real interest rate rose from 3.9% to 4.2% (chart 1), well above the neutral level (1.50%), accumulating a year in contractionary territory. This leaves room to start the rate cuts cycle without significant changes in the stance of monetary policy. We were waiting for these signals to make changes to our interest rate forecast scenario.

We see it as likely that the start of interest rate cuts will be brought forward, possibly as early as September. We do not see consecutive cuts at each meeting (there’s four meetings to go this year), but with pause. At least it is the pattern that the BCRP has used in the two cycles of pre-pandemic cuts (2017 and 2019) and it would be consistent with the caution that the BCRP should maintain with an El Niño ahead.

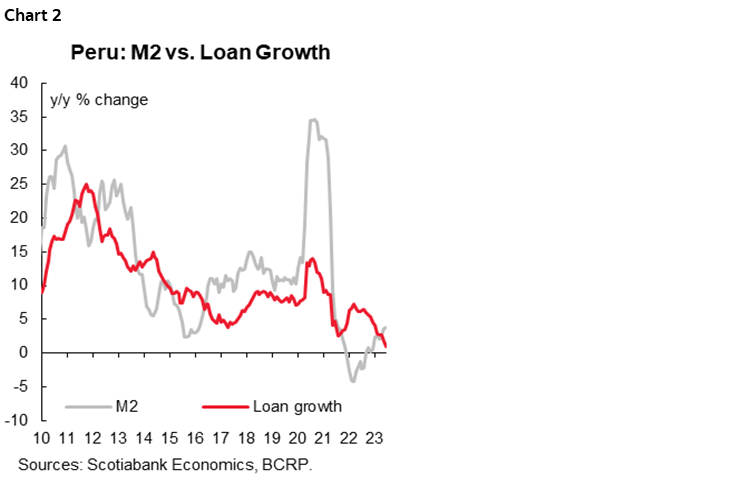

Our new scenario implies increasing rate cuts from 50bps to 75bps for this year, with a policy rate of 7.0% in December. For 2024 we maintain 200bps in rate cuts, bringing the policy rate to 5.0%. Financial conditions remain tight, characterized by weak credit expansion, which went from 1.8% y/y in May to 1.0% y/y in June, in line with the weakness of the economy and the contractionary stance of the monetary politics. However, liquidity growth in soles (M2, chart 2) stabilized at 3.7% in June, remaining in expansionary territory for the tenth consecutive month.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.