- Colombia: After nine months in government, Pres Petro made substantial changes to cabinet

A quiet European morning with no notable data of note is carrying over the positive earnings mood from yesterday in the US, with markets awaiting what will likely be a softer-than-forecast US Q1 GDP print at 8.30ET—following sizable revisions to retail sales data earlier this week. Global markets may (should) already be relatively well aware of this risk, but the outdated 1.9% projection by the median economist on Bloomberg being missed by the actual release still opens up some risk. The accompanying core PCE reading for the quarter (ahead of tomorrow’s Mar PCE) will also be important for the global tone.

SPX futures are up 0.5%, the USD is mixed and in relatively narrow ranges against the majors (the MXN is little changed) and, on net, moves along sovereign debt curves are small. Oil prices are about 0.3/4% higher but copper and iron ore are weaker, down 0.5% and 1.3%, respectively.

The Latam day ahead presents March Mexican international trade data at 8ET, which is expected to show a ~USD900mn deficit that would roughly half February’s negative balance though still represent a ~USD1bn worsening versus last March’s USD105mn surplus.

Brazilian IBGE services data out at the same time should have limited impact on local markets which maintain their focus on the country’s fiscal backdrop; we get March government budget balance data at 13.30ET. BCB Gov Campos Neto heads to Congress again today, at 9ET for a debate on “Interest, inflation and growth”, and will be joined by Fin Min Haddad. Minister of Planning and the Budget, Tebet, said yesterday that the government will present a third package of revenue-raising measures were the first two to fall short of target.

By and large, however, the most important developments to follow today will be the cabinet shuffle in Colombia that saw Fin Min Ocampo leave his post yesterday (see below). We await more statements from new Fin Min Bonilla to gauge how much markets may have to further brace for political and fiscal risks. In thin, after-market trading, Colombian assets took a hit. More losses may continue today as markets adjust, and uncertainty about what decision BanRep will take tomorrow may also have increased.

—Juan Manuel Herrera

COLOMBIA: AFTER NINE MONTHS IN GOVERNMENT, PRESIDENT PETRO MADE SUBSTANTIAL CHANGES TO CABINET

Over the past couple of days, we have had important announcements from President Petro. On Tuesday night, after the approval in Congress of the first step in the health reform process with the debate in the Seventh Commission of the Chamber, President Petro announced the end of the political coalition with the Partido de La U, Liberal and Conservador, which means that he has not longer a majority in Congress. Petro also requested the resignation of the entire ministerial cabinet, declaring that the government must work more to carry out the reforms.

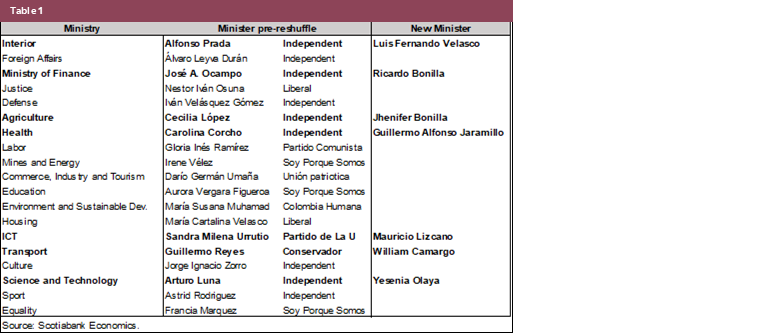

Yesterday, after market hours, it was announced that the President accepted the resignation (and thus change) of seven of nineteen ministers, which represents the biggest shakeup in cabinet since President Petro took office (the first significant change took place in February, with the replacement of Education Minister Gaviria, a strong dissenter of the Health Reform and the ministers of Culture and Sports).

Changes to cabinet are significant, and this time, it included the departure of a key official, Jose Antonio Ocampo, now former Finance Minister. Further to the ministerial changes, President Petro named Carlos Ramón González as the new director of the Administrative Department of the Presidency of the Republic (DAPRE). The main changes are listed in table 1.

One interesting fact to highlight is that President Petro decided to remove Carolina Corcho as Health Minister, which could reflect a willingness to continue health reform negotiations, now with a Minister (Jaramillo, who previously worked as Bogota health sec under Petro) with a well-regarded background and whose main responsibilities will be to find consensus in Congress.

Among the changes, we also find that the new cabinet incorporates qualified professionals and also gives participation to some people whom in the past were closer to traditional parties, as in the case of the interior minister, which opens the to finding ways to negotiate with Congress.

In next-day trading, markets have taken negatively to the news of Ocampo's resignation. The 5Y CDS spread have increased 8% to 307, while COP depreciated 2.8% to COP4660. Of course, this is the initial effect; we need to wait for the first announcement of Minister Bonilla. In his first tweet, Bonilla said he "will maintain the economic stability.”

As has been demonstrated in many occasions, the institutional framework in Colombia is robust, and thus the presidential team has to continued to pursue and necessitate consensus. In the case of the Finance Ministry, the fiscal rule is a mandate established and monitored by an independent committee, which ensures transparency in fiscal accounts.

It is worth noting that Bonilla will not participate in Frida’s Monetary Policy Meeting, he is expected to take office on May 2nd. In any case, BanRep has demonstrated being an independent institution focusing on the inflation-targeting mandate. That said, for Friday's vote, our call remains to favor rate stability, mainly due to macroeconomic reasons that point to economic activity slowing down and inflation expectations moderating. However, the current political scenario presents a challenging environment for BanReps since risk premiums could increase. We highlight that Minister Bonilla, during Petro's presidential campaign, said that fiscal responsibility is a must for emerging markets, which should be of some reassurance.

More about Bonilla

Former Minister Ocampo will be replaced by Ricardo Bonilla as Finance Minister, who had been serving as President of Financiera de Desarrollo Territorial S.A. (Findeter). He is an economist with degrees from the National University of Colombia and Jorge Tadeo Lozano University, with an advanced studies diploma from the University of Rennes, France. He has been a professor at the Javeriana and Nacional universities and a member of the Colombian Academy of Economic Sciences (ACCE). He is a follower of the Keynesian line of economics, which makes him a faithful representative of the moderate or social democratic left.

Bonilla was Secretary of the Treasury of the Bogota Mayor's Office between January 2012 and April 2015 (during the administration of today's President Petro) and has advised Petro on different economic matters. Currently, he has been one of the most important advisors for the pension reform. He is in favor of all workers contributing to the public system and that people with monthly incomes greater than four times the minimum wage can make additional contributions to the private system if they wish.

In summary, recent developments in Government’s cabinet will continue to weigh on political uncertainty. Losing coalitions in Congress will delay the legislative agenda, while the pricing of financial assets will continue to have the additional spread in place since Petro took office. For instance, in our models, the COP exchange rate has a ~700 pesos depreciatory weight due to the political uncertainty.

—Sergio Olarte, Santiago Moreno, & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.