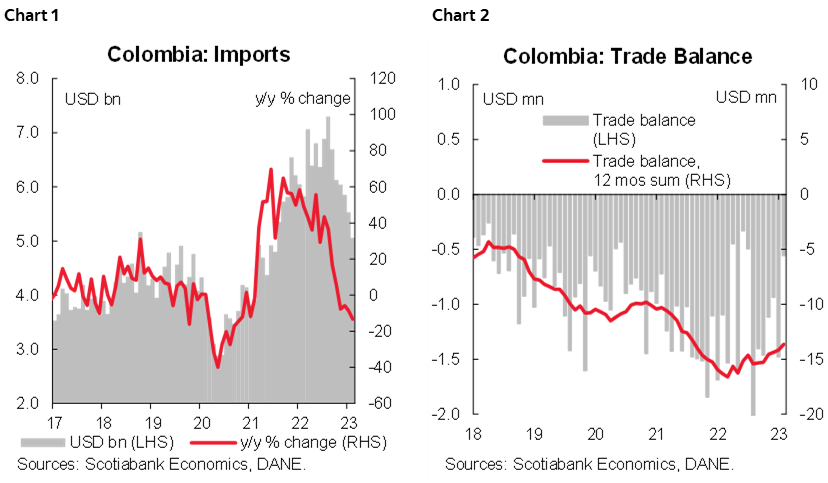

- Colombia: Imports were the lowest since mid-2021, mirroring the economic slowdown

Markets are heading into the Americas session with an uncertain feel as European started with a risk-off feel before the mood brightened over the past few hours, albeit on little of note. G10 and Latam markets await key data over the next few days that will narrow expectations for central bank decisions around the corner (see Latam Weekly).

SPX futures are down 0.2% while US rates are lower 3/4bps across the curve. Crude oil is coming back from its worst levels overnight but is still 0.4% weaker while iron ore is down ~4% amid weak Chinese steelmaking demand and copper is a touch firmer (+0.3%). The USD is mixed against the majors, with no obvious narrative ahead of regional Fed business surveys.

Mexico’s CPI release at 8ET is the highlight of the Latam day ahead. We—and the median economist surveyed by Bloomberg—believe that core inflation will drop the eight-handle after it reached a peak of 8.66% in the H1-Nov print. We think policymakers in Mexico will also close out their hiking cycle at their upcoming May 18 announcement with a final quarter-point increase. The median in the latest Citibanamex survey also sees a 25bps hike then, but economists are virtually split and so are markets. The MXN closed below the 18 pesos level again on Friday, with some upward pressure in the cross to start the week as the peso sheds a modest 0.2% on the day.

BCCh board member Cespedes speaks at 11ET on the Chilean bank’s latest monetary policy report, as the bank has shifted to a firmer wait-and-see stance that has pushed away rate cut expectations. His address will follow the publication of the Central Bank Traders survey at 8.30ET which could show higher year-end policy rate expectations; at 9ET, we also get PPI data for March. The BCCh announced last Friday that, thanks to the “adequate evolution” of the FX market, it would begin the gradual reduction of its USD9.1bn FX forward operations, starting today at a 1/10 monthly pace equivalent to USD50mn. The programme had been launched in July 2022, following the CLP’s intraday depreciation to 1,050+ pesos levels and in late-December it had announced that it would maintain the USD9.1bn forwards renewal until early-June.

—Juan Manuel Herrera

COLOMBIA: IMPORTS WERE THE LOWEST SINCE MID-2021, MIRRORING THE ECONOMIC SLOWDOWN

February imports data, released by DANE on Friday, came in at USD 5.058 bn (CIF terms), contracting by 13.2% and reaching the lowest levels since mid-2021 (chart 1). The trade deficit stood at USD 555 m (-49.3% y/y), which is the lowest monthly deficit since mid-2022 (chart 2). These data reflect the deceleration in economic activity. On a year-on-year basis, the most significant contractions were in capital goods (15.5% y/y) and raw materials (-17.2% y/y), which reflects the domestic demand slowdown. Given these results we affirm our expectation of monetary policy rate stability starting with the April 28 meeting. On the other hand, seeing lower external deficits contributes to reducing depreciatory pressures on the FX.

In annual terms, manufacturing contracted -16.6% y/y, and was the main negative force for the overall picture. Agriculture-related imports increased by 1.5% y/y, and oil-related imports fell by 4.5% y/y.

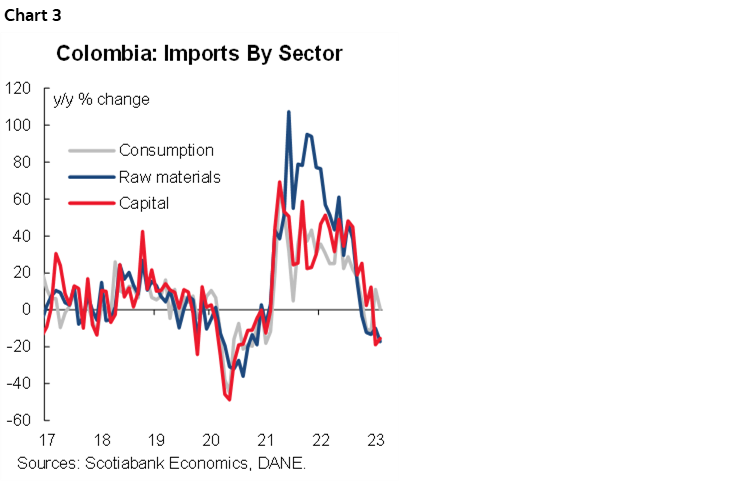

In terms of imports by use, the three major segments showed strong contractions compared to one year ago (chart 3)

- Consumption-goods imports expanded by 0.4% y/y and stood at USD 1.15 bn, the lowest level since August 2021. Non-durable goods contracted by +1.7% y/y, while durables expanded by 3.1% y/y. In the case of non-durable goods, clothing (-15.1% y/y) and items ex-food and clothing (-12.4% y/y), dragged the most in the performance. In the case of durable goods, vehicle imports surged by 38.7% y/y, suggesting a normalization in the international supply chain, unfortunately, the new vehicle stock came with higher prices and now the demand is weakening.

- Raw-materials imports contracted 17.2% y/y to USD 2.44 bn the lowest level since September 2021. Imports of raw materials for the industry (-20.8% y/y) contributed the most to the contraction, especially in the agricultural (-25.6% y/y), mining (-23.2% y/y), and chemical sectors (-26.5% y/y).

- Capital-goods imports went down by 15.5% y/y to USD 1.46 bn, the lowest level since June 2021. The most negative contribution came from transport equipment (-30% y/y), followed by capital goods for the industry (-10.7% y/y).

Imports started to moderate in September 2022, mirroring the domestic demand slowdown. All the relevant classifications (consumption goods, capital goods, and raw materials) are at their lowest levels in about one year and a half. All of the above is another sign that economic activity is weakening, and contributes to our expectation of rate stability at BanRep’s meeting on Friday. On the flip side, the year-to-February trade balance contracted by 26.85% y/y, which poses lower pressure on the COP.

—Sergio Olarte, Santiago Moreno, & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.