- Brazil: IPCA-15 misses, BCB minutes highlight risks.

- Mexico: Unemployment and trade balance misses have limited impact on Banxico.

- Chile: BCCh scraps FX intervention programme as planned. Government will send the pension reform plan to Congress in October.

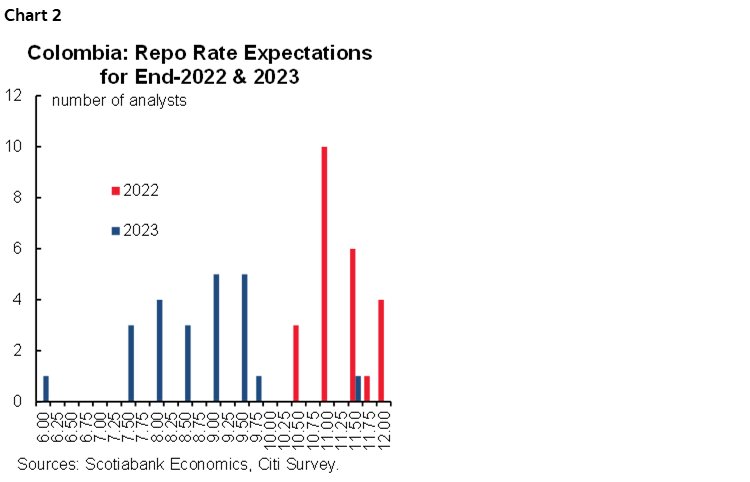

- Colombia: Citi survey showed split opinions about monetary policy rate.

Global markets traded with a more upbeat tone overnight thanks to a quiet backdrop after the recent market rout on a hawkish Fed and the UK’s poorly-received ‘mini-budget’ announcement.

While the Fed sticks to a hawkish message and global recession fears remain, it seems unlikely that market sentiment will significantly recover—with risk-sensitive Latam assets remaining on the backfoot. Yesterday, key currencies in the region weakened from 0.7% in the case of the Peruvian sol to as much as a 2.4% loss for the Brazilian real.

Despite a steep weakening of the Chilean peso in the month-to-date of close to 10% (and a 2.2% drop on Monday), Chile’s central bank confirmed yesterday that its FX intervention programme will end on Friday, as scheduled. Since launching the programme in mid-July, the CLP has strengthened by over 5% from the 1,050+ pesos per USD mark (compared to about a 2.5% gain for the MXN and a 1% loss for the COP, for instance). The bank may think broad dollar strength and risk-off sentiment, as well as soft copper prices, are currently in the driver’s seat for the CLP and intervention is no longer needed. The CLP has nevertheless been the worst performing major Latam currency through September and a continued divergence in the peso’s fate versus its peers could prompt the BCCh to reassess the need for intervention in currency markets. However, the bank announced it will roll over USD9.11bn of forwards until January 13, which should ease downward pressure on the CLP as the BCCh had effectively become a net buyer in USD amid expiring forwards. The CLP is up 0.5% on the day, compared to an unchanged MXN.

Chile’s Labour Minister announced yesterday that the government will submit a pension reform proposal around late-October with the details provided last night in line with the government’s guidance over the past few months. See our Chile team’s analysis of the announcement and yesterday’s approval of the government’s tax reform by the Lower House Finance Committee.

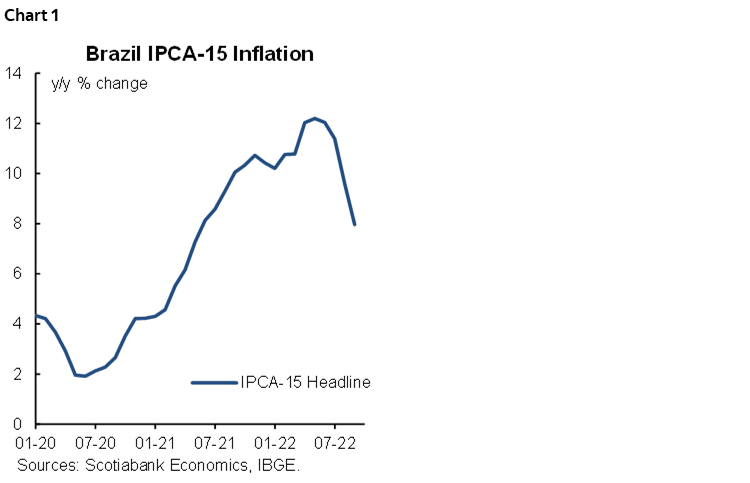

Brazil’s September IPCA-15 data published this morning showed a continued (and larger than forecast) deceleration in year-on-year headline inflation (chart 1), coming in at 7.96% from 9.60% in its previous reading (vs 8.14% consensus) while the month-on-month reading showed a smaller decline in prices at –0.37% from –0.73% previously (vs –0.20% consensus). While the BCB may be comforted by falling annual headline inflation, continued pressure in core prices (e.g. personal services IPCA-15 up 8.3% y/y) could eventually see them return to a tightening path after last week’s rate pause.

The BCB’s meeting minutes published this morning reiterated the bank’s readiness to resume its hiking cycle if inflation does not remain on a downward trajectory. The tone of the minutes also stands in clear contrast to the cuts projected by markets and economists next year. The two Copom members that voted for a ‘residual’ 25bps hike warned of longer-lasting inflationary pressures while the rest of the council preferred to take a cautious approach and observe the impact of hikes to-date. Brazilian assets remain laser focused on the results of this weekend’s first-round elections with polls pointing to the possibility that Lula takes an outright majority on Sunday. The BRL is up ~1.5% at writing, leading all major currencies, on a combination of risk-on trading and correcting for its underperformance yesterday—despite the inflation miss.

After softer-than-forecast economic activity (IGAE) data published yesterday, Mexico reported an unexpected increase in the unemployment rate in August to 3.53% from 3.43% and 3.40% expected; in seasonally adjusted terms, the jobless rate rose marginally, to 3.28% from 3.22%. Mexico’s international trade balance narrowed by around USD460mn in August to USD5.5bn, against a larger expected decline to USD4.9bn. Today’s data have limited impact on Banxico’s policy decision on Thursday, where we anticipate a 75bps increase that takes the policy rate closer to our 10.25% terminal rate forecast (with upside risk owing to persistent inflationary pressures).

The day ahead will centre around speaking appearances by central bankers in the US and Europe, with the BoE’s chief economist Pill (9:35ET) in the spotlight as markets look for guidance on the bank’s response to the recent sterling and gilts selloff.

—Juan Manuel Herrera

CHILE: BCCH SCRAPS FX INTERVENTION PROGRAMME AS PLANNED. GOVERNMENT WILL SEND THE PENSION REFORM TO CONGRESS IN OCTOBER.

On Sunday, September 25, the Minister of Labour and Social Security provided early guidance on the content of the Pension Reform plan, which would be delivered to Congress in late-October. The main change announced by the Minister was the elimination of one of the current pension options called “programmed withdrawal”, which will be replaced by a new “life annuity” that will offer the possibility of inheriting the funds under certain conditions. This benefit will apply to the 10% individual contribution, while the additional 6 ppts will not be inherited. Regarding the additional contribution of 6 ppts, the government confirmed that it will be allocated to a common fund, resources that will be redistributed among the contributors based on salary, gender, among other characteristics. At the same time, the creation of a new public manager was confirmed, who will receive future mandatory contributions. Consequently, the role of the current private administrators (AFP) will be reduced. Finally, the replacement of the current five multifunds (A, B, C, D & E; from riskier to more conservative) by a new "generational fund" was announced, which will imply that the contributors will remain in the same fund during their working life, without changes.

In our view, the aforementioned details are in line with the general guidelines given by the government in recent months in terms of increasing mandatory savings, strengthening government benefits, reducing the role of the current private managers (AFPs) and ensuring the heritability of individual funds. In this line and taking into account the result of the plebiscite, we anticipate a slow discussion in Congress and possible changes to the bill, which will be necessary to obtain the support of the right-wing parties in both houses of Parliament.

Regarding the Tax Reform, the Finance Commission of the Chamber of Deputies approved (in a general sense) the bill sent by the Ministry of Finance a few weeks ago, thanks to the support of the government parties. Despite this, the right-wing parties rejected the proposal, which foresees a difficult process in Congress. In our view, moderation in structural reforms will be necessary to pass them in Congress.

For its part, the central bank announced the end of the FX intervention program on September 30, as expected (see our Latam Flash). With this, the program will complete USD6.15bn in spot sales of dollars (USD10bn previously announced) and will renew the foreign exchange hedge stock of USD9.11bn sold until September 26 (USD10bn previously announced). According to one of the members of the Board (Mrs. Griffith-Jones), the intervention was successful until the week of September 23. In recent days, the Chilean peso has depreciated to CLP992 per dollar, reaching its highest level since the announcement of the central bank’s foreign exchange intervention (July 14), mainly due to the fall in the price of copper and the appreciation of the US dollar (DXY). However, as of September 26, the depreciation of the CLP against the US dollar is greater than in multilateral terms, which is less inflationary for the Chilean economy.

—Aníbal Alarcón

COLOMBIA: CITI SURVEY SHOWED SPLIT OPINIONS ABOUT MONETARY POLICY RATE.

September’s Citi Survey, which BanRep uses as one of its measures of inflation expectations, the monetary policy rate, GDP and COP, was published on Monday, September 26.

Key points included:

- Projections on economic activity improved for 2022, but deteriorated for 2023 again. Economic growth for 2022 is expected to reach a pace of 7.31%, above the previous forecast (6.87%). By 2023, economic growth expectations fell to 1.98% (previous: 2.32%). Looking ahead to 2024, economic growth is expected to be 2.77%, vs the previous expectation of 2.91%.

- Inflation expectations deviated further from BanRep’s target range. September’s monthly inflation rate is expected to be, on average, 0.75% m/m and 11.24% y/y. Scotiabank Economics is in line with consensus with 0.68% m/m and 11.6% y/y. In September, food inflation will continue leading to upside pressures to the inflation, in the same vein, some services, especially education will contribute to having monthly inflation above average. Colombian inflation expectation for markets is expected at 0.64% m/m in the survey, making the main difference vs. our expectation of 0.52% m/m. By the end of 2022, the consensus expects inflation to close at 11.46% well above the previous expectation of 10.05%. In 2023, inflation is expected to stand at 6.79%, still above the central bank’s target range, and also increasing from previous survey.

- Ahead of September monetary policy meeting, the majority of analysts expect a 150bps move to 10.50%, 9 analysts expect a 100bps hike, while only 2 expect a 125bps hike (chart 2). Scotiabank Economics is aligned with consensus. By the end of 2022, the key rate is expected at 11% by the median consensus, Scotiabank Economics expects 11.5%, while the maximum expectation is 12%. For the 2023 consensus, monetary policy expectations are that the rate will return to around 8.75%, showing that the rate will remain well above historical average levels as inflation shock is more persistent than anticipated.

- USDCOP forecasts point to further currency depreciation through December 2022. On average, respondents expect a level of USD COP4,270 by the end of 2022 and 4,137 by 2023.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.