- Chile: Surprisingly unchanged economic activity in August

- Colombia: Marginal job gains support BanRep deceleration

- Mexico: Banxico survey and AMLO anti-inflation plan update

- Peru: Regional and municipal elections; the right takes Lima

Cautious trading is spilling over into the new week amid limited catalysts to support a rebound in risk sentiment as markets look ahead to Friday’s release of US nonfarm employment. The risk backdrop is relatively intact, with only a short-lived improvement in sentiment earlier today on the UK’s U-turn on scrapping plans to eliminate the 45% tax rate; much more needs to be done to turn markets around.

The USD is trading mixed to weaker against the major currencies while commodity-FX outperforms thanks to gains in crude oil prices on reports that OPEC+ will announce a 1mn+ barrels supply reduction at its output meeting on Wednesday. The MXN is recording a 0.3% gain on the day as it nearly unwinds its losses since the UK-motivated selloff in global markets.

Brazil’s first round presidential election on Sunday delivered a much closer result than polls ahead of it had suggested. Former President Lula took 48.4% of the vote against the incumbent Bolsonaro’s 43.2% share. Some speculation had built ahead of yesterday’s vote that Lula would eke out a 50%+1 majority that would avoid a second round on October 30, but the weekend’s results now point to a hard-fought four-week campaign period that could see the balance shift in Bolsonaro’s favour. Lula may now have to rein in his more ’leftist’ aspirations (that had weighed on local market sentiment) with Bolsonaro closer than expected. For offshore markets averse to Bolsonaro, Sunday’s close result may be of some concern initially as will a few more weeks of uncertainty, but a more moderate Lula government on the other side would be a plus. The BRL is starting the week with a majors-leading gain of 2.7% at writing.

Economic activity surprisingly held unchanged y/y in Chile in August, according to data published this morning (see Chile section below), which has helped the CLP to a 0.7% appreciation against the USD today—with the BRL’s strength likely exerting a pull higher, too.

Later today, we’ll monitor the results of the most recent Banxico survey of economists out at 10ET that should show upward revisions to inflation and central bank rate forecasts (see Mexico section).

See also in our Colombia section a recap of Friday’s employment data that showed marginal job gains in Colombia last month that supports a deceleration in BanRep’s hiking pace. In Peru, Lima’s local elections have delivered a close decision between two right-wing candidates that is too close to call (see below).

—Juan Manuel Herrera

CHILE: SURPRISINGLY UNCHANGED ECONOMIC ACTIVITY IN AUGUST

Chilean economic activity was surprisingly unchanged in year-on-year terms in August, according to data published this morning by Chile’s central bank (BCCh), in contrast to our and the consensus median forecast that foresaw a significant y/y decline. Compared to the previous month, economic activity rose 0.6% thanks to a 0.7% m/m expansion in ex-mining GDP.

Despite today’s positive surprise, we anticipate a string of year-on-year contractions in GDP lasting until Q2-2023, consistent with our GDP forecast of -0.9% for 2023. In this contractionary context, we maintain that—contingent on inflation slowing in coming months—the BCCh will be forced to cut its benchmark rate quickly and aggressively amid a negative output gap and an economy heading towards a full-blown recession. We anticipate a cut of no less than 100bps at the BCCH’s sole meeting of Q1-2023 compared to the bank’s baseline scenario that sees a 25bps reduction during the quarter.

Last Thursday, President Boric announced a real expansion of fiscal spending of 4.2% y/y, in line with expectations and the government’s fiscal rule. The Ministry of Finance will release more details during the presentation of the Q3-2022 Public Finance Report due to Congress next on Wednesday (Oct 5). In our view, with this modest expansion of fiscal spending, the government would reduce the structural deficit from the 2.6% of GDP projected in the Q2-2022 Public Finance Report, while taking into consideration the increase in structural revenues due to an improvement in long-term GDP growth and copper prices. On the other hand, the increase in public debt towards levels above 40% of GDP in 2023 seems inevitable.

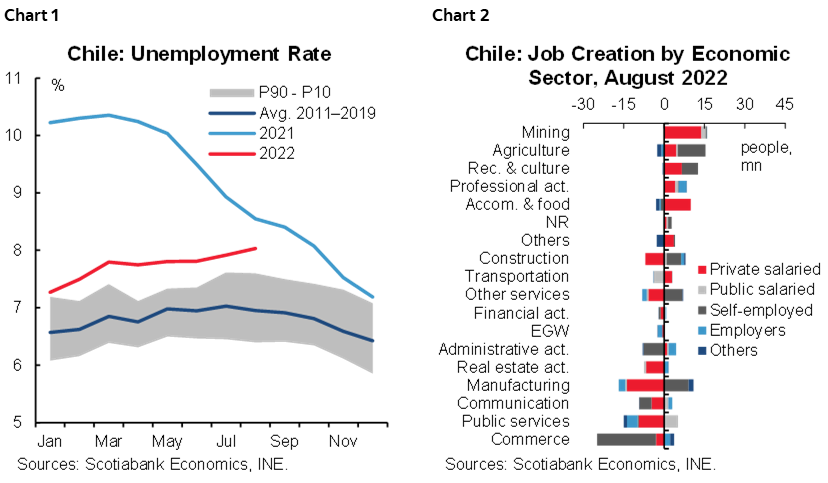

Chile’s statistical agency (INE) reported an unchanged unemployment rate of 7.9% in the country in August (in data released last Thursday). The country’s jobless rate came in below our expectations and those of the market, at 8% (chart 1). Compared to the previous 3-mth period, Chile’s labour force and employment levels saw no significant expansion. On the employment side, job creation in services and mining was completely offset by job destruction in wholesale and retail trade (self-employed), manufacturing (private salaried) and education (chart 2). The performance of employment in these various sectors in recent months seemingly reflects the slowdown in economic activity, concentrated in wholesale/retail trade and manufacturing.

With labour market slack beginning to open somewhat earlier than anticipated, one would expect lower underlying inflationary pressures (via reduced wage pressures) which would motivate relatively less restrictive monetary policy all else equal. To the extent that we see a stabilization in the Chilean peso (CLP), we should begin to see a normalization in inflation starting in November. For the central bank, labour market signals indicate that additional limited increases in the monetary policy rate are still in order so a neutral policy bias can be attained at the December monetary policy meeting. The rate cuts process may then begin once all the inflationary determinants (domestic and external) support an easing of monetary policy.

—Aníbal Alarcón

COLOMBIA: MARGINAL JOB GAINS SUPPORT BANREP DECELERATION

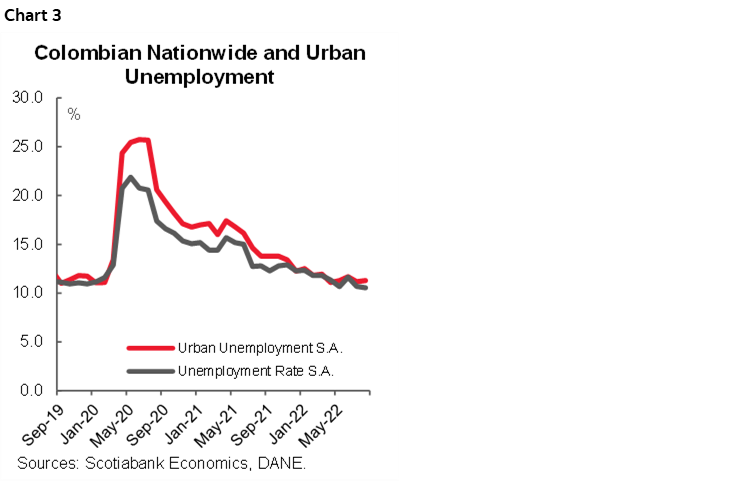

Employment data for August, released on Friday showed that job creation improved at the margin again. The national unemployment rate stood at 10.6%, while the urban unemployment rate (main 13 cities) was 10.8%. Both indicators are lower than the August 2021 levels of 12.9% and 13.4%, respectively. In seasonally adjusted terms, the nationwide unemployment rate also improved, and for the nationwide reference, it decreased from 10.7% to 10.5%, while in the Urban figure, it increased a bit from 11.2% to 11.3% (chart 3), however, gains were moderate.

Services related sectors are still the main contributors to higher employment. Formality is also improving, but people outside the labour force are still well above pre-pandemic levels. The data support our view that BanRep is reaching a ceiling in the hiking cycle since job gains have stagnated in monthly terms, possibly reflecting some weakness in the overall economic recovery.

During the last year, four sectors accounted for ~66% of the 1.5mn y/y increase in employment: commerce (+372k), public administration, education and health (+300k), leisure-related activities (+203k), and manufacturing (+181k). All of the above sectors showed that the services sector is leading the labour market recovery. On the flip side, the agriculture sector (-30k) is the only one that experiences a contraction in employment compared to a year ago, as it faces difficulties due to higher input costs and reduced economic activity.

Women again benefited the most from the recovery in employment. Services-related sectors, such as commerce, and leisure accounted for half of the job gains for women. As for men, commerce and manufacturing were the main contributors to job gains. The female unemployment rate now stands at 13.3%, which is 3.2ppts below its year-ago level and 4.6ppts above the male unemployment rate (8.7%), as the gender gap in labour markets narrows.

At a nation level, the informality rate stood at 58.1%, improving from the 60.3% of last August. In the case of urban informality, it stood at 43.8%, which is also lower compared to 45.8% twelve months ago. Despite continued improvements in formality rates, gains are moderate as employment is concentrated in the highly-informal services sector.

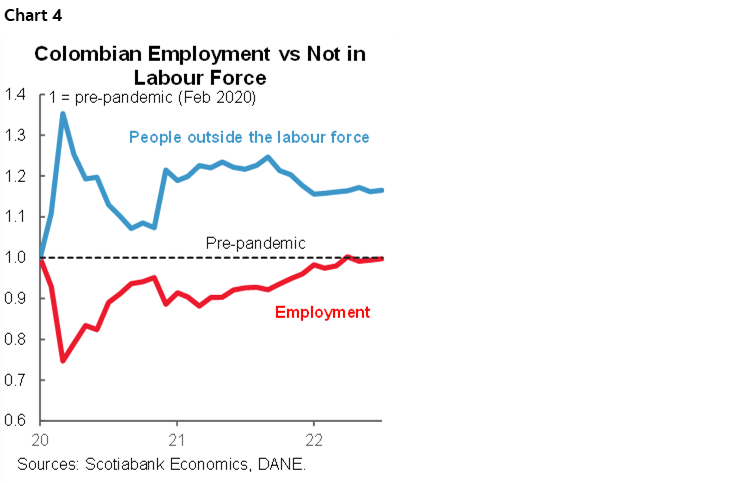

Inactivity remains a main source of uncertainty. In August, it was 16.5% (or roughly ~1 million people) above the pre-pandemic rate (chart 4). Some outside of the labour market report non-salary/wages income, which may correspond to the high level of remittances seen of late.

In conclusion, the labour market continues to show moderate improvements. Services sectors are still leading the recovery, while people outside the labour market are worth monitoring. We think the data support our view of BanRep is reaching a ceiling in the hiking cycle as job gains have stagnated month-on-month, reflecting some weaknesses in the overall economic recovery.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

MEXICO: BANXICO SURVEY AND AMLO ANTI-INFLATION PLAN UPDATE

The results of Banxico’s economists survey for September due later today will most likely show upward revisions to inflation and interest rate forecasts. In the August release, participants’ inflation forecasts averaged 8.15% for Dec-2022, while the median Banxico rate projection for year-end stood at 9.50%. Amid the most recent Fed and Banxico hikes, analysts have also likely lifted their policy rate expectations.

As we mentioned in our Banxico decision flash (see here), we now forecast a 10.50% rate at the December meeting, and we think a fair number of analysts will join this view. However, since responses were sent before September 25, we don’t expect the survey results to incorporate the most recent Banxico forecasts and bias, and the median projection may only move to around 10.00%.

We expect AMLO to release the anti-inflation plan update during his daily press conference today. The plan is focused on items impacting the basic consumption basket, which mostly corresponds to non-core goods (agriculture and energy, which rose 10.65% y/y in August) by either subsidies in energy items, reducing cost of production and distribution, or reducing tariffs in certain products. However, while the plan has resulted in more muted increases in energy prices, it has had practically no impact on the price of other goods—and we wouldn’t expect this to change substantially.

—Miguel Saldaña

PERU: REGIONAL AND MUNICIPAL ELECTIONS; THE RIGHT TAKES LIMA

Peru’s regional and municipal elections on Sunday were, perhaps, not as exciting as Brazil’s presidential elections, but they were significant. Peruvians voted for 25 regional governors, 196 provincial mayors, and 1,694 municipal mayors.

In the key race for Lima, and with over 99.5% of ballots counted, Rafael López Aliaga is (all but certainly) new mayor of Lima. López Aliaga has taken 26.3% of votes against 25.4% for runner-up Daniel Urresti. Both Lopez Aliaga and Urresti are right-wing candidates, and, together with third-placed George Forsyth with ~19% of the count. Lima voted firmly for the right, with the three candidates garnering just over 70% of the vote, combined. Note, however, that of the three right-wing candidates, López Aliaga is viewed as the most radical and the most likely to confront President Castillo’s regime. In contrast, the official Perú Libre party has so far registered 1.5% of the vote, and the left as a whole has attained no more than 8% of the vote. What’s more, the Perú Libre government (or ex-government for some) party did not win in any major region or city in the country.

The left had a very weak showing throughout the country. But, outside of Lima, the right did not do so well either. Nor did the national parties in general. A few important regions voted for the candidate for Somos Perú, a centrist party, but only a smattering of regions backed other national parties, such as Alianza para el Progreso, APP (César Acuña’s party). The predominant vote outside of Lima was not for national parties, but for regional and local parties. Overall, regional candidates are more likely to be skewed to the left than to the right, but they do not normally identify with the national leftist party. Rather, they are mainly linked to local or regional interest groups.

Sunday’s elections confirm that there is no cohesive right- or left-wing political leadership in the country, and reaffirms how fragmented and dysfunctional Peru’s political party system has become.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.