- Colombia: Monetary Policy Preview: Is a 100bps hike enough for the markets?

A rebound in US yields is driving the dollar higher across the board while a mixed-to-weaker commodities backdrop and disappointing results contribute to a soft risk backdrop. The focus of global markets for today’s session will be the ECB’s policy decision at 8.15ET (where we expect a 75bps increase) followed by the US Q3 GDP release at 8.30ET (consensus at 2.4% q/q annualized). Copper and iron ore prices continue on a negative trend as Chinese economic pessimism lingers.

Mexico’s INEGI reported a larger than expected decline in the country’s unemployment rate as well as a narrower trade deficit in data for September published this morning. The country’s non-seasonally-adjusted jobless rate decline to 3.34% against a median forecast of 3.50%; this compares to a 4.18% rate in September 2021. INEGI’s seasonally–adjusted figures saw the unemployment rate fall to 3.14% its lowest level since April 2022 (3.08%). Mexico’s trade deficit sharply narrowed to USD895mn last month from a USD5.5bn previously and against a median forecast of a USD4.53bn deficit, thanks to a strong increase in exports against a sizable decline in imports. Auto exports reached a new record high of USD16.1bn (a 42% y/y increase).

Brazil’s CB left its Selic policy rate unchanged, as expected, at its policy announcement yesterday evening. With headline inflation showing signs of cresting—despite continuing momentum in core baskets, and some of this decline partly driven by a temporary removal of gas taxes—and the runoff election ahead, the central bank left its statement practically unchanged. This notably includes an unchanged rates guidance pointing to its willingness to resume the hiking cycle if inflationary pressures warrant it. On that note, the BCB lifted its end-2023 inflation forecast to 4.8% from 4.6% in its previous iteration.

The minutes to the most recent BCCh decision were published this morning, reiterating the bank’s neutral approach. The minutes also indicated that policymakers discussed a 25bps hike in addition to the 50bps that was actually delivered. The bank has clearly communicated that they have reached the maximum level in their hiking cycle. On the other hand, continued concerns about inflation and no obvious language on possibly policy easing mean the bank is not ready to tee up a rate reduction in early-2023—as is our Santiago economists’ expectation (100bps cut in January).

BCRP Chief Velarde said yesterday that Peruvian inflation will decline without a recession, noting that if the bank succeeds at keeping inflation expectations anchored then it will be successful in reaching its inflation target. With the BCRP also expecting to reduce its public investment estimate for this year, that lessens positive output gap pressures on inflation.

It is a quiet day ahead in our core footprint ahead of BanRep’s policy decision tomorrow, where we now see a 100bps increase (see below).

—Juan Manuel Herrera

COLOMBIA: MONETARY POLICY PREVIEW: IS A 100BPS HIKE ENOUGH FOR THE MARKETS?

Tomorrow, BanRep will hold its seventh monetary policy meeting of the year. The central bank is expected to hike its monetary policy rate by 100bps again, however, the main question is if this hike will be enough for markets given the recent volatility in Colombian assets.

As noted in last week’s Latam weekly, the backdrop for Friday’s meeting is challenging. Some Board members continue to be worried about a potential downturn in economic activity ahead of 2023. But, given recent market moves, the Board could decide to be more hawkish this time around.

Our initial call was of a 50bps hike including an intervention program, assuming that the concerns about economic growth remain. However, after the market’s reaction to the latest meeting, we think BanRep sees this dovish stance as a bad decision against on-edge markets. We therefore now see a higher probability of a 100bps move. Even a full-point hike may not be enough to meet financial markets’ expectations, but in our mind it would be notable as it would affirm the independence of the central bank, as a strong institution in Colombia.

After Friday’s meeting, Colombia’s monetary policy rate will be at its highest point since the beginning of the inflation-targeting regime in 1999. This meeting will be also of particular importance as the staff is expected to present the monetary policy report to the Board, which includes a new macro scenario and balance of risks that are key to determining how close the bank is to the end of the hiking cycle.

The rates curve averaging a 13.5% rate is showing a decent discount based on domestic and international risks. That said, a decision by the central bank teeing up the end of the hiking cycle would motivate further gains (falling yields) in the short-end and belly of the curve. However, in the FX market, it may not be enough to take the currency to the levels prevailing prior to the president’s tweets that impacted sentiment in Colombian assets.

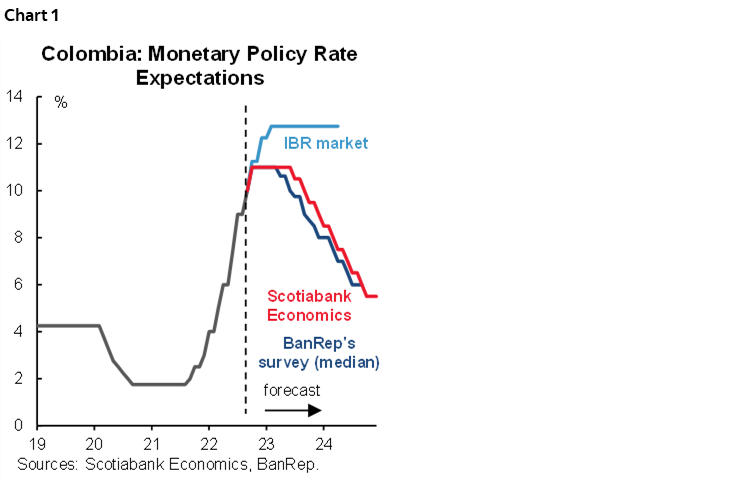

The IBR market is pricing in a 125bps move and a terminal rate of 12.75% by March 2023 (chart 1). We disagree with the market’s opinion as we expect BanRep to end its hiking cycle sooner, and at a lower level.

In the case of the Colombian peso, we see the possibility that BanRep announces a program to control the volatility of the exchange rate via options or NDFs. And we totally discard the possibility of an intervention through direct sales of USDs.

Key points ahead of Friday’s BanRep vote:

- At September’s meeting, we had a split vote of 6 vs 1. The dissenting vote for a 50bps hike argued that the main risk now is a strong economic deceleration. That said, this Board member said that increasing rates aggressively place labour markets at risk and that a large move would not be effective inflation control.

- A split vote usually signals a change of stance in forthcoming meetings. Had the market reaction in recent weeks been more benign, BanRep would have settled on a 50bps increase tomorrow. However, given recent bearish market volatility, the fact that inflation continues surprising to the upside, and the economy is showing still robust signals, the Board will likely deliver a 100bps hike while maintaining a data-dependent approach. We think that markets would be more comfortable with a more aggressive move from BanRep. However, we do not see 125bps or higher move as our base case since the Board remains concerned about next year’s economic activity while still seeing easing headline inflation in the coming months.

- Inflation expectations deviated further from BanRep’s target according to recent surveys. In BanRep’s latest survey, one- and two-year ahead inflation expectations sat at 7.38% and 4.70%, with end-2022 and end-2023 forecasts at 11.90% and 6.93%, respectively. This shows that there is no hope among economists that the bank will see inflation fall within the target range in the medium term, though this is in line with BanRep’s own expectations.

- As always, it will be relevant to monitor signals that the hiking cycle is reaching a terminal phase. At this week’s meeting, the staff will release a fresh set of macroeconomic projections that could signal an impending rates pause.

- On the FX side, the COP remains under pressure, and this time it is not only due to international broad-dollar factors but also idiosyncratic (political) issues. Governor Villar emphasized that the floating exchange regime is appropriate, however, there is some space to see a central bank intervention program to reduce the FX volatility.

All in all, we now expect 100bps that leaves the policy rate at 11.00%, with a potential split dovish vote that sees one or more voting for a smaller increase.

The yield curve recently showed easing pressures and BanRep signaling a pause would contribute to the market positioning in a more medium-term perspective. However, even if we reach the terminal rate, a discussion about future cuts would take time, which would make it difficult to anticipate a stronger rally in Colombian debt. In terms of the FX, a 100bps move could be insufficient to reverse the recent depreciation trend, which is why we expect BanRep to announce also a measure to control the FX volatility. The data-dependent approach should continue, but we expect signs of a potential pause to emerge sooner rather than later.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.