- Colombia: Inflation reaches new 23-yr high but the data surprise was more moderate than previous months

China reopening hopes took a hit over the weekend with the country’s officials reasserting their intention to adhere to current COVID-19 policies. Markets weakened as Asia opened for business but have since moved into modest gains for the day that are taking US equity futures to near Friday’s intraday high.

In the FX space, the USD is trading generally weaker after sharply falling around the European open and holding around those levels amid limited developments. The MXN is modestly better bid on the day, up 0.2/3%, while the CLP opens with a solid ~1% gain to its strongest level since mid-September.

Chile reported a USD457mn trade surplus in data released this morning for October, flipping the sign on the USD513mn deficit recorded in September. The surplus resulted mainly from a significant decline in imports to their lowest point since mid-2021, while on a year-on-year basis there was a sharp 22% decline in copper exports.

Colombian markets are closed today after Saturday’s slight inflation beat that may pressure BanRep to roll out another big hike at its final meeting of the year in December (see below).

It’s a quiet day in the Latam calendar as we look ahead to Thursday’s decisions from Banxico and BCRP where we see respective hikes of 75bps and 25bps. While the former is likely to keep pace with the Fed in the near term, the Peruvian central bank may deliver its final hike of the cycle this week. The US CPI release that same day will keep global markets enthralled and is likely to drive the broad trading mood this week.

—Juan Manuel Herrera

COLOMBIA: INFLATION REACHES NEW 23-YR HIGH BUT THE DATA SURPRISE WAS MORE MODERATE THAN PREVIOUS MONTHS

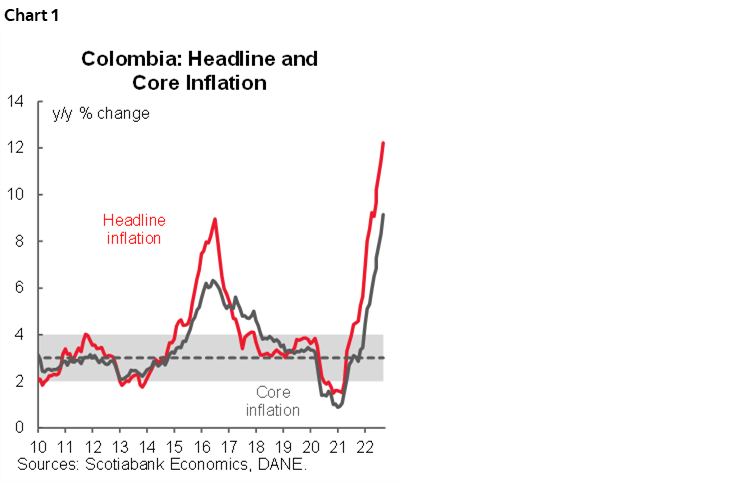

Colombia’s pace of monthly CPI inflation was 0.72% m/m in October, according to DANE data published on Saturday, November 5. The result was well above the BanRep survey’s (0.62% m/m) and slightly below the Scotiabank Economics projection (0.76% m/m). Monthly inflation was 24 times the average inflation observed for the typical October since 2016. Year-on-year inflation stood at 12.22%, increasing from 11.44% in September, and reaching its highest point since March 1999 (chart 1). Colombia is the only PAC country that hasn’t yet seen a peak in inflation during the current cycle.

Core inflation rose again, to 9.15% y/y from 8.32%, and ex-food and regulated goods inflation accelerated to 8.48% y/y from 7.49%. Core inflation is accelerating more than food inflation, reflecting the impact of FX depreciation as tradable inflation increased from 11.82% to 12.26%. But, it also reflects a robust performance of the domestic economy.

October’s CPI results continue to dash BanRep’s hope of an earlier peak in inflation. Upside risks to inflation in 2023 are increasing as the minimum wage negotiations (which start on November 30) will call for a higher adjustment. Inflation expectations deviating from target in the medium term would again place inflation worries among BanRep’s top concerns.

With this in mind, our forecast for the December meeting is now tilted towards a 100bps hike, and a potential pause will likely be delayed until an inflation peak is confirmed which may not happen until Q1-2023.

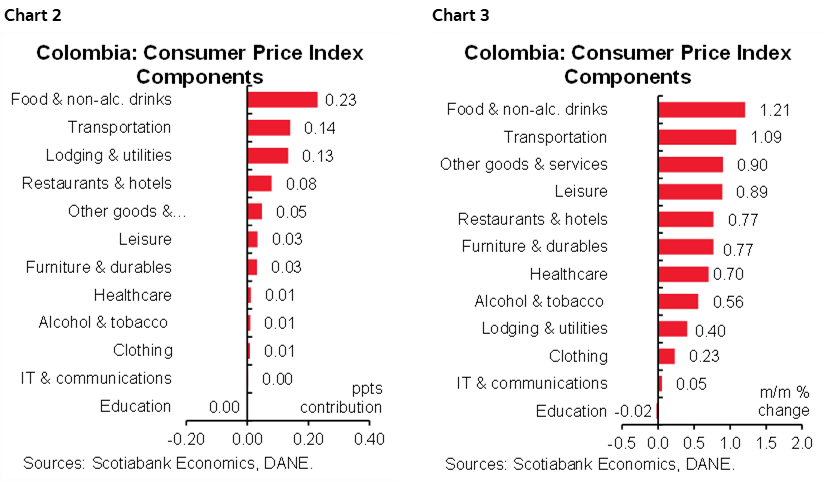

Looking at October’s numbers in detail, eleven out of the twelve components of the CPI basket contributed to higher inflation (charts 2 and 3), and the food group was again the main contributor.

The highlights of the release are:

- Foodstuffs inflation was again elevated with prices growth at 1.21% m/m, resulting in a contribution of 0.23ppts to overall inflation. In October, potatoes led the gains (+14.09% m/m), interrupting five consecutive months of declining prices; the end of the harvesting season is leading to higher prices. The other main contributors in the food group were rice (+2.42% m/m), fresh fruits (+2.27% m/m), and eggs (+2.25% m/m). All reflecting higher input prices, but also the effect of the FX depreciation.

- The second biggest contributor to headline inflation (+0.14 ppts) was the transport group (+1.09% m/m). Within this group, the main contribution came from vehicles (+2.19% m/m), its strongest monthly expansion this year, which not only reflects higher international costs but also the depreciation of the COP. Gasoline prices contributed 0.04ppts to inflation, while other items such as airfares (+2.88% m/m), reflected still strong domestic demand.

- Housing was the third main contributor to October’s inflation (rising 0.40% m/m and contributing 0.13ppts). Rent (+0.22% m/m), continued showing strong increases, while utility fees are still an important contributor to inflation, especially electricity prices (+1.61% m/m). It is important to highlight that the government has reached an agreement to moderate energy prices, though this was not yet in October’s data. In any case, we expect it to have only a modest negative impact given that leading inflationary pressures more than offset the impact of the electricity fee agreement.

- Note that the remaining CPI groups also contributed to October’s inflation, which is seasonally atypical. This shows that despite supply shocks being the main source of inflation, strong domestic demand is also being reflected in higher domestic prices, especially in services-related goods.

- Goods inflation increased from 11.57% to 13.0% y/y reflecting the effect of higher international prices but also COP weakness. Services prices increased but at a slower pace of 6.62% y/y from 5.93% y/y. The asymmetrical response of goods and services prices could reflect the difference between supply and demand sources of inflation. Regulated prices inflation rose 0.58ppts to 12.04% y/y.

To conclude, October CPI data show that inflation should still be the main concern for BanRep. Ahead of 2023 not only indexation effects but also significant FX depreciation will continue to pull inflation expectations from the target range. Ahead of the December 16 monetary policy meeting our bias is towards a 100bps hike. Calls for rate hike pause will have to wait for a peak in inflation which according to our projection will not come until Q1-2023. It is also relevant to highlight that continued large hikes are needed to restore confidence in financial markets to prevent recent risk premium shocks embedded in Colombian assets to become entrenched.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.