- Colombia: Economic activity remains robust in September

- Mexico: Banxico delivers an expected 75bps hike, although unanimity at the board has ended

- Peru: BCRP hikes 25bps, leaves door open

Markets are trading with a mixed feeling as US equity futures track minor losses while the dollar is broadly stronger, after Asian stocks started the week with decent gains on the back of China's 16 measures to support property developers. The news (first reported on Friday) resulted in gains in iron ore prices but aluminum and copper are weaker on LME standing against a ban on Russian aluminum while reporting a big increase in ‘on-warrant’ copper stocks. Comments by Fed hawk Waller last night are broadly weighing on the risk tone after the bounce last week on the weaker-than-expected US CPI print. Headlines will likely call the direction of markets through today’s session, after this morning’s meeting between Xi and Biden that resulted in relatively little aside from diplomatic cordialities—though Biden intends to visit Beijing at an unscheduled date.

Latam currencies are mixed with the BRL at the top of the regional leader-board (+0.3%) while the MXN is practically unchanged and the CLP is about 0.9% weaker. Today, the BCB reported that the Brazilian economy barely grew in September, recording a 0.05% m/m expansion, and its economists survey showed a minor revision higher to inflation expectations—with no change to the rate outlook. At 13ET, VP-elect Alckmin will announce another set of transition team members. The team is expected to finalize a draft of a budget amendment bill by mid-week. Today’s BRL and Ibovespa bounce may be merely on the back of sharp selloffs last week, though reports that centrist parties want to restrict Lula’s spending plans could also be helping.

Following Banxico’s 75bps hike last week (see below) Dep Gov Borja speaks at 11ET with her comments monitored to guide the outlook for Banxico’s rate decisions ahead. On a related note, the IADB interviewed candidates (including Esquivel) for the bank’s leadership on Saturday, with a decision expected on November 20. A replacement for Esquivel at Banxico may be announced this week or next (though AMLO may wait for the IADB to make a decision).

In the week ahead we will monitor GDP and economic activity data out of Colombia, Chile, and Peru, with a quiet calendar in Mexico, while anxiety over Lula’s cabinet will likely continue in coming days. Peru’s Congress has also invited President Castillo to defend himself from treason accusations on Wednesday.

Colombian markets are closed today to celebrate the independence of Cartagena with Brazil closed tomorrow for the Proclamation of the Republic.

—Juan Manuel Herrera

COLOMBIA: ECONOMIC ACTIVITY REMAINS ROBUST IN SEPTEMBER

On Friday, the National Statistics Institute (DANE) released its monthly surveys of economic activity for September. Manufacturing and retail activity showed a mixed performance over the month though both sectors reflect still robust domestic conditions.

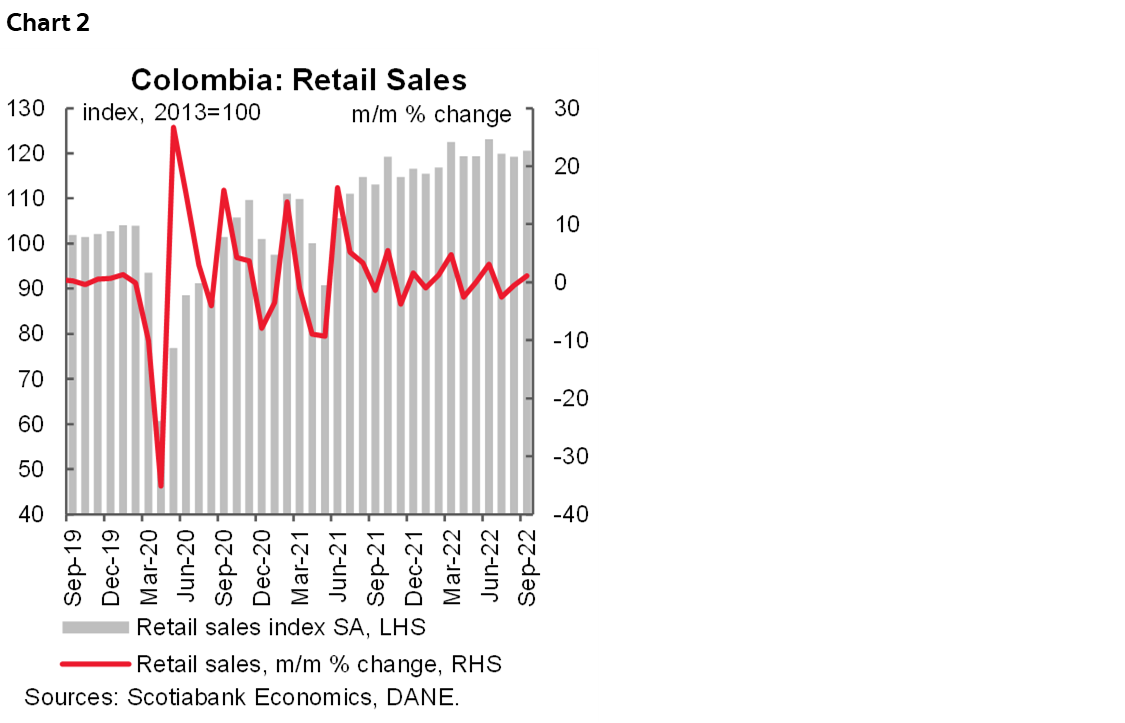

Retail sales increased again month-on-month, extending a strong annual expansion. All sectors associated with mobility continue to contribute to solid retail sales results, especially due to the celebration of Colombia’s Valentine’s Day. As a result, private consumption remains an important contributor to the total growth of the economy, though we expect some moderation in a context of high inflation and higher credit interest rates that should be headwinds for domestic consumption.

Manufacturing

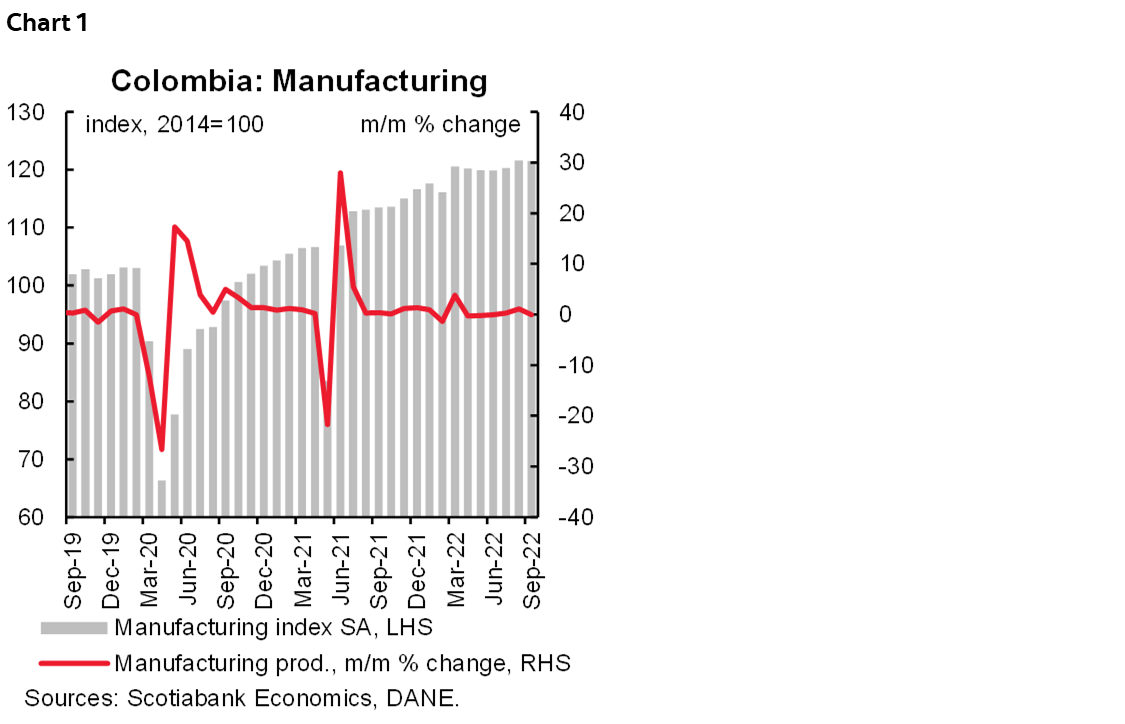

Manufacturing production increased 6.9% y/y (below the market consensus of 7.5% y/y) with a marginal contraction of 0.07% m/m (chart 1). Year-to-date, manufacturing has grown by 13.5% y/y. In our opinion, September’s data show a softening of manufacturing activity, as base effects continue to fade. However, it is also the result of some headwinds that are expected to worsen in upcoming months: high input costs, lower business confidence related to next year’s fiscal backdrop with higher tax burdens, coupled with restrictive interest rates. Taking this into account, we project a decelerating trend in the medium term.

In y/y, the best performing sectors were vehicle manufacturing (+37.1% y/y), clothing (20.1% y/y), chemicals (19.1 y/y), vehicle parts and accessories (+26.3% y/y) and printing activities (+29% y/y), which accounted for 4.3ppts or 55% of the total year-on-year expansion. On the flip side, sectors that subtracted from activity were leather tanning (-27.6% y/y), coffee threshing (-9.4% y/y), travel goods manufacturing (-11.4% y/y), and the precious metals industry (-23.5% y/y) with the weakness likely explained by pressures on production costs and perhaps more moderate demand.

Employment growth stood at 3.6% y/y. On a monthly basis, employment fell 0.5% compared to the 0.2% m/m increase of the previous month. This may be a sign of some weakness in the formal sector.

Retail

Retail sales rose 7.2% y/y in September, above the Bloomberg survey (+7.0% y/y, chart 2), while employment growth held at 3.6% y/y. On a seasonally adjusted basis, retail sales (excluding other vehicles) saw an expansion of 1.0% m/m, stronger than that observed in the previous month against the recent moderating trend. In year-on-year terms, the increase in retail sales has a lower base effect which combined with the reference month including Colombia’s Valentine’s Day could have lifted sales to a certain extent. Having said that, we still believe that, at the margin, consumption levels have moderated, explained by the persistent inflationary pressures affecting household disposable income.

In annual terms, the expansion of retail sales was explained by sales of alcoholic beverages (+21.4% y/y), books and stationery (+36.6% y/y), clothing (12.7% y/y), telecommunication items (+16% y/y), and footwear (17.1 y/y) contributed around 2.1ppts to the total expansion. Although September is a month without holidays, the celebration of love and friendship encouraged retail trade activity. For the rest of the year, we continue to expect private consumption to decelerate gradually towards healthier rates of expansion.

Services and Hotels

In September 2022, most service-related activities showed solid results, with the strongest growth seen in warehousing and complementary transportation activities (+30.7% y/y). In terms of employment, computer system activities recorded the largest change (+12.8% y/y), followed by warehousing and transportation activities, and restaurant, catering, and bar activities (+9.1 y/y).

In the hospitality sector, revenues showed a 31.1% y/y expansion, lower than that observed in the previous month (36% y/y), and employment growth stood at 24.6% from 28.5% in the previous month. Hotel occupancy was 58%, stable versus the previous month. Business travel continued to show a positive trajectory and was slightly higher than in August, accounting for 22.9% of total occupancy, and leisure travel was 29.6% lower than the previous month since it is a month that is not considered a holiday season.

All in all, there are mixed signals in the performance of activity indicators as confidence surveys show that companies are more negative about the economics outlook amid the impact of inflation and input supplies globally, on top of expectations of higher tax burdens at home.

Our baseline scenario remains that the economy will continue to show robust but moderate growth for the remainder of the year. Our forecast is that GDP growth will be 7.6% in 2022. This includes a gradual slowdown in the second half of 2022, especially from more moderate private consumption as a result of tighter monetary policy. That said, and taking into account the recent stance of BanRep which was again more concerned about inflation than growth, we expect BanRep to continue its hiking cycle in December with at least a 50bps hike at the December 16 meeting to reach a rate of at least 11.5% and do not rule out further hikes given the strong indexation effects for next year, to stay at this higher level for about a half year as inflation starts to show a stronger deceleration.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

MEXICO: BANXICO DELIVER AN EXPECTED 75BPS HIKE, ALTHOUGH UNANIMITY AT THE BOARD HAS ENDED

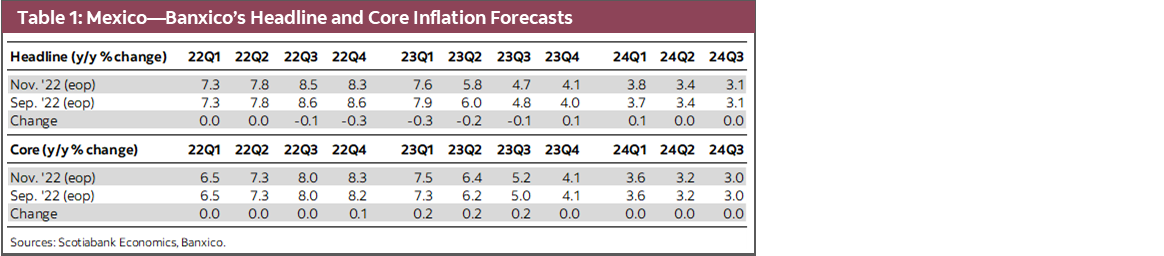

On Thursday, Banxico hiked its policy interest rate by 75bps, as widely expected, to 10.00%, marking four consecutive increases of the same size—although this time it was not a unanimous decision. Banxico’s board settled on a 75bps thanks to a 4-1 vote in its favour with Deputy Governor Gerardo Esquivel opting for a 50bps hike. Forward guidance remained largely unchanged from the previous decision, with Banxico’s statement stressing that it will evaluate “prevailing conditions” in its upcoming decisions. However, this time the board highlighted “the monetary policy stance already attained in its hiking cycle”—thus highlighting the substantial degree of tightening since mid-2021. Additionally, inflation forecasts did not change notably on this occasion (table 1); in fact, inflation expectations for 4Q2022 marginally diminished, while the expectation of convergence to the 3.0% target remained unchanged at 3Q2024. Despite this, the governing board considered that, although some shocks show signs of subsiding, the balance of risks to the inflation trajectory remains biased to the upside.

The statement highlighted the decline in headline inflation in October, which stood at 8.41%, although it mentioned that the fall was led by the non-core component, as core inflation continued its upward trajectory, standing at 8.42%. Thus, Banxico revised slightly lower its short-term headline inflation forecast, to 8.5% on average in Q4-2022, although it left its 3.1% Q3-2024 forecast unchanged. In contrast, the expected trajectory of core inflation rose modestly from 2023, again expecting it to reach 3.0% in Q3-2024.

While headline inflation appears to have settled on a downward trend, the dynamics of core inflation suggest that it is not yet a good time for Banxico to decouple from the Fed's hikes. The least volatile component of inflation and in many ways the most important for monetary policy, core inflation, continued to accelerate in October, albeit by less than anticipated. Still, the statement highlights an upwardly bias balance of risks. Thus, although at least one of its members considers that it is time to differentiate from the Fed's pace of hikes, we do not believe that there are sufficient conditions to do so. In this regard, it is worth mentioning that, although this could be Deputy Governor Esquivel's second-to-last meeting, the member who takes his place could also have a dovish bias. We forecast that Banxico will follow the Fed's December decision with a 50-point hike, to end the year at 10.50%.

For now, we maintain our view of an additional hike in early 2023, leaving policy unchanged for most of the year, to begin a cutting cycle in Q4-2023. Thus, we maintain our end-2023 rate forecast at 10.50%, but with downside risks of a possible decoupling of the Fed's stance sooner than anticipated.

—Miguel Saldaña

PERU: BCRP HIKES 25BPS, LEAVES DOOR OPEN

The board of Peru’s central bank (BCRP) raised its key interest rate by 25bps to 7.25% on Thursday, in line with our expectation and the market consensus, but above what 3-month swaps had indicated (7.00%).

This is the third consecutive time that the BCRP has raised its key interest rate by 25bps, after having hikes of 50bps at each of the previous twelve decisions. We believe that this slowdown in rate hikes suggests that the end of the interest rate hike cycle is near. The key will continue to be the speed with which inflation expectations moderate. The wording of the statement is like the previous statement, which suggests that although data are heading in the right direction, it is probably not convincing enough yet to decisively pause.

Inflation peaked in June (8.8% y/y) and has slowed since. A reflection of this is that October is the fourth month in a row where inflation decelerated, although it has done so at a slower rate than that predicted by the authorities. Other price indices, such as wholesale prices and those linked to construction materials and machinery, continue to slow. In geographical terms, 6 of the 26 largest cities in the country registered year-on-year inflation greater than 10%. This represents a slight increase compared to the 6 cities above 10% in September.

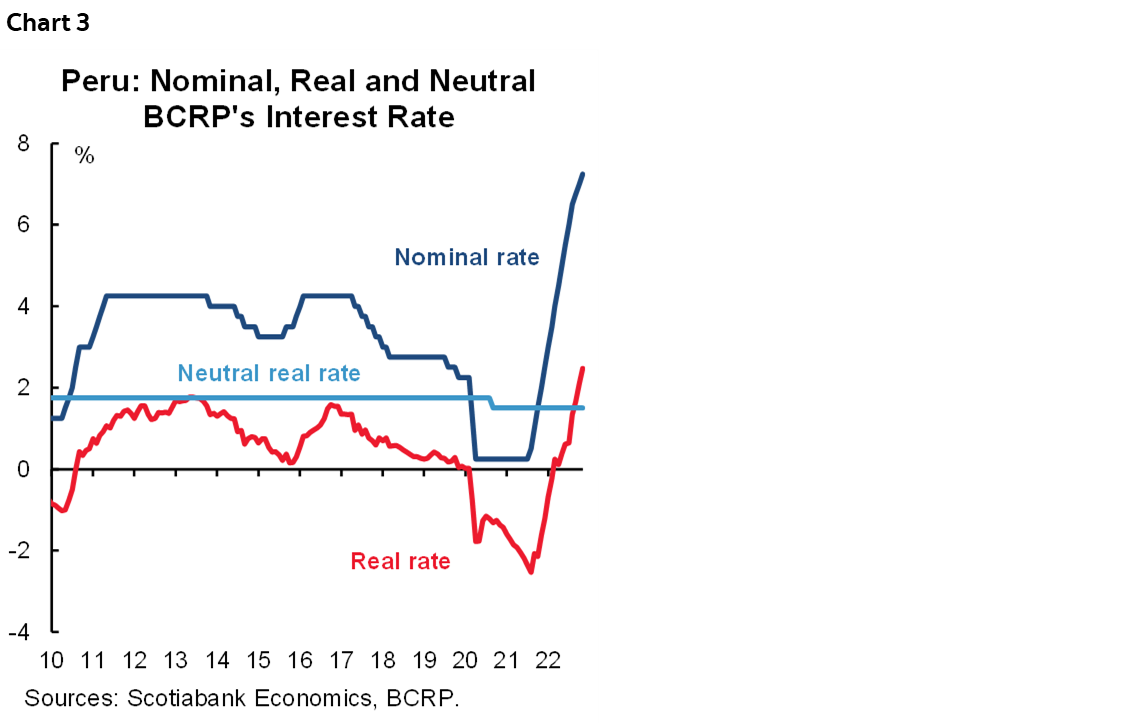

The real interest rate has risen from 2.11% to 2.47%, standing above 1.50% for a third straight month, a level considered neutral by the BCRP (chart 3). It is likely that, due to this, the BCRP’s statement no longer mentioned that the hike continued the “normalization of monetary policy”, now emphasizing that “it continues with the adjustments of the monetary policy position”.

The BCRP kept the forward guidance used in previous statements, which leaves open the possibility of new hikes, depending on how the inflation drivers evolve. Our base scenario projects a terminal rate of 7.25%. This statement results in upside risks to this forecast.

Like us, the central bank forecasts a downward trend in year-on-year inflation, maintaining its expectation of a return to the target range during the second half of 2023, both due to the moderation of the impact of international food and energy prices as well as declining inflation expectations. However, the global price environment is still unstable, so the central bank may continue to make further adjustments.

The statement maintains its pessimistic outlook for global and local economic activity, emphasizing the worsening of global growth expectations for this year and next. It also highlights that, although most of the leading indicators and expectations for Peru's economy recovered in September, most remain in pessimistic territory.

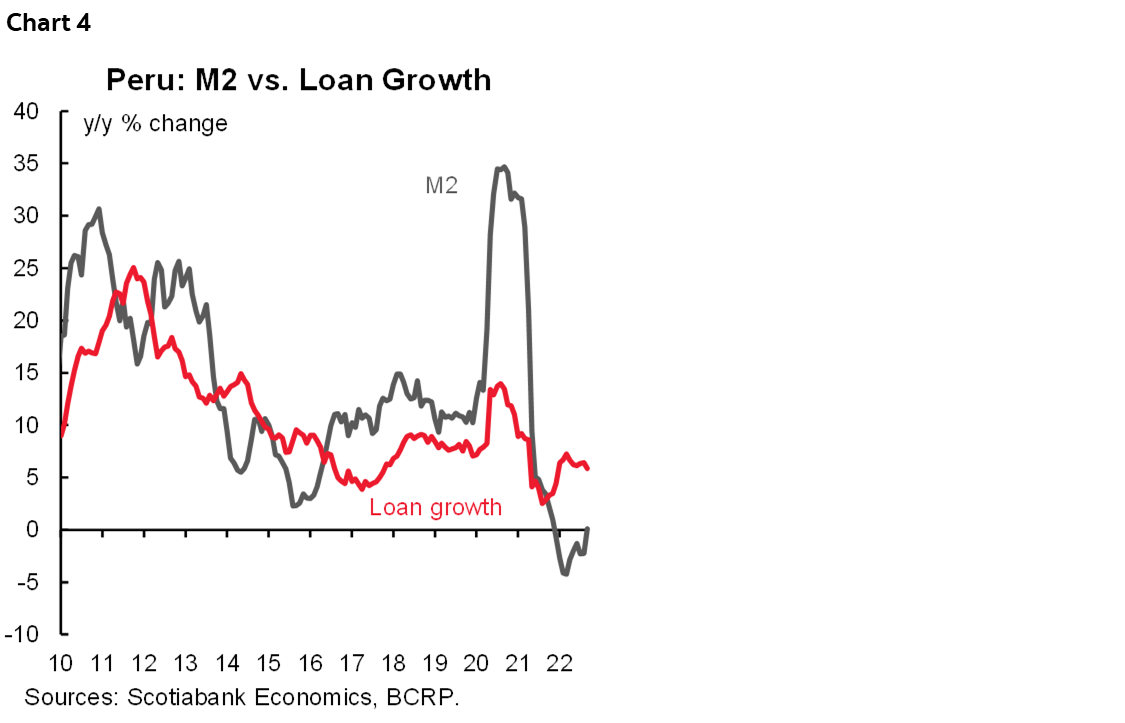

On the quantitative side, growth in the quantity of money (M2) entered positive territory (0.1% y/y in September) for the first time after nine consecutive months of y/y declines (chart 4).

—Ricardo Avila

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.