- Chile: Central Bank raises the benchmark rate by 125 bps to 8.25%

- Colombia: Inflation soars, but stable credit rating confirmed

- Mexico: Forecast revisions despite Mexican government’s plan to deal with inflation

- Peru: Congress approves new private pension fund withdrawal

CHILE: CENTRAL BANK RAISES THE BENCHMARK RATE BY 125 BPS TO 8.25%

I. We expect a terminal benchmark rate at 9.25% and aggressive cuts as global supply shocks wane

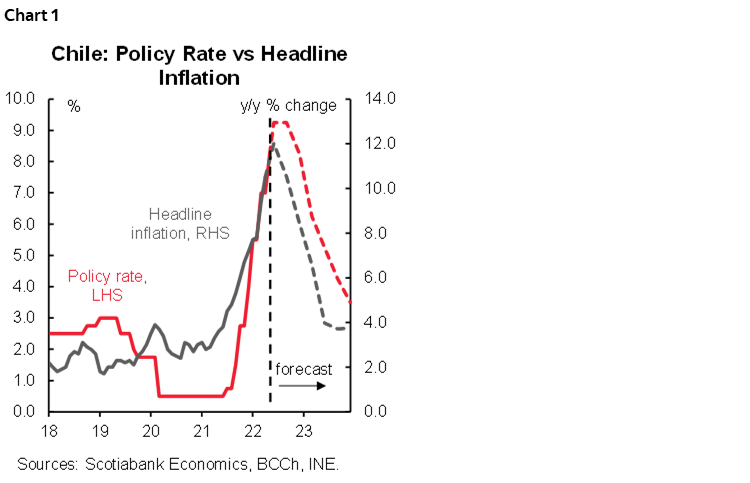

On Thursday, May 5, the central bank (BCCh) hiked the monetary policy rate by 125 basis points (bps), to 8.25%, surprising both market and our expectations. Contrary to our view that caution and lower global growth would likely constrain the increase, the bias of the statement does not seem particularly neutral, and given the size of the increase, the benchmark rate is unlikely to remain at this level. In fact, the BCCh statement makes for a hawkish read, particularly in pointing out that all the recent international and national data are inflationary and the discussion of the board's decision to place the policy rate in the upper part of the rate corridor revealed a few weeks ago in the March Monetary Policy Report. We see a central bank very concerned about local inflation and inflation expectations, and we reassess the terminal rate of this policy cycle towards 9.25% (chart 1).

The statement also reveals concern with respect to the recent nominal depreciation of the Chilean peso (CLP), which contrasts with the fall in the real exchange rate and the limited multilateral depreciation of the CLP.

The BCCh recognizes upward surprises in activity, especially March's monthly GDP growth and inflation, which they point out was significantly higher than that estimated in the Monetary Policy Report. At the same time, the resilience of consumption is noted, while its diagnosis regarding weak private investment is reiterated, especially in the construction sector. The central bank also acknowledges a resurgence of inflationary pressures owing to the increase in volatile prices as well as the recent depreciation of the CLP and the inflationary effects of the lockdown in China. Although inflation excluding volatile components was in line with its baseline scenario, the concern about second-round effects seems to be greater.

Regarding the international scenario, the BCCh appears to be weighing the higher external inflationary pressures resulting from the lockdown in China and the consequent deterioration of the supply chains much more heavily than the reduction in global growth prospects and the fall in the terms of trade. Along these lines, concerns about China's GDP growth and the downward correction in world GDP growth prospects are not viewed as a surprise to its baseline scenario; that is, the reduction in world GDP growth does not seem particularly disinflationary. It should be noted that, after the publication of the March Monetary Policy Report, US GDP contracted in quarterly terms, while the lockdown in China intensified as a result of the increase in Covid-19 cases.

For now, the central bank is focusing on the surprisingly high short-term inflation, with the aim of calming private inflationary expectations, which could lead to a particularly active monetary policy during the coming months. In the case of a slowdown and/or sharp drop in the price of commodities, we do not rule out abrupt reductions in the reference rate in the next few months. The reference made by the Board to a reassessment of the rate corridor in the next June Monetary Policy Report (to be released on June 8) leaves monetary policy without a clear bias that would anchor expectations.

A monetary policy rollercoaster becomes more likely in the second half of 2022. This is because the BCCh has been very active, quickly moving the rate into contractionary territory, and has not hesitated to withdraw monetary stimulus, even above what is reflected in asset prices. However, once the supply shock fully passes and inflation starts to recede locally and globally, it seems very likely that we will see a very active central bank lowering the benchmark rate. The already weak GDP growth that the surveys and the CB itself expect for 2022 and 2023 (2% accumulated) may be even more affected. In this respect, the probability of having a recession in 2023 has increased and the CB will need to be very quick to bring the rate (at least) to neutral ground once signs of slowing inflation emerge.

II. April CPI of 1.4% m/m leaves annual inflation at 10.5%

On Friday, May 6, the statistical agency (INE) released the April CPI inflation, which rose 1.4% m/m (10.5% y/y), above both market and our expectations. These levels of inflation generate significant second-round effects that give rise to inflationary persistence that is not easy to contain. In this context, after two consecutive monthly inflationary surprises, we have revised our inflation scenario for 2022 and 2023, projecting annual inflation in 2022 at 8.4% and in 2023 at 3.7% (before 6.6% and 3.5%, respectively).

Regarding April’s figures, generalized increases were recorded, especially in volatile items, but also at the core level. It is services (without volatile components) that continue to push up inflation, especially food services, home repair, health, recreation and transportation, largely due to the readjustments of past inflation and the persistent increase in costs that are rapidly being passed on by the providers of these services. For their part, goods prices continue to rise, although these increases seem to be concentrated in non-durable goods, beyond the special case of new cars.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

COLOMBIA: INFLATION SOARS, BUT STABLE CREDIT RATING CONFIRMED

I. Headline inflation of 9.23% highest in 21 years

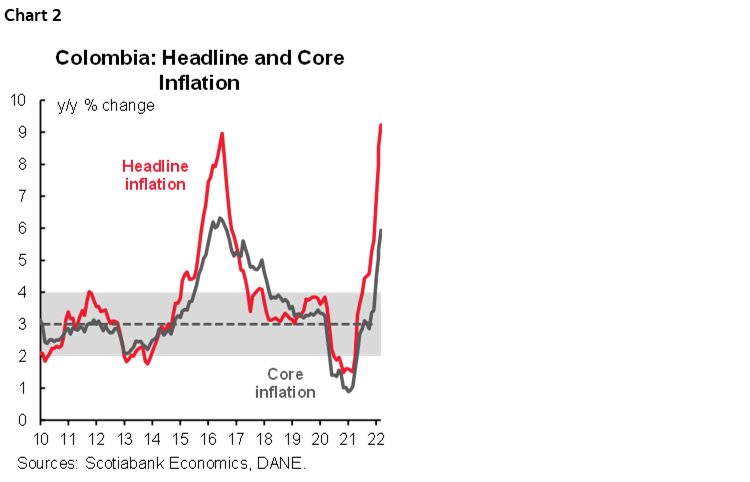

Monthly CPI inflation was 1.25% m/m in April 2022, according to DANE data published on Thursday, May 5, well above the BanRep’s survey (0.78% m/m) and Scotiabank Economics’ projection (1.07% m/m). April’s inflation was almost three times the average monthly inflation observed since 2016 (0.45% m/m) and brings annual headline inflation to the highest level since mid-2000 at 9.23% y/y, up from 8.53% y/y in March (chart 2), and well above BanRep’s target range (2%–4%) for the 19th month in a row. Annual food inflation is at its highest level in recent history at 26.2%.

Core inflation also increased, from 5.31% y/y to 5.94% y/y, the highest since September 2016, while ex-food and regulated goods inflation came in at 5.26% y/y (up from 4.51% of the previous month). These results show that inflation is not only reflecting the effect of supply shocks on food prices but also upside pressures on other key prices owing to indexation effects and the ongoing recovery. In fact, the central bank recently highlighted that consumption credit demand is increasing at an 18% y/y pace, which points to still-strong demand.

We affirm our 100 bps rate hike expectation for June’s monetary policy meeting, as the BanRep board endorsed a gradual approach to tightening monetary conditions is appropriate given the high uncertainty, especially on the economic activity front. We expect May's headline inflation to moderate due to the statistical base effect on the back of the nationwide strike one year ago. However, we will only have confirmation of a downward path after the June and July releases. That said, we expect the hiking cycle to end at 8% in July, with the rate easing to 5.5% by the end of 2023, if inflation moderates in the H2-2022 and during 2023.

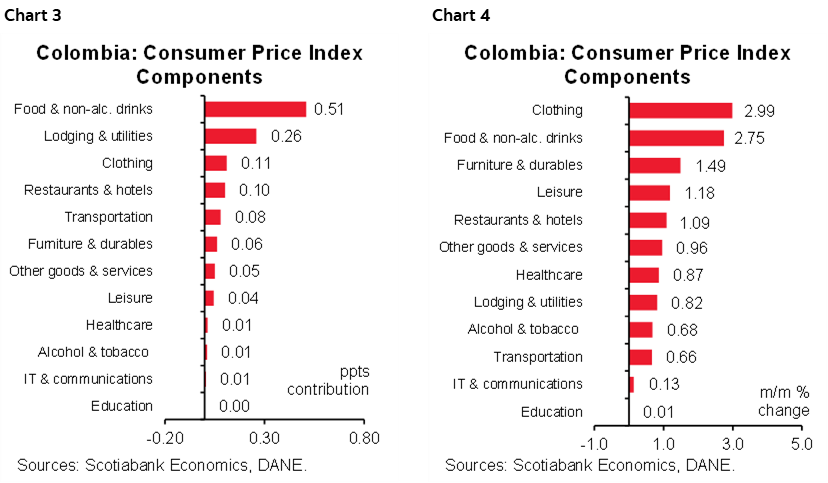

Looking at April’s numbers in detail, all 12 components of the CPI index contributed to higher inflation (charts 3 and 4), with foodstuffs once again posting the highest gains.

The main highlights are:

- Foodstuffs had the largest contribution (+51 bps), with inflation of +2.75% m/m, coming from rice (+7 bps), milk (+6 bps), and meat (+6bps), with other products showing upside pressures from higher input prices. Food inflation reached a new record level reaching 26.2 % y/y. In March, the PPI showed high pressures on fertilizers that are likely to continue to be reflected in the CPI numbers in forthcoming months.

- Food inflation will have a high statistical base in May resulting from the nationwide strike in 2021, which led to a 5.37% m/m increase. This base effect should contribute to a decrease in the headline inflation. However, if food inflation remains above an average of 0.80% m/m for the rest of the year, inflation would continue accelerating after June. In this respect, the risk of closing 2022 with inflation above 8% has increased, which would lead to higher indexation effects that would delay the expected y/y reduction of inflation in 2023.

- Lodging and utilities (+19bps) were the second-largest contributors to headline inflation. In April, rents rose 0.47% m/m, reflecting indexation effects. It is worth noting that in 2022 we are experiencing a stronger indexation than in a regular year. Utility fees jumped by 1.99% m/m, led by electricity (+1.93% m/m), and gas (+3.80% m/m). These increases concern us, since they could continue to push inflation up as indexation rules are consistently triggered.

- Other components recorded monthly inflation at above pre-pandemic averages. Cleaning-related goods continued contributing to price pressures owing to higher input prices.

- Clothing had a positive contribution due to a reversal effect of the VAT holiday in March. However, higher input prices and the strong demand recovery due to in-person activities are also leading to higher prices.

Looking at annual inflation across major categories, goods inflation jumped more than 100 bps to 7.82% y/y in April, while services increased from 3.79% y/y to 4.29% y/y. Regulated-price inflation increased from 8.26% y/y to 8.32% y/y.

All in all, April inflation paints a worrying picture. It came in well above market consensus and, in our opinion, also above the central bank’s expectation. Foodstuff inflation contributed the 40% of total inflation, which is lower than what was observed the previous month. That said, the rest of the CPI components are also reflecting significant upside pressures from higher input prices, supported by strong domestic demand. In May, the VAT holiday will contribute to moderating the headline inflation, however, upside risks ahead in H2-2022 remain high. For now, we expect the central bank to continue hiking the monetary policy rate until 8%. We think a 150 bps hike will be under discussion ahead of June meeting, but for now we affirm our 100 bps call.

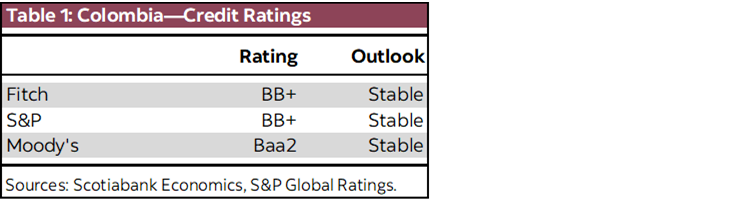

II. S&P affirms Colombia’s rating at BB+ outlook “stable”

On Thursday, May 5, S&P Global Ratings affirmed Colombia’s rating at BB+ (one notch below investment grade) with an outlook of “stable”. S&P emphasized that they expect continuity in the macroeconomic framework following the elections, which with better economic growth will help to stabilize the debt burden. The “stable” outlook reflects the expectation of a reduction in the government debt-to-GDP ratio at around 60% of GDP over the next two to three years.

While the announcement is good news, there is still a long way to go before investment grade is restored. According to S&P, an upgrade would require significantly better-than-expected growth in the next 24 months together with structural measures to diversify exports and reduce the fiscal deficit.

Some highlights include:

- S&P would view a Congressional elections result in which no party is close to a simple majority in any chamber as a favourable outcome. Such a configuration would ensure policy continuity, limiting policy changes regardless of the political orientation of the new government.

- Economic growth exceeded expectations and average growth is expected around 3% in the medium term. High inflation and global economic slowdown are downside risks.

- S&P anticipates a correction in the fiscal deficit, however, government expenditure as a share of GDP will remain above pre-pandemic levels.

- The current account is a negative. S&P expects a current account deficit of 4.4% of GDP as a result of higher commodity prices and better economic growth. However, this metric still is pointing to a weak external position.

Our take:

S&P's affirmation of a stable rating is probably a non-event. More important, S&P is also affirming its confidence in the country’s institutional framework, which is positive news ahead of the first round of presidential elections on May 29. This assessment is compatible with our perspective that the next President, whoever that may be, will have to negotiate with a very diverse Congress, making abrupt economic policy changes less likely.

—Sergio Olarte, Maria Mejía, & Jackeline Piraján

MEXICO: FORECAST REVISIONS DESPITE MEXICAN GOVERNMENT’S PLAN TO DEAL WITH INFLATION

On Wednesday, May 4, the Mexican government announced an agreement with private companies on 16 measures designed to contain inflation. The plan, which is called package against inflation and scarcity or PACIC (Paquete Contra la Inflación y la Carestía), is expected to last at least six months. The measures include: standardizing the price of 24 basic products nationwide, eliminating import tariffs on 21 basic food basket products and 5 inputs, stabilizing production and distribution costs by slowing the increase in railroad rates, highway tolls and gasoline, diesel, LP gas and electricity prices, among other measures.

In our opinion, the federal government overestimates the positive effect that the plan may have on inflation, both in the short and medium term. Additionally, no mention was made of the negative effect that the PACIC will have on public finances. So, despite these measures, we are revising upwards our year-end forecasts: for 2022 we expect inflation to reach 6.50% and for 2023 5.10%. We will be attentive to Banxico’s monetary policy decision next week and expect another 50 bps increase to 7.00%. We are also revising our year-end estimates for Banxico’s rate: for 2022 we now expect 8.50% and for 2023 9.00%.

—Luisa Valle

PERU: CONGRESS APPROVES NEW PRIVATE PENSION FUND WITHDRAWAL

You could see it coming. At midnight on Wednesday, May 4, Congress approved a bill that allows individuals to withdraw up to PEN 18,400 (USD 4,900) from private pension funds. This would be the sixth withdrawal that has been authorized since the pandemic began. The bill was approved with a large majority, with 107 votes in favor, 8 against and 2 abstentions. Now it will go to the Executive Branch, which has up to 15 days in which to approve the legislation.

The finance minister has indicated that he will oppose the measure in the Council of Ministers. It is not clear this is the position of the cabinet, although of the three pension withdrawal initiatives initiated by Congress, two were opposed by the Executive. If so, it would go back to Congress, where it is very likely that it will be approved “by way of insistence” as has happened in the past, given the high level of support for the proposal (107 versus the 66 votes required to override).

Once the law is published, the bank regulator (SBS) has a period of up to 15 days to determine the operating procedure—regulation with the respective schedule—to start the withdrawal. Considering these deadlines, it is possible that the withdrawal will start in June.

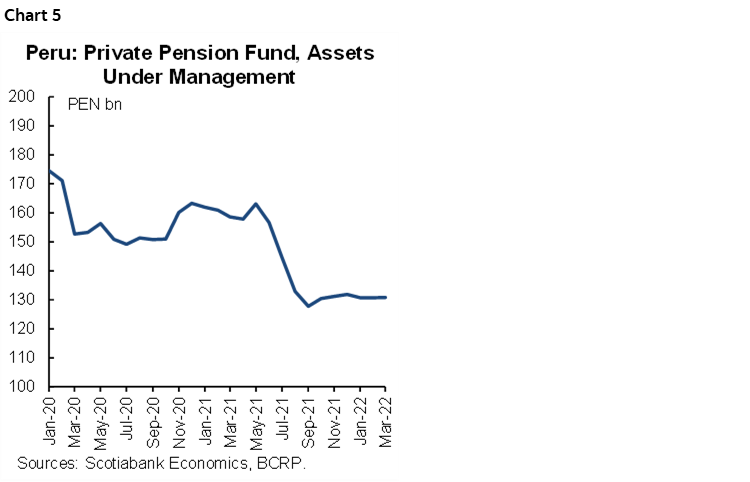

The bank regulator estimates that this new round of withdrawals could reach close to PEN 30bn (USD 7.9bn), which is equivalent to between 20% and 25% of AUM (chart 5). This amount makes it likely that the private pension funds will need to convert part of their portfolio into liquidity through asset sales, as in previous withdrawals, and could require specific liquidity measures by the central bank, already provided on previous occasions, such as repos sovereign bond facilities. The five previous withdrawals total PEN 65.9bn (USD 17bn), equivalent to 8.1% GDP, and were made by 5.7 million affiliates.

The bill sends a negative signal with respect to governability because it reinforces the populist orientation of Congress, adding to that of the government. At the same time, it weakens one of the sources of long-term financing of the country, as argued by the MoF, central bank and SBS. However, in the short term it could further boost consumption already fueled by previous withdrawals, which in the current context of high inflation would help maintain purchasing power but at the cost of keeping inflation high.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.