- Chile: Unemployment rate drops to 7.7%

- Peru: The Attorney General opens an investigation on President Castillo

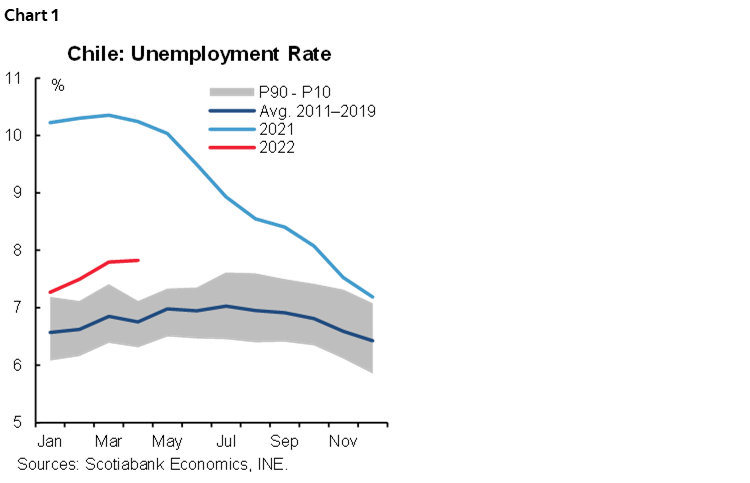

CHILE: UNEMPLOYMENT RATE DROPS TO 7.7%

Job creation everywhere—except construction. On Monday, May 30, the statistical agency (INE) announced that the unemployment rate for the three months ending in April fell to 7.7% (chart 1). The drop from the previous three-month period reflects employment growth (0.43% m/m; 38k) that exceeded labour force growth (0.38% m/m; 36k), as job creation, especially formal jobs, absorbed the effects of increased labour force participation.

Formal employment closed the gap with respect to its pre-pandemic level. The incentives given by the government since last year through the labour Emergency Family Income (IFE), which continues through the end of the year, likely contributed to this recovery. In contrast, the informal employment gap has increased in recent months owing to the employment losses in agricultural and some services. Although 2k informal jobs were created, the gap reached 230k jobs, with a total gap of 228k (chart 2).

In recent months, the workforce has shown greater dynamism than would be expected based on seasonal factors, with monthly growth rates higher than those observed in recent years. The labour market has therefore been able to maintain a rate of job creation that absorbs part of the increase in the workforce, allowing the unemployment rate to remain near its historically observed levels. In the coming months, however, the unemployment rate will likely increase for seasonal reasons. In this context, the challenge will be to maintain the pace of job creation as labour participation rises with increased openness and the end of employment support programs.

At the sectoral level, jobs were created throughout the economy, except for construction. Job creation was driven by services, especially salaried employment linked to investment (professional activities), along with manufacturing and mining. Although the agricultural sector lost employment, job losses were less than expected based on seasonal factors.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

PERU: THE ATTORNEY GENERAL OPENS AN INVESTIGATION ON PRESIDENT CASTILLO

It’s not easy focusing on economics in Peru, as politics always seems to get in the way. Over the weekend, the Attorney General, AG (Fiscal de la Nación) Pablo Sánchez announced that he had opened an investigation into allegations of malfeasance against President Castillo. The decision came after a person under the protected witness program testified that President Castillo was using the Provías road-building program to award projects to companies that had supported his candidacy. The same witnessed also stated that it was his understanding that in November or December President Castillo received PEN 30,000 from a construction businessman who is also currently under investigation for malfeasance with respect to government projects.

Although President Castillo cannot be indicted while he is in office, under the new AG Sánchez, he can be investigated. Sánchez has been in office since March 20, when he replaced the former AG, Zoraida Avalos. He brought with him a change in policy. While Avalos had refused to investigate President Castillo under the argument that, as President, Castillo could not be indicted until his term ended, Sánchez has proceeded to open an investigation arguing that the Constitution mandates the AG office to investigate potential acts of criminal activity.

Though the investigation cannot lead to an indictment, it can reveal information that could conceivably lead to President Castillo being impeached by Congress. This would not be a simple matter under the current make up of Congress, however. The two previous impeachment initiatives in Congress were blocked by the left with the votes of a contingent of non-aligned members of interest groups. Both could conceivably continue to support President Castillo, as long as there is a perceived political advantage to doing so. But, then again, votes in Congress can be fickle.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.