- Colombia: Leftist candidate Petro and populist Hernández in runoff for Colombia’s presidency

- Chile: We project May’s CPI at 0.98% m/m (11.3% y/y)

COLOMBIA: LEFTIST CANDIDATE PETRO AND POPULIST HERNÁNDEZ IN RUNOFF FOR COLOMBIA’S PRESIDENCY

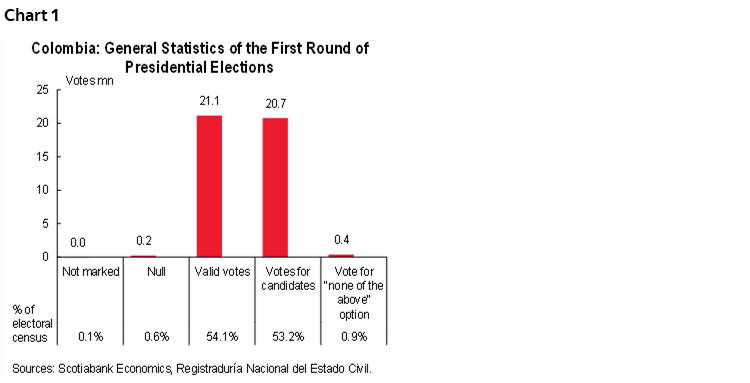

Colombia held the first round of presidential elections on May 29 and with 99.82% of votes counted, the turnout was 54.8% (21.39 million votes, chart 1), slightly above the 54.22% level observed in the 2018 presidential election 54.22% (19.64 million). The votes required to win the presidency in the first round was thus 10.70 million votes.

While Gustavo Petro received 8.50 million votes (40.32%), his lead was insufficient for a first round victory. The big surprise of this election was the independent candidate, engineer Rodolfo Hernández, who benefited from a sudden spike in popularity in the last two weeks of the campaign. Hernández got 5.94 million votes (28.19%) and defeated the centre-right candidate, Federico Gutiérrez, in key areas including Bogota. We expect the majority of Gutiérrez’s 5.03 million votes (23.87%) will now swing to Hernández. In fact, Gutiérrez has said that he will vote for Hernández in the runoff. Sergio Fajardo was the fourth candidate getting 0.9 million votes (4.20%), vanishing in the political spectrum.

The main conclusion of Sunday’s vote is that, while Gustavo Petro represents the left and Hernández advocates an alternative business-friendly approach, both candidates in the final round represent a break with traditional politics.

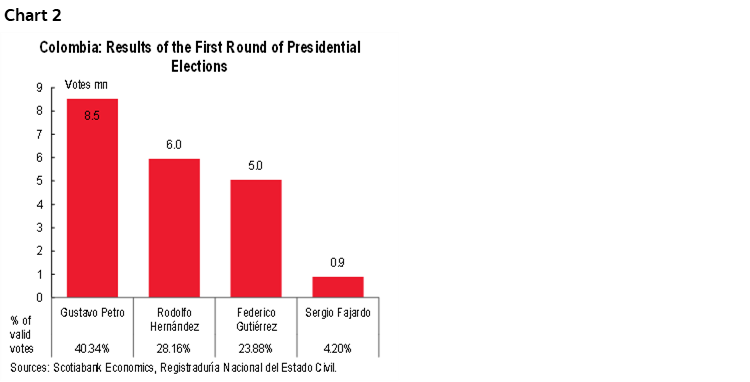

Key takeaways from the first-round results (chart 2) include:

- Petro failed to win the presidency in the first round, coming up short by around 10 ppts. However, he surpassed his vote count in the first round in 2018 (4.86 million votes), the runoff in 2018 (8.04 million votes), and the votes cast for the Pacto Histórico in the primaries on March 13 (5.85 million). The potential to grow could be limited unless participation increases significantly in the runoff, something that is unusual in the country.

- The performance of Hernández was the biggest surprise. His popularity increased days before the elections, with the main campaign theme of fighting corruption appealing to voters. A Hernández presidency wouldn’t entail a sharp turn to the left, but instead likely focus on promoting economic activity to further social progress. While respect for institutions would be maintained, it would be interesting to see how he would govern given that he has no political alliances.

- Gutiérrez’s defeat not only punishes the traditional parties, but also repudiates the current government, whose unpopularity surpasses 70%.

- Petro’s advantage over Hernández is around 2.56 million votes, an advantage that represents half the votes obtained by Gutiérrez (5.03 million votes). But with the majority of Gutiérrez’s voters expected to turn to Hernández, the candidate favoured to win the June 19 run-off election is Rodolfo Hernández.

What is next?

We expect both campaigns will concentrate on providing more information on policy positions in the coming three weeks, especially the Hernández campaign, which did not participate strongly in earlier debates. It also will be key to see how alliances will formed. In the case of Hernández, the potential to grow in votes is stronger, as we think more Gutiérrez voters are likely to vote “against” Petro in the runoff.

—Sergio Olarte, Maria (Tatiana) Mejía, & Jackeline Piraján

CHILE: WE PROJECT MAY’S CPI AT 0.98% M/M (11.3% Y/Y)

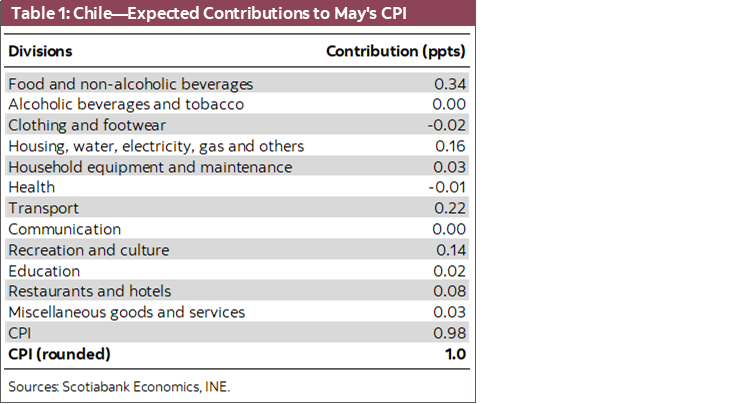

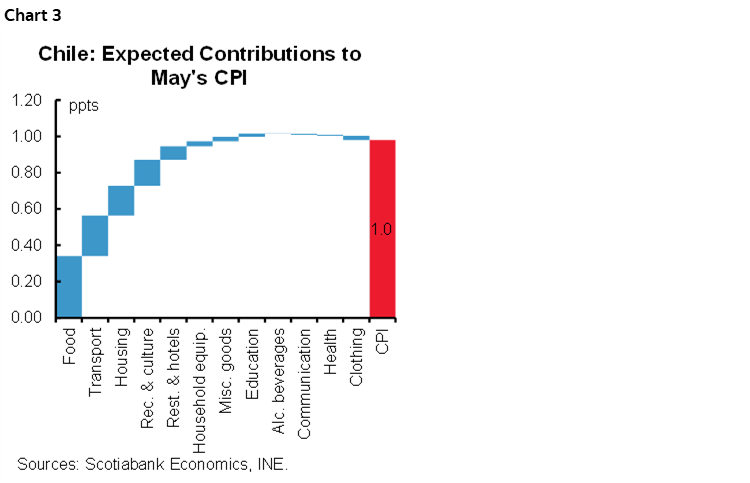

Volatile items may account for more than 60% of May inflation. We project inflation in May will come in at 0.98% m/m (11.3% y/y), above that expected by the Economic Expectations Survey (0.9% m/m) and below that reflected in the Financial Operators Survey (1.1% m/m) and the forward market (1.2% m/m). We estimate the CPI excluding volatile components will increase 0.6% m/m (compared to 1.1% in April), once again revealing that a large part of inflation is explained by these items (table 1). With this, we expect May CPI excluding volatile items is likely to rise 0.8% m/m, while service prices could rise 0.4% m/m. The dispersion of higher price pressures across the consumption basket dropped somewhat but remains high at 59%, placing it in the upper part of the range of recent years.

Food inflation is likely to continue in May, mainly owing to increases in the prices of non-perishables, edible oils, and dairy products (chart 3). Based on our sampling, we estimate that the statistical agency (INE) will record higher prices for bread, rice, among other foodstuffs. Likewise, higher prices for milk, cheese, and derivative goods are likely to push the food component of the CPI basket up 1.6% m/m (incidence of 0.34 percentage points), an increase that would once again be the highest in recent years.

Meanwhile, higher prices for new automobiles, air transport and gasoline will result in an increase in the transport component. We expect higher prices of new vehicles, particularly the best sellers, that would lead to 11 consecutive months of price rises in this item. Increases in air transport fares, mainly for international routes on high season dates, are also likely. Gasoline and diesel prices have been raised on a weekly basis in May, albeit constrained by the operation of the stabilization mechanism that limits the incidence of price hikes to around 0.1 percentage points. Meanwhile, the drop in the price of kerosene announced by the government for the last week of May (around 20%) will have a downward, but limited, effect on inflation in June.

Services would have continued to add to inflation in May, mainly related to restaurant services. We anticipate increases in food consumed outside the home and in dishes prepared to take away, to reach historical highs in May. Finally, seasonal declines in clothing and footwear prices have been observed as the end of the summer season approaches.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.