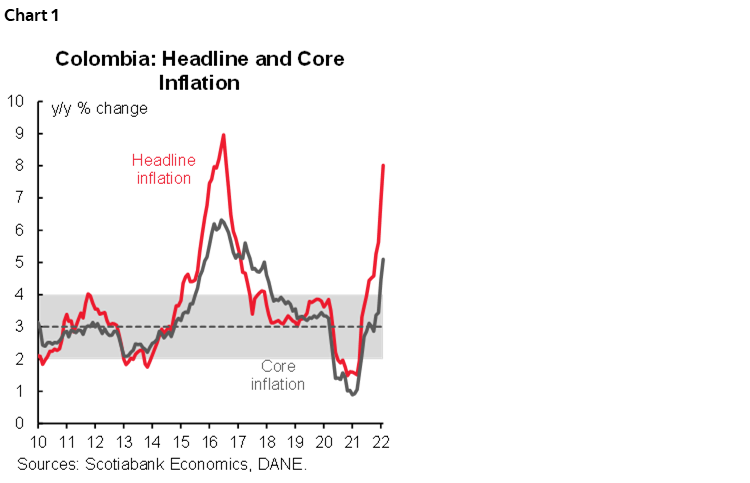

- Colombia: Headline inflation hits 8.01% y/y, with core inflation well above target

- Mexico: Consumption, investment and auto numbers provide a mixed outlook

COLOMBIA: HEADLINE INFLATION HITS 8.01% Y/Y, WITH CORE INFLATION WELL ABOVE TARGET

Monthly CPI inflation was 1.63% m/m in February 2022, according to DANE data published on Saturday, March 5, well above the median forecast in BanRep’s survey (1.23% m/m), and Scotiabank Economics’ projection (1.27% m/m). February’s inflation was twice the average observed since 2009 (0.76% m/m) and brings annual headline inflation to 8.01% y/y, the highest since mid-2016, up from 6.95% y/y in January (chart 1), and above BanRep’s target range (2%–4%) for the seventh month in a row.

Core inflation also increased, from 4.47% y/y to 5.01% y/y, while ex-food and regulated goods inflation came in at 4.14% y/y (up from 3.47 % the previous month). Inflation not only reflects the effect of supply shocks on food prices, but also upside pressures on other key prices as the economy recovers, as well as indexation effects.

We affirm our expectation of at least a 125 bps rate hike in March’s monetary policy meeting. The near-term inflation outlook is subject to several factors. In March, inflation will include the downside effect of the VAT holiday (March 11), and still material upside pressures on food prices. Meanwhile, the possibility remains that inflation could start a downward trend in May. The current environment is challenging for the central bank, however, since inflation risks remain on the upside while economic activity could slow as higher prices affect private consumption and election uncertainty looms. Regardless, we think the inflation targeting mandate will prevail and the central bank will consider overshooting the neutral level. Our expectation of the monetary policy rate for December 2022 is 6.50%, with the rate easing to 5% by the end of 2023.

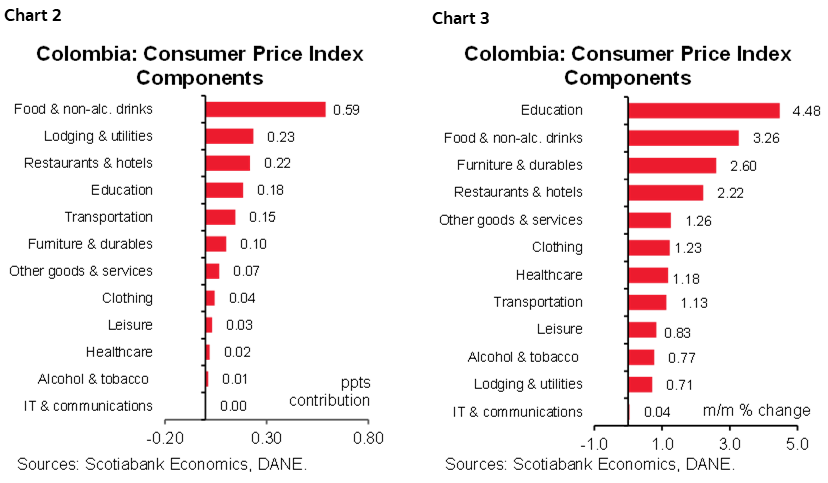

Looking at the February’s numbers in detail, all components contributed to higher inflation (charts 2 and 3), with foodstuffs once again posting the highest gains. The main highlights are:

- Foodstuffs had the largest contribution (+59 bps), with inflation of +3.26% m/m, coming from milk (+4.25% m/m), potatoes (+16.14% m/m), fruits (+5.70% m/m) and rise (+4.26% m/m). Rising input prices and FX depreciation are exacerbating food prices. In some cases, products are increasing faster than in last year’s nationwide strike.

- Lodging and utilities (+23 bps) were the second largest contributors to inflation. In February, rents rose 0.41% m/m, above the 0.26% m/m increase in January, reflecting indexation effects. Utility fees jumped by 1.66% m/m, led by electricity (+2.62% m/m), gas (+2.20% m/m), and garbage collection (+1.41% m/m), with the last component showing the effect of the minimum wage hike.

- Education fees increased by 4.48% m/m, below our projection, but at a rate similar to that observed in pre-pandemic periods. However, DANE noted that some educational establishments have still not reported fees, which could lead to further positive contribution in forthcoming months. Meanwhile, elementary school fees rose at a below-pre-pandemic pace, providing some relief to inflationary pressures.

- Other components recorded monthly inflation at above pre-pandemic averages. Clothing had a residual effect from the normalization after the last year’s VAT holiday. In addition, some cleaning-related goods also contributed to price pressures owing to higher input prices.

Looking at annual inflation across major categories, goods inflation jumped to 5.98% y/y in February, while services increased by 61 bps from 2.79% y/y to 3.40% y/y. Regulated-price inflation rose 59 bps to 8.91% y/y.

All in all, 35% of total inflation was explained by food inflation, with the rest attributable to a combination of higher input prices, FX effects on tradable goods, and indexation of rent and educational fees. Year-end inflation would exceed 6% if inflation pressures remain. That said, the monetary policy rate will keep rising, with a 125 bps hike in the March 31 meeting, to end 2022 at 6.50%. However, we anticipate rates start to ease in early in 2023 as inflation returns to target.

—Sergio Olarte & Jackeline Piraján

MEXICO: CONSUMPTION, INVESTMENT AND AUTO NUMBERS PROVIDE A MIXED OUTLOOK

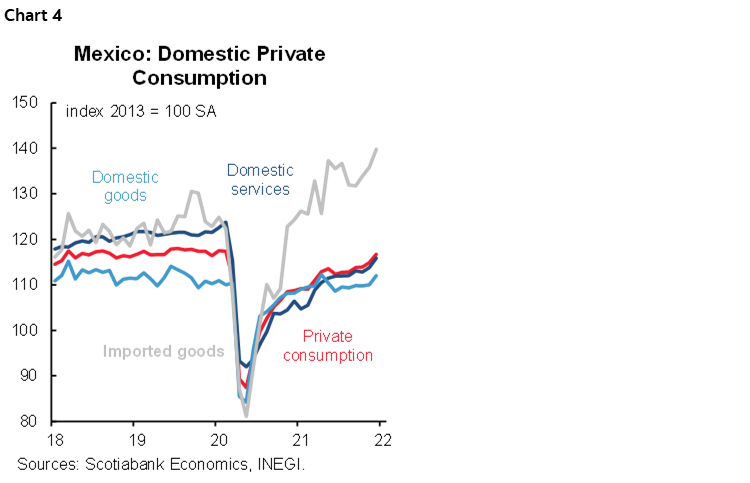

I. Consumption keeps its upward trend, already above pre-pandemic levels

Consumption accelerated in annual terms in December to 7.7% y/y from 7.4% y/y, measured on a non-seasonally adjusted basis (chart 4). Seasonally adjusted, consumption rose from 0.7% m/m to 1.5% m/m, with increases in all its components. Domestic goods accelerated from 0.1% m/m to 1.7% m/m, services from 0.9% m/m to 1.4% m/m, and imported goods from 1.3% m/m to 2.2% m/m. In general terms, consumption is already above pre-pandemic levels, with a stronger recovery in goods than in services reflecting the risks in contact-intensive activities in the pandemic.

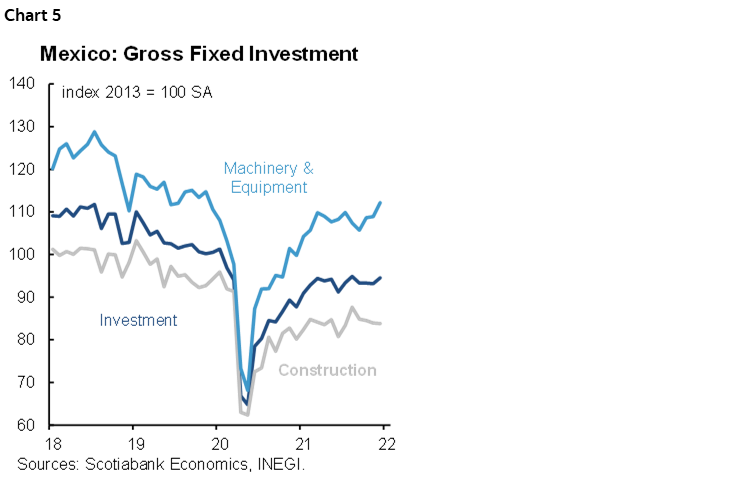

II. Investment for December recovered modestly, but remains weak

Gross fixed investment for December accelerated to 8.1% y/y, exceeding the expected figure of 5.5% and the previous figure of 5.9% (chart 5). Investment has now grown 10 consecutive periods on a y/y basis, but still remains below pre-pandemic levels. Construction increased 4.2% y/y in December, with machinery and equipment up 13.1% y/y and imported goods growing 19.5% y/y. Meanwhile, residential construction has posted three consecutive monthly declines. In monthly terms, investment grew 1.2% m/m. Construction was unchanged from the previous month, while machinery and equipment increased 2.2% m/m. Investment continues to be one of the major obstacles to economic recovery, and may be held back by the complicated relationship between the public and private sectors.

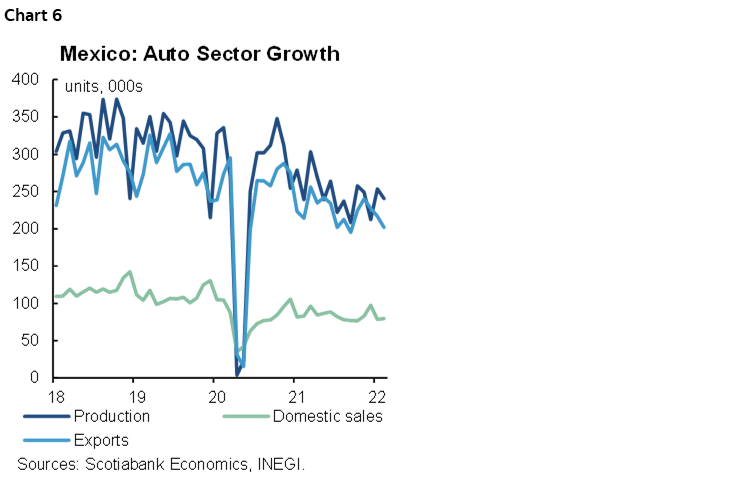

III. Automotive industry limited by input and inventory scarcity

Preliminary numbers show that 79,600 light vehicles were sold in February, the lowest level for the month since 2012 (chart 6). Final automotive industry figures point to a slight recovery in production, though signs of weak demand and disruptions in the value chains remain. Production rebounded from -9.1% to 0.7% y/y, while exports extended their decline from -3.1% to -5.7% y/y and domestic sales went from -3.8% to -3.9% y/y. In the January–February period, production totaled 493 thousand units assembled, its lowest level since 2014. Meanwhile, exports were 418 thousand and domestic sales 158 thousand, the lowest levels since 2015 and 2013, respectively.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.