- Peru: Mining conflicts flare up again

PERU: MINING CONFLICTS FLARE UP AGAIN

Mining conflicts escalated this week. On Monday, installations at the Las Bambas copper operations were damaged, and on Tuesday Southern Peru’s Los Chancas copper project came under attack.

Las Bambas

The conflict at Las Bambas has been ongoing since April. On April 20, MMG Limited (China), which operates Las Bambas, announced that it was halting its operations following a land takeover by local groups of Las Bambas property near to its operations. Conflicts escalated this week in a confusing succession of events. To the best of our understanding, based on press reports, on May 31 a group of informal miners were allowed by local communities to enter the Chalcobamba sector of Las Bambas, damaging property. Chalcobamba is located 4km from the mining operations and processing plants. The following day, the police attempted to dislodge the occupying groups. At the same time, apparently, maintenance crews accompanied by police attempted to gain access to the water treatment plant to clear it of sludge which, after lacking maintenance for nearly 50 days, has become an environmental concern. Both events produced clashes between the police and the groups inside Las Bambas. Later Tuesday night, these groups damaged company installations and equipment.

Informal miners may be trying to prevent Las Bambas from developing the Chalcobamba sector, which is close to their own activities. On 24 March 2022, MMG Limited had announced that it had received regulatory approval from the Peru Ministry of Energy and Mines (MINEM) for the development of the Chalcobamba pit and associated infrastructure at Las Bambas.

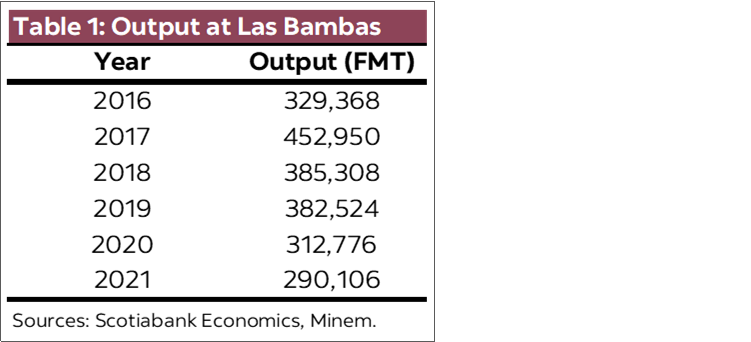

The Las Bambas operations reached a maximum output of nearly 450,000 tons in 2017. It has not been able to repeat this level, however, as it has continually faced social conflicts which led to temporary halts in production (aside from the impact of COVID lockdowns in 2020). Operations were severely affected by conflict in 2021, when operations had to be halted for over 100 days.

Operations are currently located at the Ferrobamba pit, while Chalcobamba Phase I is under development. Chalcobamba I, located approximately four kilometers northwest of the Las Bambas processing plant, is expected to compensate for lower metal grades at current operations, and allow production levels at Las Bambas to remain at 380,000 to 400,000 tons of copper in concentrate per annum over the medium term (table 1).

We estimate that the 43 days during which Las Bambas has halted production since April 20 are having the following consequences:

- Daily losses of at least US$ 8.5 million in export sales.

- An output loss, so far, of approximately 35,000 tons of copper, which will increase as the mine lockdown continues. The company’s production target of between 300,000–320,000 tons of copper concentrate in 2022 is at risk. Current events are likely to lead to a delay in developing the Chalcobamba mine.

- Peru’s copper export levels for April, May, and probably June, will be affected, although this may be less visible due to high prices.

Note also that Las Bambas copper output represents approximately 0.8% of Peru’s GDP. However, this is already factored in our GDP forecast of 2.6% for 2022. Las Bambas production represents 2% of the world's copper supply and around 15% of Peru's copper production.

Los Chancas

The second event occurred at Southern Copper Corporation Peru’s Los Chancas project’s property and installations. According to press reports, a group of informal miners entered Los Chancas property and damaged installations. Los Chancas is a USD2.6 bn copper project that we do not expect to begin production before 2026. The project is scheduled to start construction in 2024, according to the Ministry of Mines. However, permits are still lacking, and the project has yet to produce an Environmental Impact Report.

Los Chancas is located near the Las Bambas Chalcobamba project and faces a similar local socio-political environment. This raises the possibility that the Monday event by informal miners at Chalcobamba, and the Tuesday event at Los Chancas, may be linked. It is our understanding that both projects are in a region that is very mineral rich, and has attracted informal miners.

What does this all mean?

The recent events do not affect copper production more than has already been occurring, as Las Bambas had already halted production, and Los Chancas had not begun.

However, these events reveal the high degree of hostility that exists surrounding mining operations in this region of Apurímac. Such hostility implies, in turn, that the conflict may be protracted.

The recurrence of mining conflicts strengthens our opinion with respect to the challenges to mining investments in Peru, and that once the current generation of ongoing projects ends, new projects of significance may not emerge to replace them, at least until the Castillo government ends.

It is our perception that protesters have greater bargaining power today, as the government has been permissive with protests, frequently siding with protesters. Moreover, the government has not shown initiative, urgency or capacity in attempting to resolve mining conflicts.

There is a risk that mining conflicts may extend. Nearly 40% of copper production capacity has been under pressure at some point or another in the last two years due to protests. That said, most protests are relatively short-lived (Las Bambas is the exception).

To put all this in perspective, we continue to expect mining GDP to grow 3.9% in 2022 (Quellaveco comes online in Q4), although this is lower than the 5.5%–6.0% mining growth we initially expected.

—Guillermo Arbe & Katherine Salazar

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.