- Colombia: Strong growth heralds pandemic recovery; BanRep’s expectations survey signals inflation risks

- Peru: GDP grew 13.3% in 2021, as expected

COLOMBIA: STRONG GROWTH HERALDS PANDEMIC RECOVERY; BANREP’S EXPECTATIONS SURVEY SIGNALS INFLATION RISKS

I. 10.6% growth in 2021, with only mining and construction lagging recovery

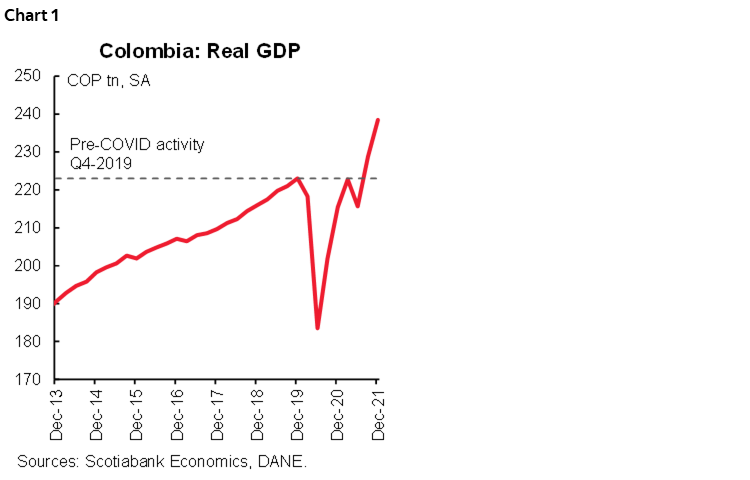

Data released on Tuesday, February 15 by Colombia’s statistical agency, DANE, show Colombia’s real GDP grew by 10.8% y/y in Q4-2021, above both consensus (9.3% y/y according to Bloomberg) and our own forecast of 9% y/y. Growth was 4.3% in quarterly seasonally adjusted terms, with positive contributions from services-related sectors. Colombia grew 10.6% in 2021 as a whole and on average, operated 2.8% above pre-pandemic levels (chart 1). In contrast, total employment closed 2021 4% below the pre-pandemic 2019 levels.

The strong growth results reflect the positive response of the economy to the mid-year relaxation of mobility restrictions and were powered by a strong contribution from private consumption. Investment continued to lag the recovery. Looking ahead, we expect a slowdown in consumption to more sustainable levels in 2022, while investment picks up on increased construction activity. For now, our 4.5% GDP growth forecast for 2022 is skewed to the upside. And with the pre-pandemic output level achieved, employment recovery is key to sustained growth.

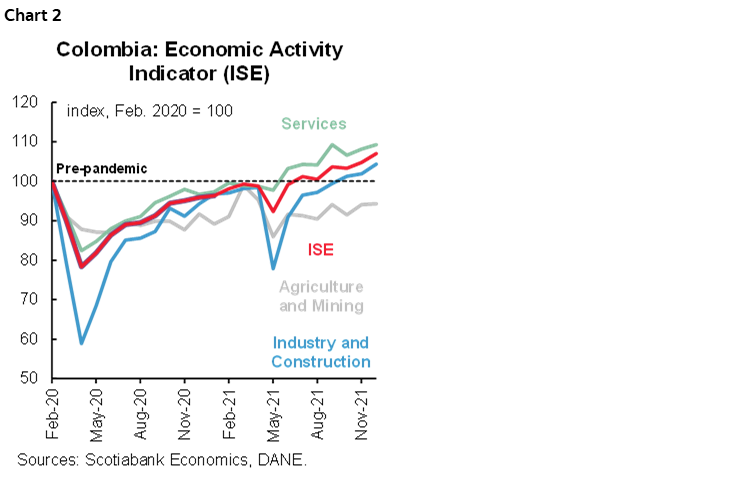

According to the monthly indicator (ISE), economic activity rebounded 11.8% y/y in December (+2.2% m/m sa), to close a robust quarter a solid 7% above the pre-pandemic level in February 2020 (chart 2). The largest gains were in the industrial and construction sectors (+2.4% m/m), and services-related sectors (+1.0% m/m). Construction (+1.4% m/m) is showing better gains, which supported the good performance of industry (+1.7% m/m), while in the services sector, commerce, transport & hotels (+0.4% m/m), public sector (+4.3% m/m) and leisure (5.9% m/m) led the gains.

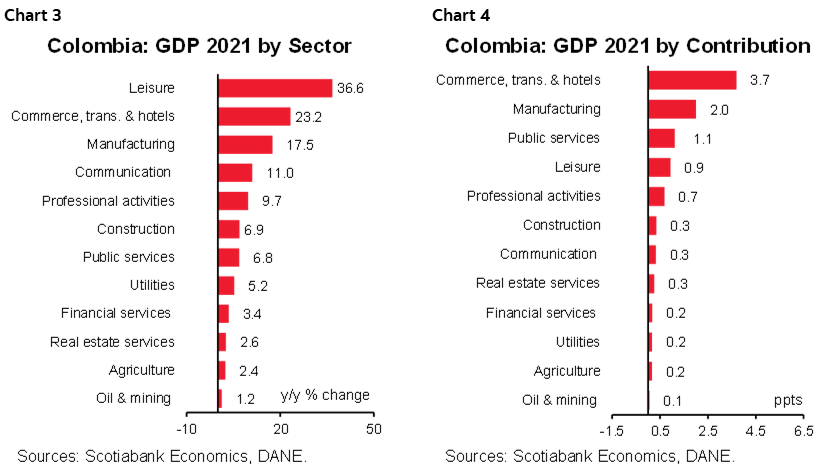

- The most significant increases in the last quarter of the year were in manufacturing (+11.7% y/y), commerce, transport & hotels (+21.2% y/y), and public administration, health, and education (+6.5% y/y), which accounted for 67% of total growth.

- All sectors expanded over 2021 as a whole (chart 3), with the largest expansions coming from commerce, transport & hotels (+21.2% y/y, chart 4), and manufacturing (+16.4% y/y). The weakest performance came from mining (+0.4% y/y).

- At end-2021, only construction and mining remained below pre-pandemic production levels. However, construction grew strongly at the end of 2021, which supports our call that construction will lead GDP growth in 2022.

- At the same time, we see room for further improvements in the services-related sector, as large gathering events and in-person activities resume.

Expenditure side GDP Q3-2021:

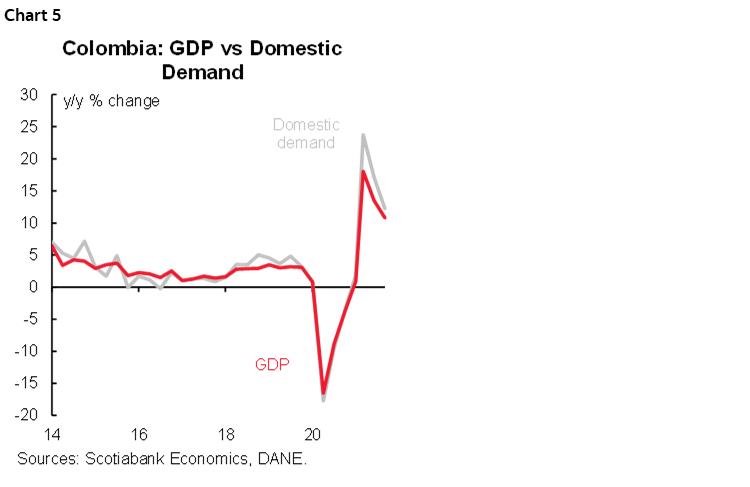

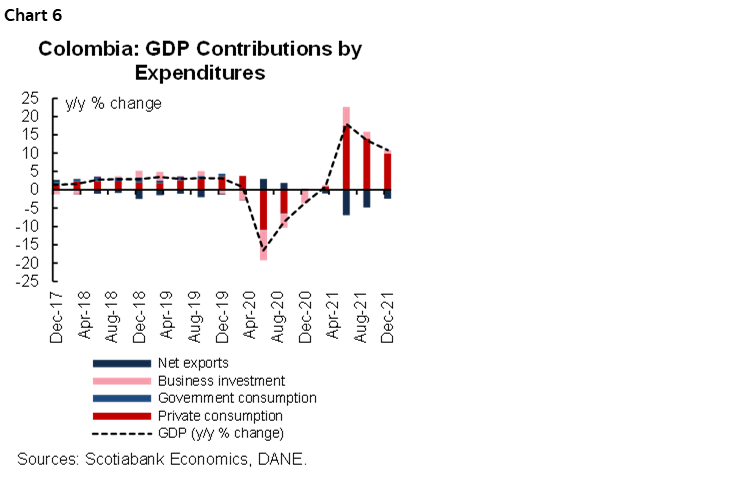

- Domestic demand increased by 12.2% y/y in Q4-2021 (chart 5), well above GDP growth (+10.8% y/y), pointing to a widening of the real external deficit. On a sequential basis, domestic demand expanded by 1.6% q/q sa, moderating from the previous quarter, while import growth slowed. For the whole of 2021, domestic demand expanded by 13.8%.

- Private consumption (+13.7% y/y) contributed the most to the overall growth (+9.9 bps) in Q4 2021 (chart 6). In quarterly seasonally adjusted terms, private consumption posted the strongest increase, which is partially explained by VAT holidays in the October–December period. Public consumption increased by +11.9% y/y and +0.7% q/q, as the COVID-19 crisis eased. Private consumption growth should moderate to more sustainable rates in 2022, while public spending is likely to return to pre-crisis levels.

- Investment expanded by 6.3% y/y and +0.7% q/q sa, showing a positive performance in construction-relating activities, and recovering the ground lost during the nationwide strike in the Q2-2021. Either way, investment closed the year 11.9% below pre-pandemic levels and it will be important to see a better performance in 2022.

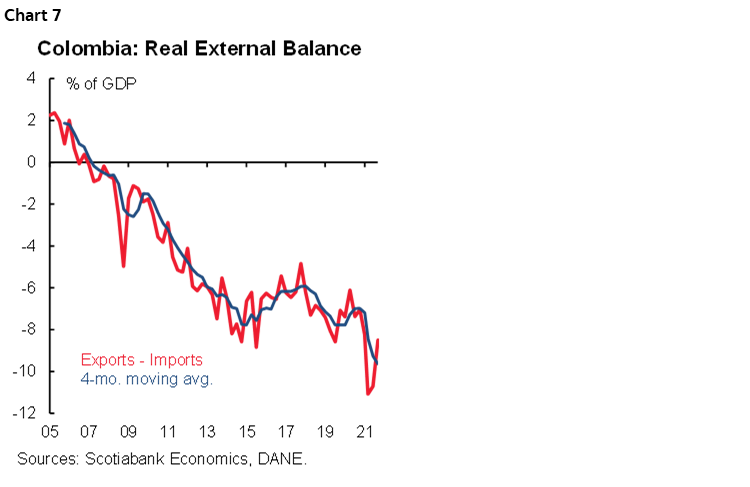

- Net exports contributed negatively to growth in Q4-2021 and 2021 as a whole (chart 7). In Q4-2021, imports grew strongly (+31.7% y/y), but moderated on a quarterly basis (1.9% q/q in Q4 as compared to +7.5% q/q in Q3). Exports registered a 30.5% y/y expansion (11.1% q/q), reflecting a pick-up in the mining sector as the year closed.

- The real external deficit widened in the year which on average represented 9.6% of GDP. We expect the balance to improve somewhat in 2022 amid a better export performance, while imports continue high, fueled by strong economic growth.

All in all, Colombia’s 2021 GDP posted better-than-expected results, with a robust performance in Q4. Services led the gains, supported by manufacturing and the recovery in other sectors, such as construction. On the expenditure side, the main gains came from private consumption, while investment remains below pre-pandemic levels.

A simple calculation shows that, if activity remains at a level similar to that observed in the Q4-2021, economic growth in 2022 would be at least 4.7%. This puts a strong upside skew to our current forecast of 4.5% and approaches the MoF projection (+5.0%). Moreover, continued recovery will generate fiscal dividends in terms of tax collection.

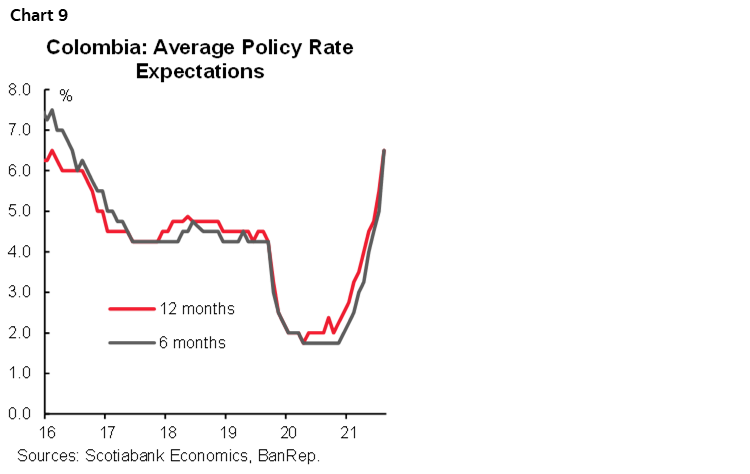

Regarding monetary policy, the central bank is likely to continue its hiking cycle, and we now expect a +125 bps hike at the March meeting, to 5.25%. Weak investment is the main risk to the outlook in 2022, while inflation could negatively impact consumption. At the same time, employment is a key factor to sustained growth and warrants close monitoring.

II. BanRep expectations survey: Inflation expectations increased again and market expect a new 100 bps hike in March

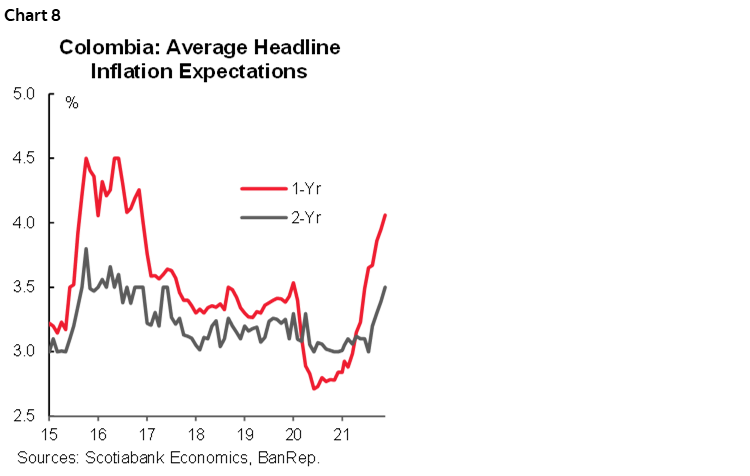

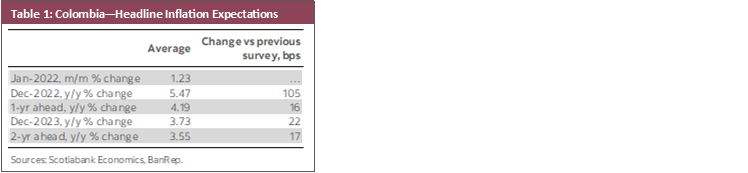

On Tuesday, February 15, the central bank, BanRep, published its monthly expectations survey for January that showed an increase of 105 bps in expected inflation at the end of 2022, to 5.47%. Expectations one year and two years ahead also increased (chart 8), pointing to further indexation effects on inflation down the road—an uncomfortable scenario for BanRep.

The central bank’s tightening cycle is expected to continue, with consensus calling for a 100 bps hike at its March 31 meeting and a further 100 bps rate increase in the April meeting, to get to 6%. While markets expect the terminal rate to hit 6.50% in June (chart 9), the rate subsequently falls to 5.40% by December 2023. Scotiabank Economics expect a 125 bps hike in March and a terminal rate of 5.75%, with upside risk to 6.25%.

- Short-term inflation expectations for February is 1.23% m/m, which would put annual inflation at 7.53% y/y (up from 6.94% y/y in January). The dispersion of the survey remains high, however, with a minimum expectation of 0.42% m/m and a maximum increase of +1.80% m/m. By way of comparison, Scotiabank Economics estimates that actual monthly inflation for December at +1.27% m/m and 7.62% y/y, owing to food inflation, education fees, and other lagged effects from indexation.

- Medium-term inflation expectations for December 2022 increased to 5.47% y/y, 105 basis points above last month’s survey (table 1). Higher actual inflation is now generating long-lasting effects and for the second year in a row the headline inflation is expected to close above the target range (defined between 2% and 4%). Inflation expectations for one-year ahead stood at 4.19% y/y (4.03% y/y in the previous survey), while the two-year forward expectation of 3.55% y/y was also above the target range, showing a new deviation from the 3% target. Scotiabank Economics expects CPI inflation to close 2022 around 5.3% y/y.

- Policy rate. On average, the consensus expects a 100 bps rate hike in March, to leave the rate at 5.0% (from 4.0% currently); Scotiabank Economics expects a 125 bps hike in a split vote. Consensus also expects a policy rate of 6.50% by the end of 2022, an increase compared to the previous survey (5.50%). Scotiabank Economics’ forecast is for a terminal rate of 5.75% with an upside bias to 6.25%, assuming that headline inflation starts to ease in Q2-2022.

- Foreign exchange. The COP is expected to end 2022 at USDCOP 3,833. By December 2023, respondents think the peso will be USDCOP 3,742, and 3,688 at end-2024. We believe that the currency will appreciate by the end of the year to USDCOP 3,755.

—Sergio Olarte & Jackeline Piraján

PERU: GDP GREW 13.3% IN 2021, AS EXPECTED

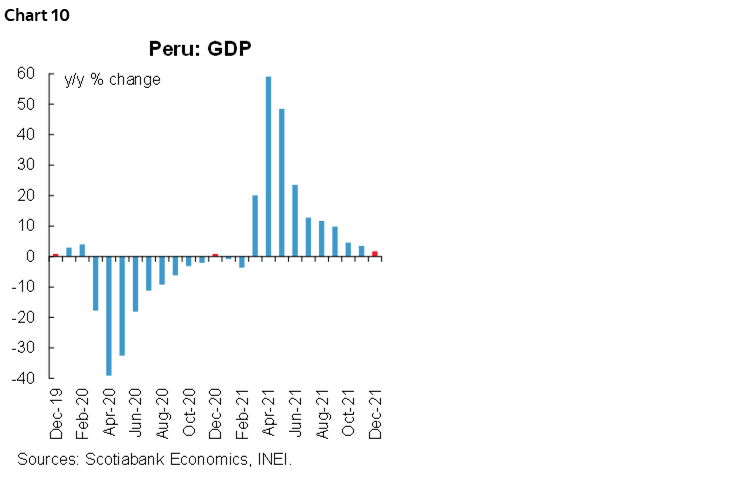

Peru’s GDP grew 1.7% in December, slightly below our 2% estimate. With this result, growth reached 13.3% in 2021, in line with our forecast, recovering from the 11.0% drop in 2020 due to the impact of COVID-19 (chart 10). GDP grew 3.2% in Q4-2021, its lowest quarterly expansion rate since GDP began to grow in December 2020, an evolution explained both by a higher base of comparison and by lower public and private investment. Lower investment was more than offset, however, by the commerce and services sectors, given the dynamism of private consumption and manufacturing, which was driven by strong demand from export-oriented industries.

For Q1-2022 our projected GDP growth is 2.5%, a slightly lower rate than that posted during Q4-2021. Economic activity likely started January at a pace similar to December 2021, but was affected by a drop in fishery production owing to lower anchovy catches. However, we foresee a pick-up in growth in February because the capacity of commercial stores has been maintained and the curfew eliminated in the current third COVID-19 wave, unlike February 2021, when the second wave led to the tightening of social distancing measures. These measures have been relaxed thanks to the progress of the vaccination process that reached more than 80% of the target population. That progress has benefited sectors such as commerce and services, especially restaurants.

—Pablo Nano

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.