- Colombia: President-elect Petro’s inauguration focuses markets’ attention on the proposed tax reform; price pressures continue to increase

COLOMBIA: PRESIDENT-ELECT PETRO’S INAUGURATION FOCUSES MARKETS’ ATTENTION ON THE PROPOSED TAX REFORM; PRICE PRESSURES CONTINUE TO INCREASE

I. Preview of the President-elect Petro’s inauguration

Roughly one month after the run-off presidential election, President-elect Petro will take office on Sunday, August 7th. His administration represents a marked change in traditional politics, since it is the first led by a president broadly considered to be a leftist. Every announcement has therefore been in the market’s spotlight. So far, the new Congress, the composition of the Cabinet, and possible reforms have been the main milestones for markets.

July 20 was the day that the new Congress took office, an event in which each party declared its position with respect to the new administration, with only one party (Centro Democrático) declaring itself as an opposition party. However, by law, the parties have until September 7 to define their positions and have the option of changing their position only once during the four-year mandate. The incoming Petro Administration has adopted a conciliatory attitude and is open to dialogue with all parties.

The Cabinet is still incomplete, with only eight out of the 18 portfolios appointed. As a result, considerable uncertainty remains with respect to the composition of the government. Additionally, the directors’ names of several public institutions have not been named, including the Dane statistical agency.

However, a key appointment, the Ministry of Finance, has already been made with the appointment of Jose Antonio Ocampo, a renowned economist, whose nomination helped to calm markets. Ocampo is talking sensibly about tax reform, noting that it will be structural in nature, and that reforms would be gradual and consistent with the rule of law. Expected revenues have moderated, as Ocampo indicated he wants to collect more than COP 45 trillion, while the text that will be filed with Congress on August 8 would target revenues of around COP 25 trillion.

Key points of the tax reform include:

- Income tax will be increased for persons with incomes above COP 10 million, about 1% of the population, according to calculations of the Minister.

- The base of the wealth tax will be reduced to COP 2000 million.

- For companies, some tax exemptions and benefits will be removed.

- The minister does not rule out the possibility that another reform will be proposed to reduce the percentage of tax by companies.

In addition to tax reform, there are also proposals with respect to rural land reform, education, the health system, and the pension system. However, they are not a priority in the short term. Meanwhile, the president-designate of the economic commission of Congress has said that he hopes in this first legislature to address three important projects for the beginning Petro Administration: tax reform, Budget for 2023, and national development plan.

Overall, there has been a tone of moderation in the speeches of the president-elect, who has been open to dialogue with all social sectors and especially with Congress. For now, we think that the Sunday, August 7th inauguration will not generate an overreaction or higher risk premia in markets. In the near term, the focus will be on the tax reform bill and pending appointments.

II. Headline inflation highest since start of inflation targeting

Monthly CPI inflation was 0.81% m/m in July 2022, according to DANE data published on Friday, August 5. The result was well above BanRep’s survey (0.53% m/m) and Scotiabank Economics’ projection (0.63% m/m). July’s inflation was more than five times the average monthly inflation observed since 2016 (0.15% m/m).

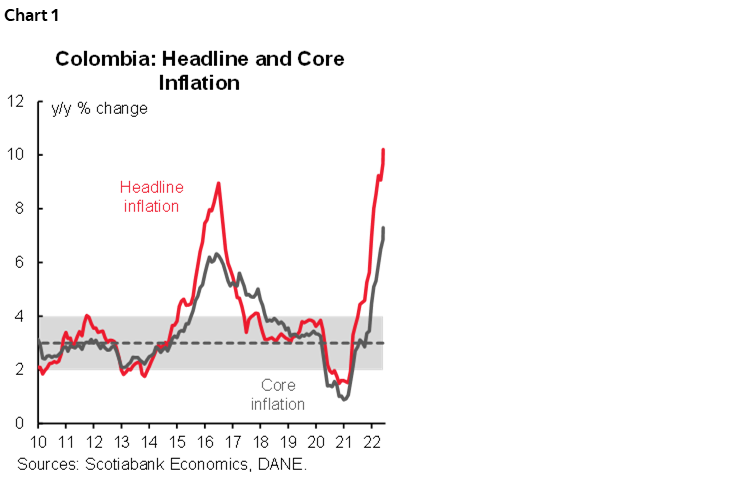

Annual headline inflation stood at 10.21% y/y, up from 9.67% y/y in May (chart 1), and the highest since the inflation targeting regime was implemented. In monthly terms, food inflation again accelerated, increasing 1.1% m/m from the previous 0.65% m/m. Utility and rental fees were the second main contributors, with the reversal of the VAT holiday and higher gasoline prices also contributing.

Core inflation rose again, from 6.84% y/y to 7.29% y/y, the highest level since December 2003, while ex-food and regulated goods inflation came in at 6.44% y/y (up from 6.06% of the previous month), the highest level since 2009. Food inflation was the main contributor, while core metrics show other sources of pressure, such as rental fees, some services, and tradable goods, especially vehicles, which is now the fifth main contributor to the inflation.

July’s CPI print would, in our opinion, put again pressure on the central bank ahead of September’s meeting. Our projection is of a 9.50% terminal rate, but there is a strong upside bias. We expect inflation to continue oscillating around 10% in coming months; however, high inflation at year-end will again trigger strong indexation effects ahead of 2023 amid the minimum wage negotiation. As BanRep mentioned, uncertainty remains, though high inflation could make it go farther than expected in the hiking cycle.

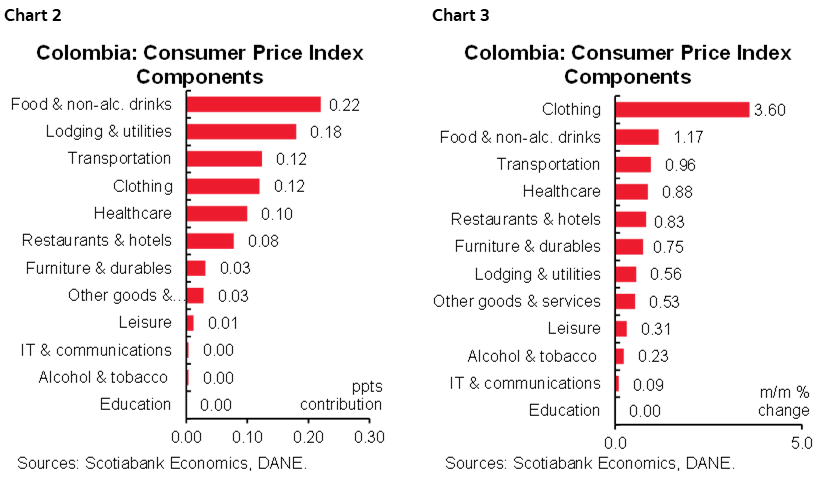

Looking at July’s numbers in detail, 11 out of the 12 components of the CPI index contributed to higher inflation (charts 2 and 3).

The main highlights are:

- Foodstuffs inflation again accelerated, with a 1.17% m/m increase, with a contribution of 22 bps to total inflation. In July, meat (+1.17% m/m), chicken (+2.04% m/m), vegetables (+5.01% m/m) and corn-related products (+4.14% m/m), were the main contributors, reflecting, in part, international price dynamics. According to DANE, price pressures are unlikely to moderate in the term as fertilizer and import prices for food production continue to show upside pressures. Food prices are thus the main upside risk in our projection for H2-2022, and could lead to inflation closing the year at double-digit levels if pressures similar to those observed in July continue.

- The second main contribution (+18 bps) came from the lodging and utility group (+ 0.56% m/m). In this group, utility fees (+1.62% m/m) are driven by indexation effects, while electricity (+1.13% m/m) and gas (+2.91% m/m) reflect FX depreciation. In the same vein, rental fees (+0.22 % m/m) are also contributing to inflation, but according to DANE the indexation in rents is normalizing.

- FX depreciation and bottlenecks in international logistical channels are also contributing to higher inflation. Vehicle prices (+1.77% m/m) became the fifth biggest contributor to inflation, and in the last year have increased by 15.2%. Health care and cleaning products are reflecting higher production costs amid international input price increases.

- Other contributors to the July number include the reversal of the VAT holiday, especially with respect to clothing prices (+3.6% m/m). However, clothing prices are also rising because of higher input costs and FX depreciation.

- Gasoline prices (+1.97 % m/m) contributed 6 bps to total inflation and will be an important effect if the government continues increasing prices to avoid higher deficits in the gasoline price stabilization fund.

Looking at annual inflation across major categories, goods inflation increased from 8.30% y/y to 9.52% y/y owing to the VAT holiday reversal and higher international prices, while services rose slightly, from 5.21% y/y to 5.26% y/y, a more moderate increase that could point to weaker economic activity and private demand. Regulated-price inflation increased 69 bps to 10.49% y/y.

All in all, July inflation again surprised on the upside, largely as a result of higher-than-expected food inflation, but also higher tradable goods prices. Services inflation is posting lower increases, which could be associated with a moderation of the economic activity. Regardless, July’s result puts pressure on the central bank as headline inflation reached the highest level since the start of the inflation targeting regime, with no signs of a reduction. In this respect, while our forecast calls for a 50 bps hike in September to bring the policy rate to 9.50%, there is an upside bias on the terminal rate which would be realized if inflation continues to rise.

—Sergio Olarte, Maria (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.