- Mexico: Minutes suggest a 75 bps hike in September while June GDP proxy suggests growth is cooling from a solid pace earlier this year

MEXICO: MINUTES SUGGEST A 75 BPS HIKE IN SEPTEMBER WHILE JUNE GDP PROXY SUGGESTS GROWTH IS COOLING FROM A SOLID PACE EARLIER THIS YEAR

I. Banxico Minutes Suggest a 75 bps Hike in September

Banxico released the minutes of its August decision, where in a unanimous decision, the bank decided to increase the monetary policy rate for the second time by 75 basis points to 8.50%. In our view, the communiqué of the decision hinted that the Board might not opt for 75 bps again in September and now, after the discussion embodied in the minutes, we expect a divided Board in the next decision: on the one hand, further tightening seems unnecessary as some of the pressures outside the scope of central banks' action start to ease. On the other hand, we cannot ignore certain signals that indicate a process of de-anchoring inflation expectations (nominal wage increases at historical highs, deterioration of long-term inflation expectations). Therefore, in this uncertain environment and with a balance of risks, both local and external, markedly biased to the upside, we expect Banxico to opt for another 75-bps hike in September.

In the global environment, most agreed that global economic activity has continued to weaken: slowdown in China, the geopolitical conflict, prolonged inflationary pressures and tightening global financial and monetary conditions have increased fears of a recession in the near future. Some highlighted the case of the United States, where GDP fell for two consecutive quarters with labour market conditions remain strong. Even so, considerable risks to global growth remain.

Regarding economic activity in Mexico, most agreed that the recovery continues, supported by industrial production and services, although it remains incomplete and uneven. In this regard, several mentioned that certain indicators suggest that consumption has begun to decelerate, despite wage increases and remittances. Towards the second half of the year, the slowdown in the U.S. economy, the drought affecting several regions of the country and the lag in investment are factors that contribute to a downward bias in the balance of risks to growth.

On inflation, the majority highlighted that it is the result of external global factors that directly affect production and input costs, although another member mentioned insecurity in the country as another factor contributing to the increase in prices. However, what stands out most in the document is the discussion around the continuous increase in inflation expectations and the actions needed to avoid further deterioration in price formation. One board member sees the need to “continue the pace of tightening the monetary stance”, while another believes that “there are indications that we are close to reaching an unnecessarily high level of monetary tightening”. While the tone of the minutes continues to be restrictive, it is also evident that at least one Board member is concerned about tightening more than necessary, so while we expect Banxico to continue to act with the same “forcefulness” that we have seen in the last two decisions, we cannot rule out the possibility that it will reduce the pace of tightening.

—Luisa Valle

II. GDP in Q2-2022 increased owing to dynamism in both services and industry, but monthly proxy in June suggests downside risks

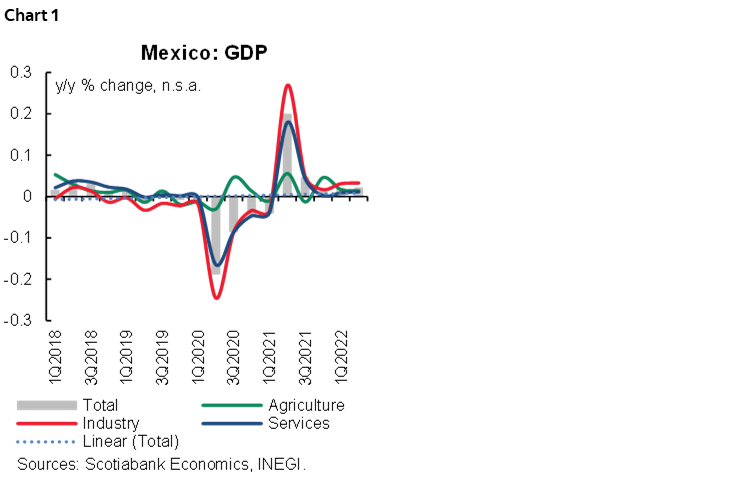

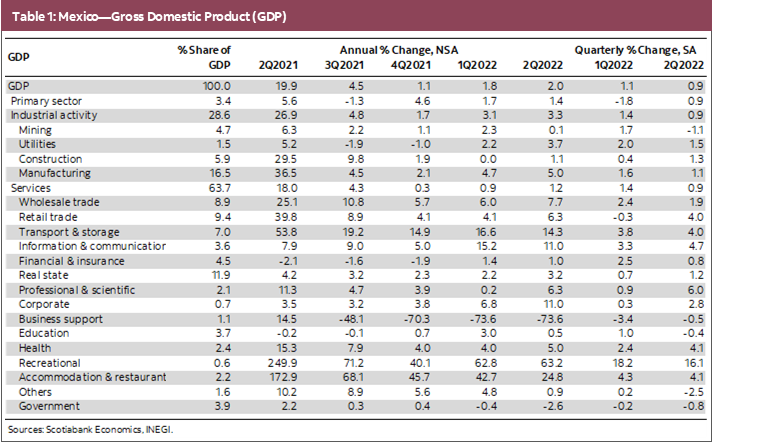

INEGI released the revised GDP figures for Q2-2022, which came in at 2.0% y/y in real terms, marginally below the flash estimate of 2.1% and in line with consensus (chart 1). By sector, industry accelerated to 3.3% y/y (versus 3.0% previously), driven by the increase in manufactures, which accelerated 5.0% (from 4.7% previously). The services sector registered an increase of 1.2% y/y (from 1.9% previously), with important advances in most of its components, although lagged by a significant drop in corporate services owing to the effect of the outsourcing bill implement in April 2021. Services related to hospitality, and leisure activities continued to surge on a yearly basis as COVID-19-related risk almost dissipate (63% y/y and 24% y/y, respectively). The primary sector decelerated to 1.4% y/y, from 1.9% previously. With this, GDP grew 1.9% YTD during the first half of 2022 (table 1). In its seasonally adjusted quarterly comparison, GDP moderated to 0.92% q/q, from 1.14% previously. By sector, industry moderated by 0.86% q/q (1.39% previously), services sector also cooled 0.92% q/q (1.39% previously) and the primary sector rebounded 0.94% (-1.81% previously).

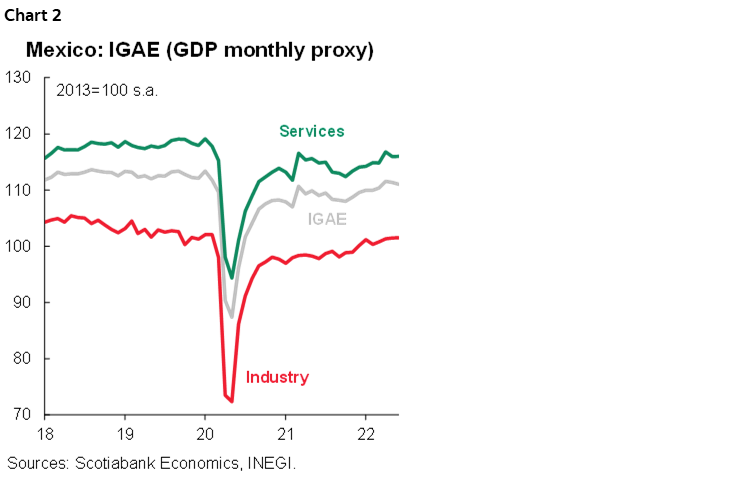

In June alone, the GDP proxy (IGAE), also released by INEGI, dropped for the second consecutive time on a seasonally adjusted monthly basis (chart 2), this time from -0.2% to -0.3% m/m. Industry moderated from 0.2% to 0.1% m/m, while services showed no change (0.0% m/m from -0.7% previously), and primary activities fell -6.6% m/m from 2.0% previously. In its annual comparison nsa, the IGAE index moderated from 2.1% to 1.6% y/y.

Looking ahead, we expect modest advances during the remainder of the year, as we anticipate a 1.7% GDP growth during 2022, and 1.5% for 2023, in line with the expected slowdown in the US economy, and the effect of interest rate hikes.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.