- Colombia: Headline inflation 8.53% y/y in March, highest level since mid-2016

- Peru: The government declares a curfew, unleashing protests and disturbances

COLOMBIA: HEADLINE INFLATION 8.53% Y/Y IN MARCH, HIGHEST LEVEL SINCE MID-2016

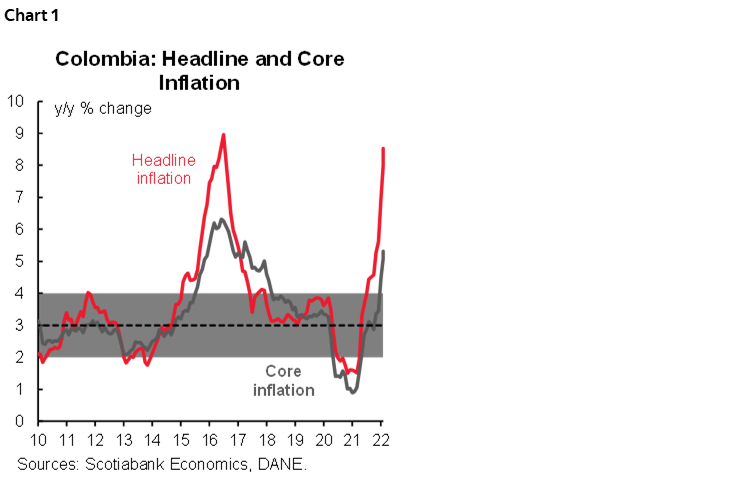

According to DANE data published on Tuesday, April 5, monthly CPI inflation was 1.00% m/m in March 2022, close to the median forecast in BanRep’s survey (0.91% m/m), and above Scotiabank Economics’ projection (0.80% m/m). March m/m inflation was almost double the average rate of inflation since 2016 (0.53% m/m) and brings annual headline inflation to 8.53% y/y, up from 8.01% y/y in February (chart 1). This is the highest rate of inflation since mid-2016 and the eighteenth consecutive month that inflation has been above BanRep’s target range (2%–4%). Annual food inflation is at its highest level in recent history at 25%.

Core inflation also increased, from 5.10% y/y to 5.31% y/y, while ex-food and regulated goods inflation came in at 4.51% y/y (up from 4.11% the previous month). These results show that inflation is not only reflecting the effect of supply shocks on food prices, but also upside pressures on other key prices probably due to indexation effects and the ongoing recovery.

We now expect a 100 bps rate hike in April’s monetary policy meeting. Ahead of April and May, we expect the headline inflation to show some moderation due to the statistical base effect associated with the nationwide strike one year ago. However, we would need to see further normalization in foodstuff inflation on a m/m basis to confirm a downward trend in H2-2022. That said, we expect the hiking cycle to end at 7.50% in July, with the rate easing to 5% by the end of 2023.

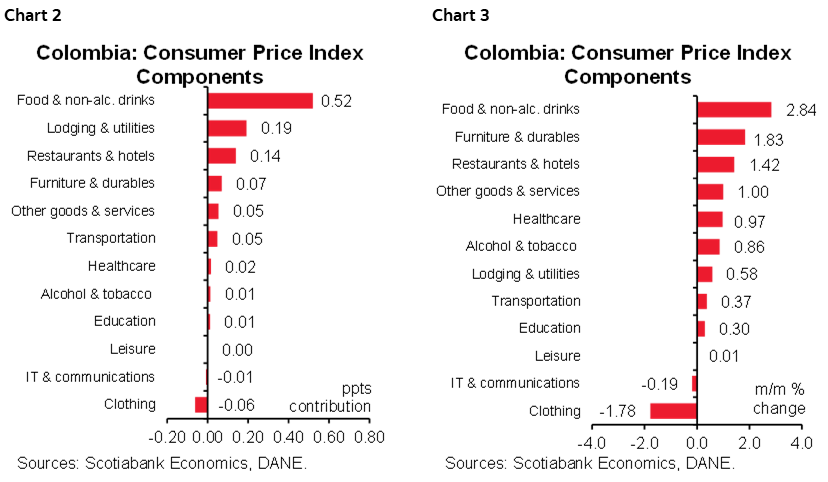

Looking at March’s numbers in detail, 10 out of the 12 components contributed to higher inflation (charts 2 and 3), with foodstuffs once again posting the highest gains. The main highlights are:

- Foodstuffs had the largest contribution (+52 bps), with inflation of +2.84% m/m, coming from rice (+6 bps), fruits (+6 bps), milk (+4 bps) and eggs (+4 bps). Rising input prices and seasonal issues in the harvest process are exacerbating food price increases, which are now at the highest level in recent history reaching 25% y/y. The war between Russia and Ukraine has led to higher fertilizer prices in the PPI index, which will continue to be reflected in the CPI numbers in coming months.

- In April and May, food price inflation will encounter a high statistical base due to the nationwide strike in 2021. Monthly food inflation in those months a year ago were 2.09% m/m and 5.37% m/m, respectively, which could contribute to lower headline inflation in April and May. However, if food inflation remains above an average of 0.80% m/m for the rest of the year, total inflation would continue accelerating after June.

- Lodging and utilities (+19 bps) were the second largest contributors to headline inflation. In February, rents rose 0.35% m/m, reflecting indexation effects. Utility fees jumped by 1.37% m/m, led by electricity (+1.44% m/m), water (+2.12% m/m), and garbage collection (+1.46% m/m).

- Other components recorded monthly inflation at above pre-pandemic averages. Cleaning-related goods also contributed to price pressures owing to higher input prices.

- Clothing had a negative contribution due to the VAT holiday. However, the price reversal was lower than it was observed in previous years as the new stock is showing higher prices.

Looking at annual inflation across major categories, goods inflation jumped to 6.42% y/y in March, while services increased from 3.40% y/y to 3.79% y/y. Regulated-price inflation moderated from 8.32% y/y and 8.91% y/y.

All in all, inflation continued to rise in March in y/y terms, but without an upside surprise. About half of total inflation was again explained by food inflation. However, the remaining groups likewise show indexation effects in the middle of still-robust demand. The VAT holiday produced a moderate downward effect. April and May will likely some relief in headline inflation, though June will be critical to confirm a downward trend. For now, we expect the central bank to continue hiking the monetary policy rate until it reaches 7.50%. We anticipate rates will start to ease in early in 2023 as inflation returns to the target range.

—Sergio Olarte & Jackeline Piraján

PERU: THE GOVERNMENT DECLARES A CURFEW, UNLEASHING PROTESTS AND DISTURBANCES

The government’s decision to declare a State of Emergency in Lima, including a 24-hour curfew (the full day of April 5), backfired as it stirred even greater protests and disturbances. The curfew was announced at midnight Monday night, so most people were not aware until early next (Tuesday) morning, generating confusion in the early morning. The surprise measure met with opposition across the political spectrum, with even members of Congress on the centre-left, who normally support the regime, coming out against the decision.

The reason given by the government for the emergency measure was that it had received, presumably through police intelligence, reports that segments of the population were organizing mob raids on stores on April 5. This may be possible, as acts of vandalism had been recurring over the past few days in different parts of the country, in the shadow of the confusion caused by a nationwide transportation strike.

Opposition to the stay-at-home curfew was evident in social media very early in the morning, with calls for disobedience. At least one mayor, that of the Lima district of San Isidro, publicly announced that his office would not obey the measure. The country’s ombudsman (Defensoría del Pueblo) submitted a legal brief against the measure to the courts.

The government itself showed a lack of conviction in enforcing the curfew, as road checkpoints that were in place at the break of day, were largely removed by mid-morning. At mid-day, residential areas reverberated with the calming sound of pots being banged to signal disapproval with the measure. At 3pm, President Castillo and the entire Cabinet visited Congress seeking, purportedly, to work out a solution to the crisis. Two opposition parties, Fuerza Popular (Fujimori) and Avanza País, refused to participate in the meeting. By this time, protesters were already pouring into downtown Lima. At little after 5pm, President Castillo finally lifted the curfew and the State of Emergency, nearly seven hours early. By then, very few people were actually obeying the curfew. The protests themselves lasted well into the night. A number of police officers were injured. There were no official report of injuries among protesters, but media showed some people that were injured.

So, what does it all mean? It is possible that there was a valid reason for the government to fear mob raids and vandalism, given that similar acts had already occurred, albeit on a limited scale. At the same time, the government decision could also have been an attempt to buy time and calm the waters surrounding the transportation strike. The counterargument is that even if these risks existed, such a severe measure as a full-force curfew was an overreaction, and proof of the government’s lack of managerial skills towards a more measured and focused solution. It is also clear that the government did not expect the reaction that has occurred. The protests were against the curfew only in name, and appeared to reflect a much deeper sensation of dissatisfaction with the government, as chants quickly evolved into calls for Castillo to resign.

It was not really surprising that nothing came out of the meeting between the Executive and Congress. Neither side introduced a proper working agenda. At times it seemed that President Castillo’s desire to meet with Congress was more a call for help, although it could also simply have been a gesture of good faith. It is not the first time that President Castillo has appeared to be trying to extend a hand to Congress. It is not working, perhaps largely because of his government’s evident association with the more radical Perú Libre.

Some members of Congress are talking about calling for a vote of no confidence against the Torres Cabinet. The Castillo Government is increasingly besieged by protests and social conflicts, and it has not found the formula, or the appropriate team, to manage them. The protests may blow over, but they add to the impact of the transportation strike on general business costs and logistics, to the effect of social conflicts on mining operations, and so forth, to amplify concerns. We have not changed our forecast of 2.6% GDP growth for 2022, as so far protests and conflicts have not been prolonged enough. But, they are adding up.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.