- Chile: GDP expanded 6.8% y/y in February; non-mining activity drops 0.8% m/m, signaling a soft-landing

- Peru: Inflation surprises in March, the highest in 28 years

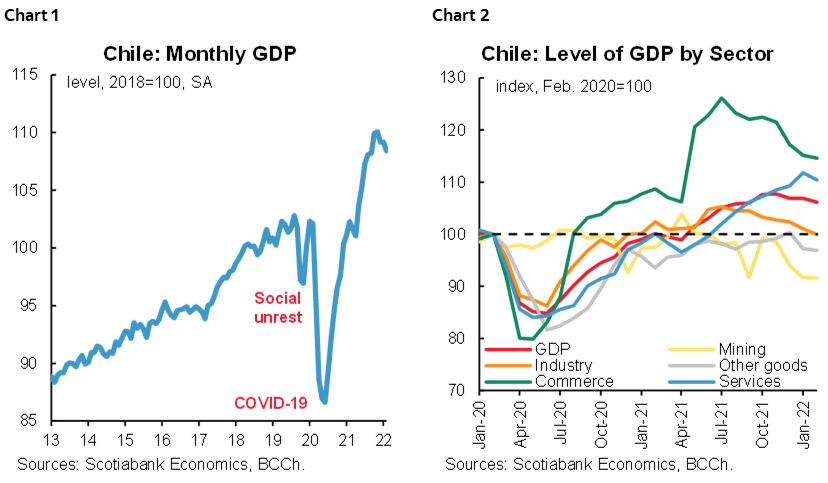

CHILE: GDP EXPANDED 6.8% Y/Y IN FEBRUARY; NON-MINING ACTIVITY DROPS 0.8% M/M, SIGNALING A SOFT-LANDING

Weaker activity means benchmark rate unlikely to go above 7.5%. Possible technical recession on eve of constitutional referendum.

On Friday, April 1, the central bank (BCCh) released its proxy for monthly GDP growth (IMACEC) for February, which increased 6.8% y/y well below market consensus and Scotiabank’s expectations (8%). The main surprise for our short-term scenario comes from services, which fell 1.2% m/m after expanding 2.3% m/m in January (charts 1 and 2). This sector should improve in March, as mobility restrictions introduced in response to increased COVID-19 cases were in place in February. The relaxation of these restrictions should partially offset a negative trend in activity. Meanwhile, seasonally adjusted monthly data suggest a slight slowdown is in process in the rest of the sectors.

A technical recession in Q2-2022 is probable, confirming BCCh’s caution. In our view, the central bank is unlikely to raise the benchmark rate above 7.5% in this tightening cycle and we reiterate our call for an increase of 25 basis points at the next monetary policy meeting, provided the CPI for March does not exceed 1.1% m/m. A moderate technical recession is part of our baseline scenario and the just released February data could lead to a seasonally adjusted contraction in Q1-2022. This contraction is likely to be followed by another (seasonally adjusted) marginal decline in Q2-2022, marking a technical recession after the June IMACEC is released on August 1.

With the plebiscite to ratify the constitution pending, the economy could thus be in a technical recession that might affect the decision of undecided voters. The Constituent Convention is scheduled to deliver the proposal for a new Constitution to President Boric on July 5, while a technical recession could be called less than one month later. (This would be the first technical recession since March 2017 in the last part of the government of President Michelle Bachelet, as Chile did not have a technical recession during the social unrest or the worst of the pandemic.)

The non-mining IMACEC dropped a moderate 0.8% m/m (after +0.8% m/m in January), mainly influenced by the decline in services (-1.2% m/m). We believe that the contraction in services is largely explained by a break in services associated with investment. Other sectors declined modestly on a m/m basis, particularly commerce and construction.

Public spending did not contribute to investment growth, which likewise affected investment-related services. Public spending in February grew 3.6% y/y owing to higher health spending (vaccines). However, capital spending (public investment) contracted by a significant 3.9% y/y, which could have influenced the fall in services more linked to investment. Looking ahead, the fiscal budget incorporates a significant increase in public investment for 2022, so this component should begin to support investment in the coming months.

The new fiscal package of the government will be known in coming days, though USD 3.5 bn focused on small companies and households most affected by the rise in consumer inflation has already been announced. This package would be financed with freely available resources (without further debt issuance), and would have an impact on activity in the second half of the year.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

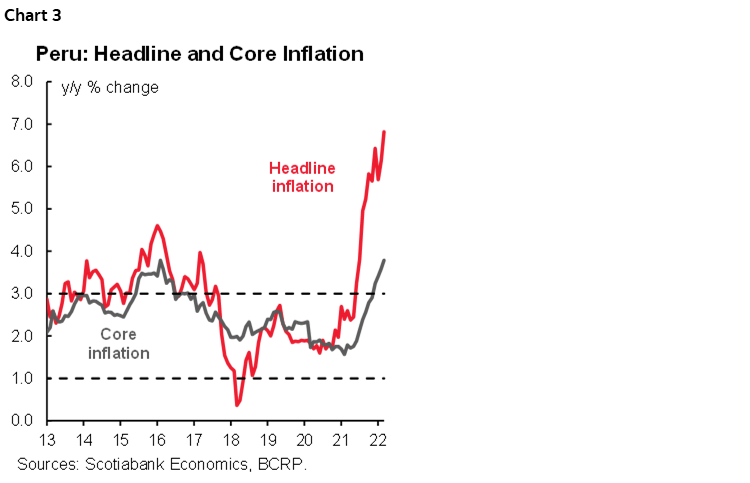

PERU: INFLATION SURPRISES IN MARCH, THE HIGHEST IN 28 YEARS

Inflation surprised to the upside in March, reaching 1.48% m/m, the highest m/m rate in 28 years for the month of March (since March 1994 when it reached 2.32%), exceeding the estimate by the market consensus (0.92% according to a Bloomberg survey) and our own forecast of 1.2%. Year-on-year inflation accelerated from 6.2% y/y to 6.8% y/y (chart 3), in line with what was observed in the rest of the region. March marks the tenth month in a row that inflation exceeded the upper limit of the central bank’s target range (between 1% and 3%) and price pressures show no signs of converging towards the target. The March result will exert pressure on the central bank, which we expect will continue to raise its reference rate in April.

Price pressures were broadly based in March. Of the 586 products that make up the new consumer basket (base 2021), 457 (78%) rose, 69 (12%) fell, and 60 (10%) remained unchanged (table 1). Core inflation went from 3.6% y/y in February to 3.8% y/y in March, above the upper limit of the target range (3%) for the fourth consecutive month. Wholesale inflation, linked to production costs, went from 11.4% in February to 11.6% in March. Cost pressures, such as port freight, energy and agricultural commodity prices, were exacerbated in March owing to the Russia-Ukraine conflict, which will drive inflation higher in the future. The USDPEN exchange rate, which depreciated 3.6% in February on a year-on-year basis, appreciated 1.8% in March, limiting the rise in the prices of imported products.

For April, we expect inflation above to 7% y/y, driven by a low base of comparison since inflation in April 2021 was negative (-0.10% m/m) and by the pressures of higher commodity prices, such as oil, grains and fertilizers, on local prices.

In our Latam Weekly of March 18, 2022, we revised our inflation forecast from 4.2% to 6.4% for 2022, as a first approximation of the likely impact of the Russia-Ukraine war on the price of oil and cereals. We see inflation at least as high as that posted in 2021. However, we will adjust our forecast as we have greater clarity on the duration of the effects of the conflict on commodity prices and supply chains.

Over the past eight months, the central bank raised its benchmark rate by 375 basis points to 4.0% and increased reserve requirements three times. With inflation accelerating, we expect this hawkish stance on inflation control to continue. We believe that further increases in the key policy rate are necessary to bring inflation expectations (3.75% over 12 months according to the BCRP February survey) to the target range, so we expect a 50 bps hike at their meeting on Thursday, April 7.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.