ON DECK FOR FRIDAY, MAY 8th

KEY POINTS:

- Markets on cautious footings into payrolls, developments in Iran

- Trump’s misguided 10% Section 122 tariffs shot down—sort of

- The signs that US-Iran negotiations are not going well

- Nonfarm payrolls & Canadian jobs on tap

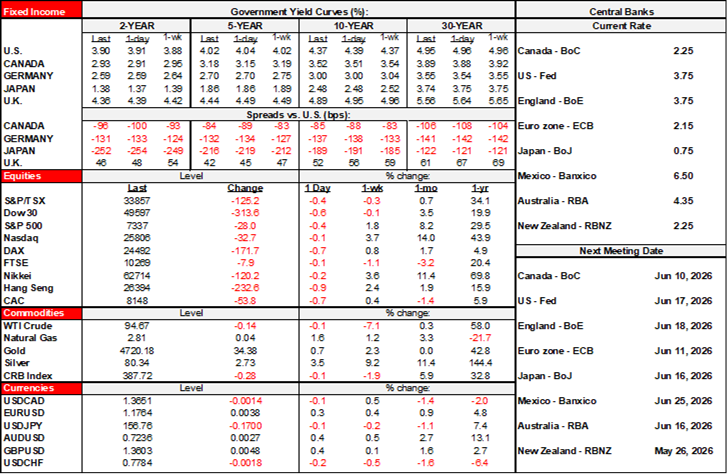

Global markets are highly mixed into the end of the week amid swirling developments on tariffs (see below), conflict in the Middle East, and ahead of dual jobs reports out of the US and Canada. Oil is little changed after reversing yesterday morning’s dip because of signs that US-Iran negotiations are not going well (see below). US and Canadian equity futures are a little higher, but European cash markets are down by up to about -1%. The dollar is generally softer but not by much. Sovereign bond yields are mixed with gilts outperforming. Mexican markets will follow US payrolls and oil market developments after Banxico delivered the universally expected -25bps cut with a narrow 3–2 vote and signalled the end of the easing cycle yesterday afternoon.

All of that could change very shortly and perhaps multiple times over today’s market session.

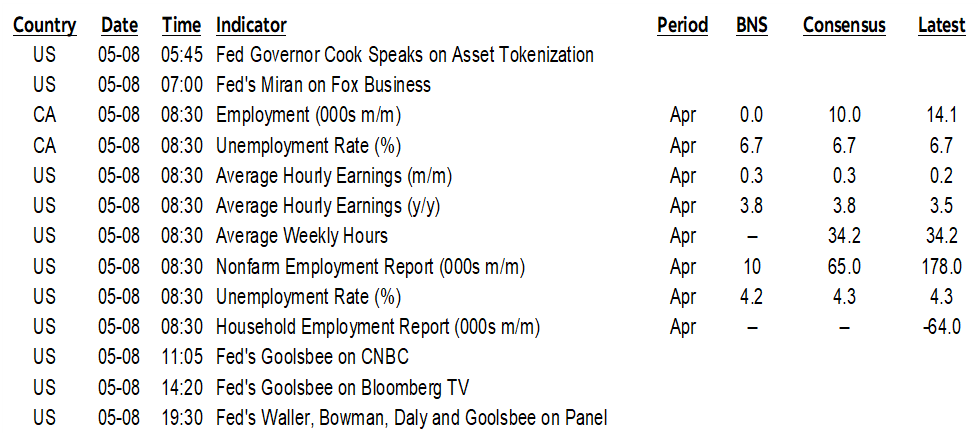

NONFARM PAYROLLS

April’s batch of US job market readings arrives at 8:30amET. Consensus expects 65k for the change in nonfarm payrolls and an unchanged unemployment rate and I’m at 10k with a downtick to 4.2% for the UR. A full preview was available in my weekly which I won’t repeat here at this late stage. Onto the numbers.

CANADIAN JOBS

April’s batch of Canadian job market readings also arrives at 8:30amET. Unlike the US that releases both the payroll and household surveys simultaneously, Canada will only release the household survey today. The Canadian payrolls measure lags by a couple of months and is poor quality with off-the-charts monthly revisions whereas the Labour Force Survey is only revised once per year.

Consensus is at 10k for the change in jobs and I’m at 0k with an unchanged UR at 6.7%. See my weekly for a full preview. Onto the interpretations and clean-up.

SECTION 122 TARIFFS SHOT DOWN—SORT OF

It has long been clear that the Trump administration abuses past pieces of legislation when it imposes tariffs. It’s clear to many readers of a publication like this one that tariffs are just plain bad economic policy that damage global trade and global growth with American consumers and businesses paying for them. Yesterday’s decision by the US Court of International Trade was the latest validation of those views.

The Court voted 2–1 against Trump’s 10% global tariffs that he introduced under Section 122 of the Trade Act of 1974 back in February. They were imposed as a temporary replacement for IEEPA tariffs that were shot down and until bogus tariffs under Section 301 of the Trade Act can be imposed after fake investigations led by the (anti) Commerce Department. The Court ruled that the administration misinterpreted the act’s definition of a balance of payments problem.

Next steps are highly uncertain. The Court only ruled in favour of the small business complainants. It rejected the standing of the states in the matter and did not issue a universal rejection of the Section 122 tariffs which seemed half-baked. The Justice Department will probably appeal. What we’re left with is more soul-crushing uncertainty hanging over the American and global economies.

SIGNS POINT TO NO US-IRAN DEAL

The US continues to wait for Iran’s response to its 14-point plan to suspend or end the war. Developments in the background suggest that Iran may have made up its mind and is acting in such fashion as to have rejected the plan or is delaying along the lines of the ‘managed irresolution’ narrative.

- Iran's Foreign Minister met with Pakistan's president after Iran's President met with Supreme Leader Khamenei. This suggests Iran may have decided on its course of action and communicated it through Pakistan as Iran said it would.

- Iran's new mechanism for tracking ships and charging them fees for using the Strait is a direct affront to the US demand that the Strait be opened without such restrictions.

- The US is planning to restart 'Project Freedom' ie: forced opening of the Strait and with apparent use of Saudi and Kuwaiti bases.

- Attacks unfolded in both directions yesterday into today across the Strait included military clashes and Iran’s seizure of a tanker.

- News broke yesterday that the reason why Trump suspended “Project Freedom” earlier in the week—the effort to force the reopening of the Hormuz Strait—wasn’t because the administration was offering a deal to Iran but because the Saudis and Kuwaitis refused to grant use of their airspace and bases by the US. The Saudis and Kuwaitis then reversed course yesterday and granted use, allowing the US to proceed with ‘Project Freedom’ shortly. Articles like this one argue that the 14-point US plan that was delivered to Iran coincided as cover for the suspension of ‘Project Freedom’ and as a cynical return volley to Iran’s 14-point plan that was delivered to the US last week.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.