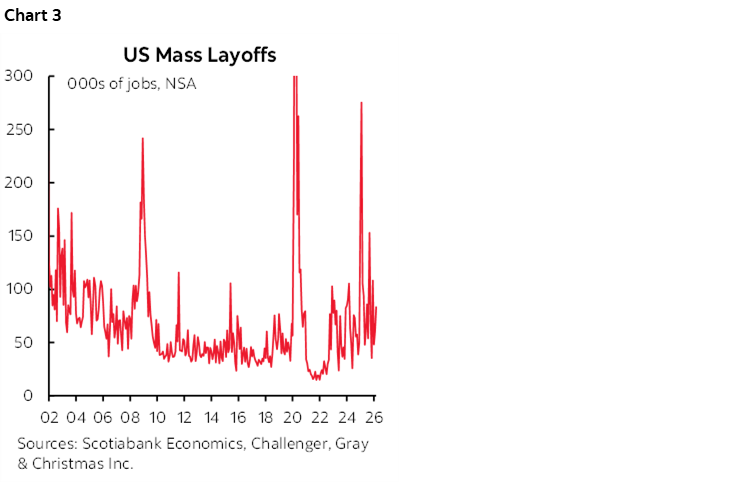

ON DECK FOR THURSDAY, MAY 7th

KEY POINTS:

- Deal or no deal? Markets remain cautiously optimistic

- Norges Bank hiked despite restrictive stance going in

- Riksbank held, absent its neighbour’s energy exposure

- Banxico may cut and signal an end to easing

- German factor orders soared

- US job cuts picked up

- US productivity probably stalled, labour costs up

- Was the drop in US jobless claims a flash in the pan?

Deal or no deal? Where’s Howie Mandel when you need him. After all, I’m surprised he hasn’t been called in to guide things thus far, given that much of Washington has become a reality tv or game show. Markets continue to be cautiously optimistic toward the prospect of a US-Iran deal to end the war despite the appearances of the US administration pumping the deal vastly more than the other side. Oil is off by another couple of bucks this morning. Sovereign yields are slightly lower by 1–2bps across major markets. The dollar is on the run, but with the krone outperforming after Norges hiked. Equities are mixed, however, with N.A. futures in the black but European cash markets slightly in the red.

Any hints at which direction negotiations are going will clearly dominate market movements relative to what else is on the line-up below.

NORGES BANK HIKES

Norges Bank partially surprised by delivering a 25bps hike, raising the deposit rate to 4.25%. The krone is the strongest performer to the dollar. Norway’s curve barely changed. Markets are pricing half of another hike in June.

Only five out of 17 forecasters anticipated the move. The reason for the mixed consensus going in was that “the Committee judges that it will likely be necessary to raise the policy rate at one of the forthcoming monetary policy meetings.” That lack of specific guidance was somewhat unusual for a central bank that publishes explicit guidance. Further, Norges was already in restrictive territory going into the decision, unlike other central bank in significantly commodity-driven economies like the BoC that sits at the bottom end of neutral rate range.

Guidance continues to point to the possibility of a further hike but with highly uncertain timing. Norges merely pointed to its March projections for the policy rate to potentially end the year at between 4¼% and 4½%.

RIKSBANK HOLDS

Sweden’s central bank held its policy rate at 1.75% as widely expected and markets largely shook off the decision. All forecasters got this one right. Forward guidance noted “there is scope to wait until there is a clearer picture of the effects of the war and the supply shocks it entails.” The Riksbank noted that inflation is below target and economic activity is weak. Sweden clearly does not benefit from the commodity shock like neighbouring Norway does.

BANXICO EXPECTED TO CUT

Mexico’s central bank is unanimously expected to cut its overnight rate by 25bps this afternoon with markets a little more uncertain about the combination of the possible move and guidance (2pmET).

Banxico has an easing bias as indicated by saying at its March meeting that “the Board will evaluate the appropriateness and timing for an additional reference rate cut.” Growth is disappointing as the economy contracted in Q1. Still, expect dissenting voices again after Deputy Governor Jonathan Heath voted against easing the last time because of inflation worries. Governor Victoria Rodriguez Ceja recently remarked that the end of the easing cycle is near at hand and so this could be the final cut.

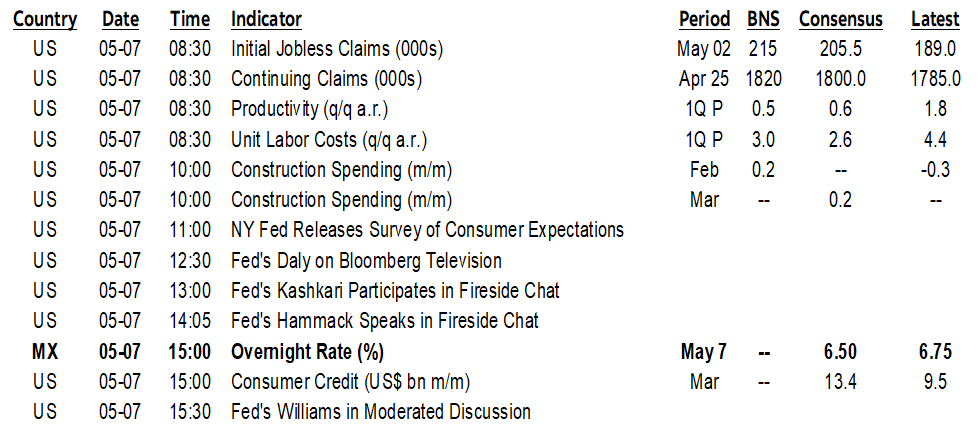

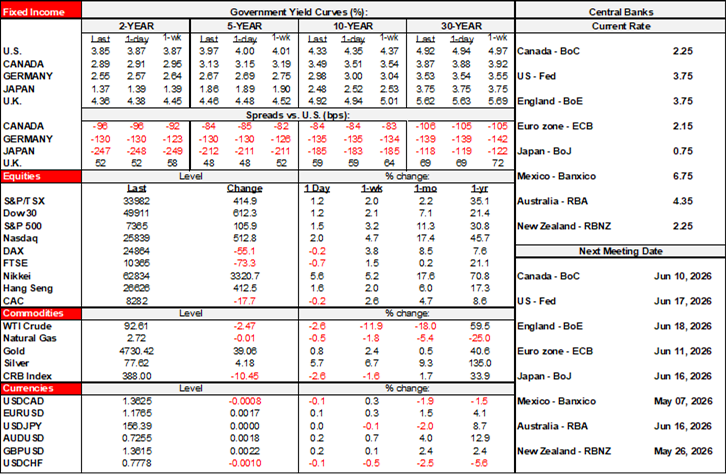

A limiting factor is that Banxico’s policy rate spread over the Federal Reserve is toward the tights and with the FOMC not sounding like it’s in a hurry to cut with the hawks lining up (chart 1).

MACRO RELEASES

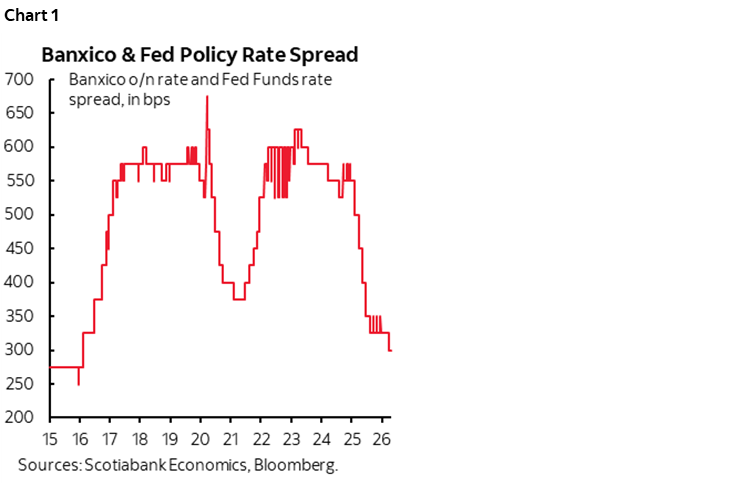

German factory orders soared in March. The 5% m/m SA gain was five times what consensus expected, followed a 1.4% prior gain albeit after contracting by 11% in January. Orders have been up in six of the past seven months (chart 2). Consumer goods led the way in March (+7.3% m/m) but capital goods also contributed (2.1%).

Mexico updates CPI for April (8amET) ahead of Banxico’s decision. The 0.3% m/m expected rise is rarely surprised because Mexico releases inflation figures on a bi-weekly basis, given local analysts a running head start at the estimate.

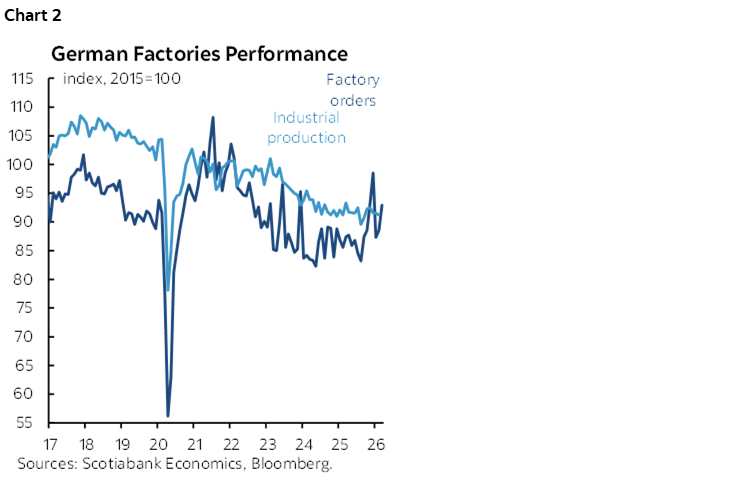

US job cuts increased to 83.4k in April (60.6k prior). The volatile pattern is shown in chart 3. There should be little effect on nonfarm expectations tomorrow.

Several US releases will pass the time ahead of payrolls tomorrow.

- Q1 labour productivity (8:30amET): Productivity may have been weak again in Q1. A rise of only around ½% q/q SAAR is expected and is based on nonfarm output and nonfarm hours. Such a print would follow 1.8% productivity growth in Q4 after two quarters in the 4–5% range.

- Q1 unit labour costs (8:30amET): Productivity-adjusted labour costs probably jumped as a consequence of the slowdown in productivity growth. I expect a figure of around 3% q/q SAAR.

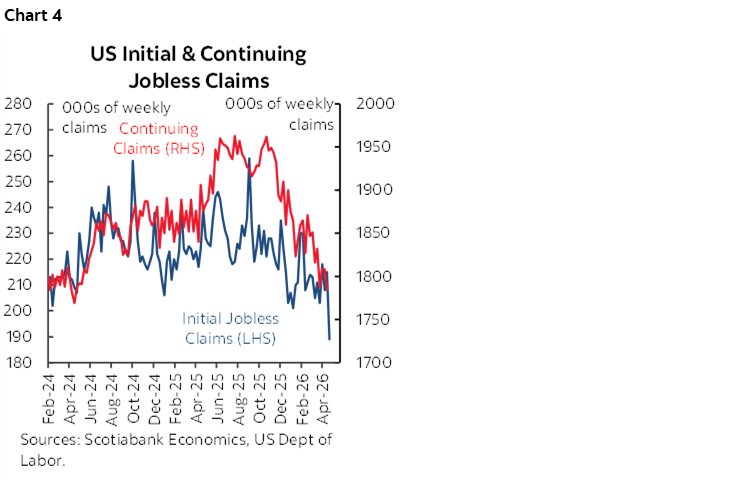

- Weekly jobless claims (8:30amET): Was the prior week’s drop in initial jobless claims merely an aberration (chart 4)? We’ll find out, alongside answering the same thing for a more persistent downward trend in continuing claims that points to a falling unemployment rate.

- Construction spending (10amET): A small gain is expected to have occurred in March.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.