ON DECK FOR WEDNESDAY, MAY 6th

KEY POINTS:

- Iran deal optimism drives oil lower, risk-on sentiment that may be premature

- The US proposal to end the war awaits Iran’s approval…

- …would grant Iran some of what it has demanded all along…

- …and would therefore be hard not to see as victory by Iran…

- …but Iran may yet reject it because it doesn’t address several other demands

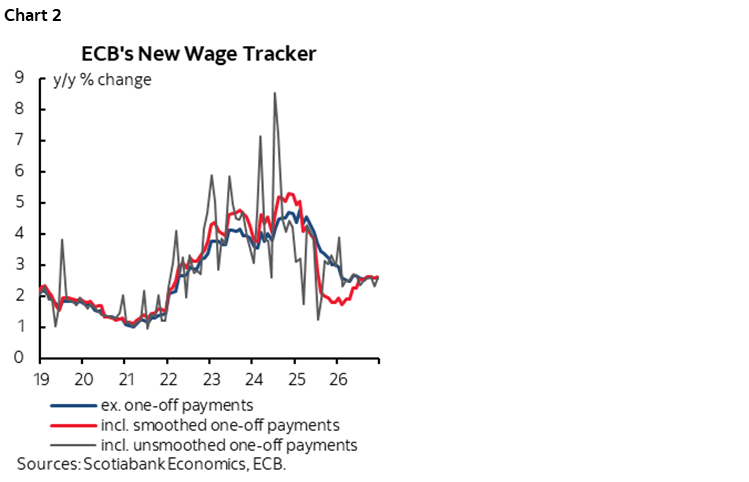

- ECB wage tracker ebbs, but it’s too early to assess second-round effects

- NZ put up mixed labour market readings

- US ADP payrolls expected to be solid

- BoC testimony is not expected to offer anything new

- Mixed regional inflation reports

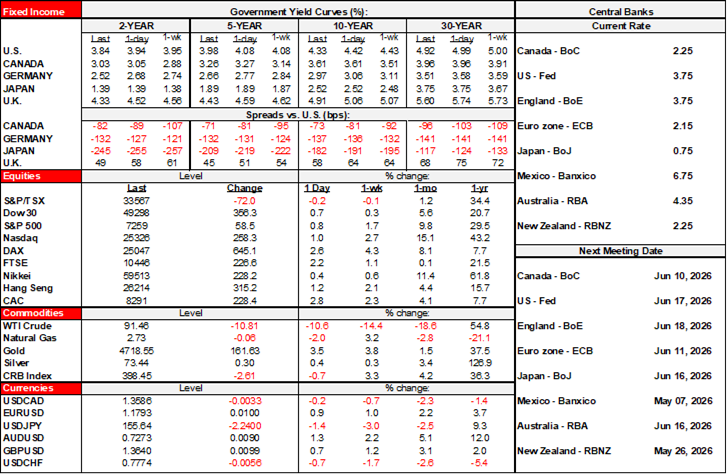

The rumour mill that the end of the war with Iran may be near has markets buying it with few questions asked when perhaps many remain. Oil is off by almost $10. Sovereign bond yields are down across the board and by double digit basis points in parts of European curves. Stocks are pushing higher, again led by Europe where the gains are in the 2–3% range. The dollar is broadly weaker, but oil crosses like CAD and NOK are underperforming. Central bank moves are being slightly repriced. Much of this is a reflection of algo/robot trades but perhaps some well placed folks are making a lot of money again.

WHAT’S IN, AND WHAT’S OUT OF THE RUMOURED PROPOSAL?

It all traces back to an article from Axios shortly before 5amET, the media world’s rumour mill extraordinaire. Axios quotes two anonymous US officials and two other unreferenced sources. If what they are reporting is true and ultimately agreed upon, then Iran is winning. Iran reportedly has 48 hours to consider a US proposal that reeks of increasing desperation. The US officials are reportedly mixed on whether a deal can truly be achieved which might be because the Iranian regime is divided and several of its prior demands are not being met.

Axios reports that the US offered to lift sanctions against Iran, unfreeze Iranian assets, and allow Iran to merely commit to a moratorium on nuclear enrichment while both sides fully open the Strait of Hormuz. This isn’t a US proposal. It is exactly what Iran demanded at earlier stages! So, the US went through all that only to propose a deal that couldn’t secure and remove Iran’s enriched uranium. Couldn’t get them to give up their nuclear program. Couldn’t remove the old regime. A regime that is angrier in a more fractured middle east. A regime that will rebuild.

What is not mentioned as part of the proposed deal but that Iran has previously demanded includes:

1. A complete cessation of the adversary’s “aggression and assassination” operations.

2. Establishment of concrete mechanisms to ensure the war is never again imposed upon Iran.

3. Guarantees and clearly defined procedures for payment of compensation and reconstruction costs resulting from the war.

4. Cessation of hostilities across all fronts and across all resistance groups involved throughout the region.

5. International recognition and guarantee of Iran’s sovereign right to exercise jurisdiction over the Strait of Hormuz.

Some of these should be non-starters, but their apparent omission suggests that markets are being a touch too quick to conclude that Iran will accept the proposal and that the war’s over. If it is, then the proposal indicates that Trump clearly has his eyes on the midterms, his very low polling, and getting energy prices lower as the war drains Treasury and hits Americans in their pocketbooks. Who’s crying Uncle?

LIGHT OVERNIGHT AND N.A. DATA

Nothing else is even worth mentioning by way of market effects that the proposed deal is dominating, so we can be quick.

New Zealand’s labour market put up mixed numbers overnight. Job growth cooled in Q1 (0.2% q/q SA, 0.3% consensus, 0.5% prior) but the unemployment rate dipped a tenth to 5.3% and wage growth ex-overtime accelerated (0.5% q/q, 0.4% prior and consensus). Chart 1.

Three countries released April CPI reports. Swedish CPI surprised lower at -0.6% m/m (-0.2% consensus) with underlying prices dropping by 0.6% m/m (-0.1% consensus). South Korean CPI landed on the screws at 0.5% m/m. Thai CPI jumped by more than expected (2.8% m/m, 2.1% consensus).

The Eurozone’s wage tracker gave the ECB a bit of good news as it worries about second-round effects of high commodities and inflation (chart 2). Wage growth is expected to rise by 2.6% in 2026, slightly down from 3% last year and steady in April over March. It may be too early to assess second-round effects on wage pressures.

US ADP payrolls are due (8:15amET) and expected to jump by 150k m/m based on their weekly tracking, but very commonly throw off misleading signals for private nonfarm payrolls. Treasury investors will keep an eye on the quarterly refunding announcement (8:30amET) that now risks getting lost behind bigger headlines.

Nothing new is expected from the second round of BoC parliamentary testimony because, well, nothing new was offered in the first round on Monday! Canada also updates the little-watched Ivey PMI for April (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.