ON DECK FOR TUESDAY, MAY 5th

KEY POINTS:

- Markets vacillate between peace on-and-off sentiment

- RBA hiked again, signals pause

- Mixed signals in Canadian trade

- US Trade, ISM-services, JOLTS, new homes sales on tap

- Philippines inflation reinforces further BSP hike

- Global Week Ahead reminder here

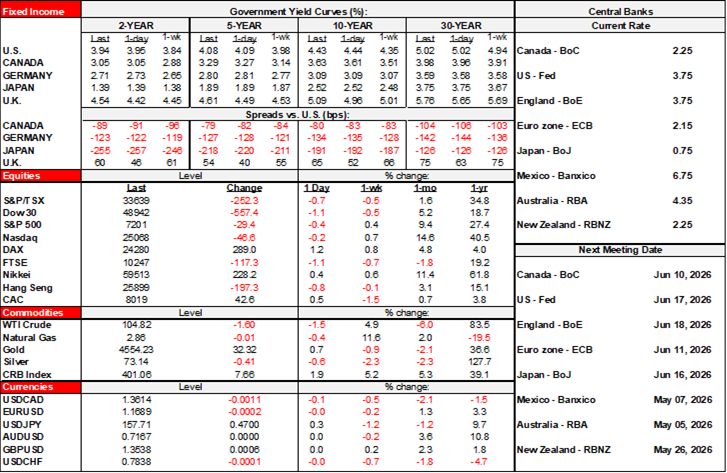

The on-and-off peace trade is on again this morning after being off yesterday and who knows which direction tomorrow. Oil is retaining most of yesterday’s jump in Brent and WTI but giving back a couple of bucks this morning. UK gilts are underperforming by the most as they catch up to yesterday’s developments in energy and bond markets following yesterday’s UK bank holiday. BoC hike pricing remains near 60bps after bland BoC testimony yesterday afternoon. Equities are mostly higher except for London after the bank holiday.

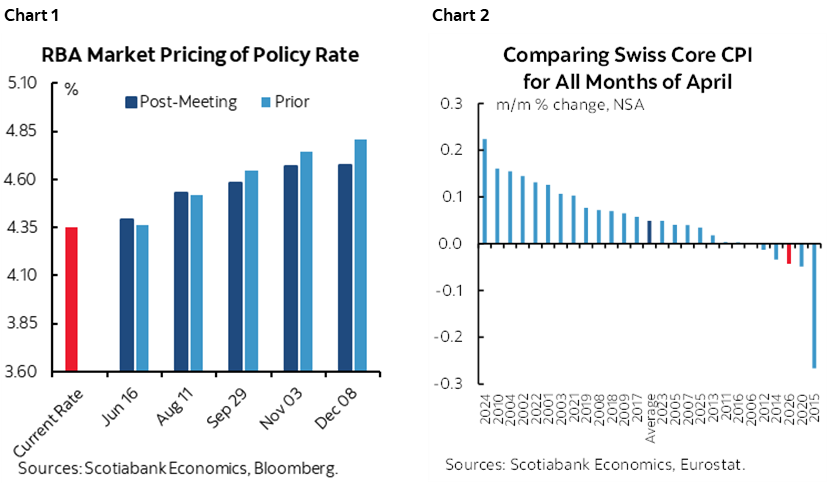

Overnight developments brought out a dovish hike by the RBA with markets still pricing future hikes (chart 1), light Swiss core CPI (chart 2) and a big jump in Philippines CPI that sets up another coming hike. Canadian and US macro reports are on tap into the N.A. open.

RBA Hikes, Sets Up a Pause Ahead of Budget

Australia’s central bank hiked its cash rate target by 25bps to 4.35% overnight as expected by all but one in consensus. The A$ is slightly underperforming other major crosses and Aussie rates mildly rallied in slight bull steepener fashion because guidance suggested a near-term pause after three consecutive rate increases. Governor Bullock stated “On reason to increase interest rates was to give ourselves space now to sit and see what happens. We feel we’re now in a position where we’ve got space to be alert now to both sides of the risks to inflation—upside and downside.” Markets are mostly pricing a pause at the next decision on June 16th but lean toward a further 1–2 quarter point hikes being priced by year-end. Australia’s Budget next Tuesday and further developments in commodities markets will be monitored.

Philippines CPI Reinforces Further Tightening

Inflation in the Philippines accelerated to 7.2% y/y in April (5.5% consensus, 4.1% prior) as prices jumped by 2.6% m/m (1.2% consensus). The peso slightly outperformed post-release with markets leaning toward another hike on June 18th after BSP raised its overnight rate by 25bps on April 23rd.

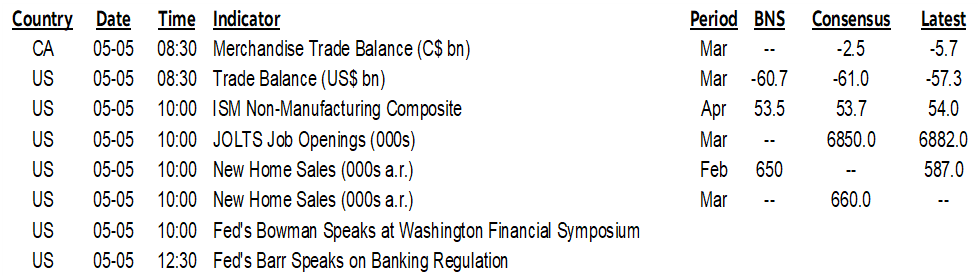

CANADA-US MACRO REPORTS

Canada and the US will refresh trade figures for March (8:30amET). The US trade deficit widened in March based on the advance goods balance with the usually stable services balance to be added in this morning’s figures.

Canada’s goods trade is tracking a wider deficit in Q1. Before March’s figures, exports are tracking a drop of about 12% q/q SAAR with imports tracking a gain of over 9%. Trade as captured in GDP accounts is tracking a considerably bigger import gain and smaller export drop. This follows two quarterly gains in exports and little net movement in imports. There is significant breadth to the Q1 export decline and significant breadth to the jump in imports, pending March’s figures. For instance, imports of equipment are up 17% q/q SAAR which matters because Canada imports most of its capital goods. Imports of autos and parts are up by close to 6% but imports of other consumer goods are off by about 3%.

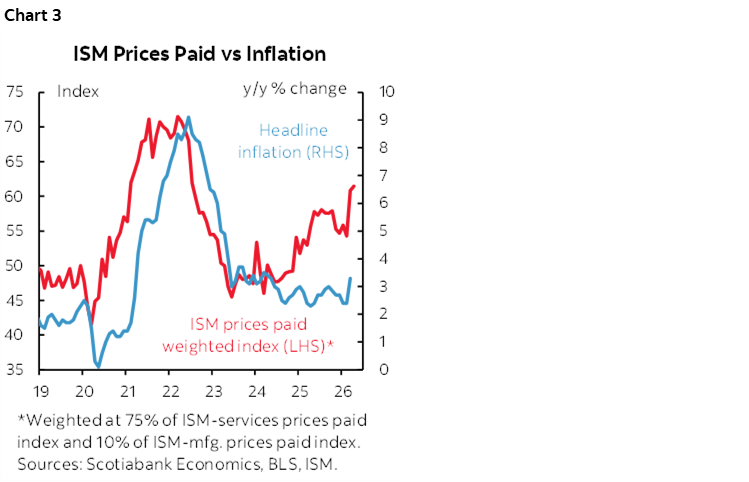

The US then releases a trio of figures at 10amET. ISM-services will inform growth, hiring and price pressures in the services sector during April. New home sales should be updated with February and March readings. JOLTS job openings, quits and layoffs during March will be among the set ups to Friday’s nonfarm payrolls. Key may be the extent to which ISM prices-paid signals continue to evolve as a leading indicator of future CPI inflation (chart 3).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.