ON DECK FOR FRIDAY, MAY 22nd

KEY POINTS:

- Markets offer a nice segue into a US long weekend

- Fed’s Waller to speak on the outlook

- Canadian consumers likely had a strong Q1 into Q2 uncertainty

- Canadian producer prices may further inform pass through to consumer prices

- UK consumers had a strong Q1, start Q2 by taking a breather

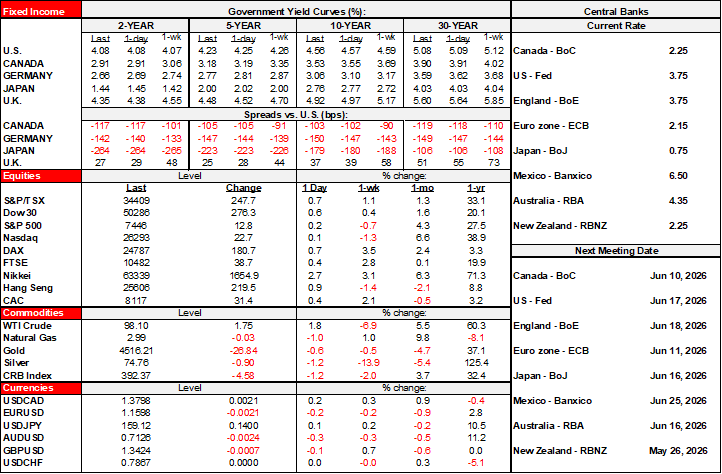

Well, it’s not a bad segue into a long weekend for Americans. Stocks are a touch higher across the board. Global sovereign bond prices are higher as well with the US 10-year yield now about 13bps off the peak since just a couple of days ago. The dollar is broadly firmer but only gently so against the majors.

The one outlier is the won which depreciated again overnight, prompting the Finance Ministry to remark that the moves have been “excessive relative to fundamentals and will take decisive action if necessary”. Cue next week’s BoK decision but most have a hold. The won has been a train-wreck since the middle of last year after which it depreciated by about 12% to the dollar which further complicates the picture for inflation risk.

Light Canadian and UK data and a speech by a top Fed official are highlighted below.

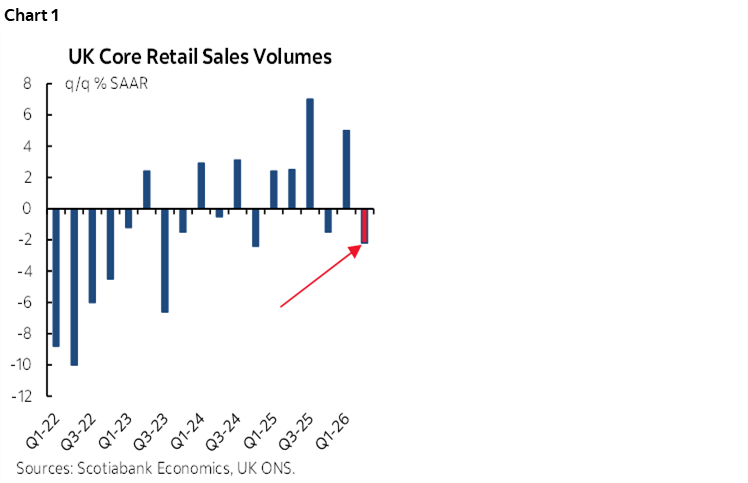

UK CONSUMERS TAKE A BREATHER

UK retail sales volumes disappointed with a 1.3% m/m drop in April (-0.6% consensus) mostly due to lower fuel sales volumes. Sales ex-fuel slipped by -0.4% m/m. UK consumers are coming off a strong Q1 advance during which core retail sales volumes grew by 5% q/q SAAR (chart 1). Very tentative tracking for Q2 is pointing to about a 2% pullback through a combination of a strong jumping off point and economic uncertainty.

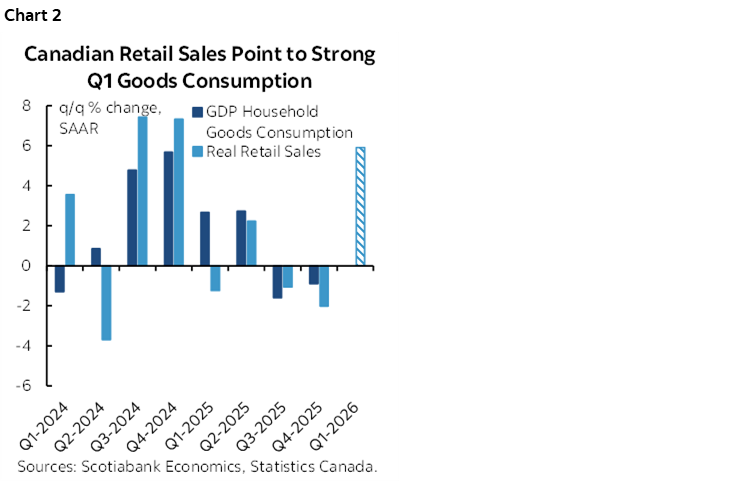

CANADIAN CONSUMERS LIKELY HAD A SOLID Q1 INTO Q2 UNCERTAINTY

Canada follows suit with updated retail sales figures for March and April plus any revisions. Advance guidance from Statcan on April 24th indicated March was tracking a nominal sales gain of 0.6% m/m SA. That can often be off by a lot and so revision risk is in play along with important details like volumes. The first estimate for April is due with it.

Barring massive revisions in either direction, we’re tracking retail sales volume growth of around 6% q/q SAAR in Q1. Based on historical connections, that could imply that inflation-adjusted consumer spending on goods in the GDP accounts may be tracking around 4%+ q/q SAAR (chart 2). Like the UK case above, tentative tracking for Q2 will be offered, except it will be more tentative than the UK case because Statcan’s early read on April will only be for nominal sales (not volumes) and will not contain any details; such teases. The picture we could be left with is a strong Q1 after a tepid second half of 2025.

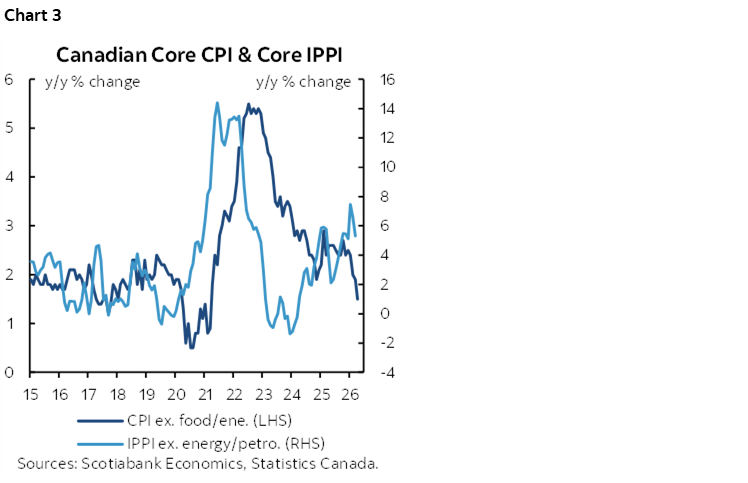

CANADIAN PRODUCER PRICES TO INFORM LAGGING CONSUMER PASS THROUGH

Canada also updates industrial and raw materials prices with April readings (8:30amET). Only folks with time to waste submit random guesses for these readings so ignore the very thin consensus. An updated version of chart 3 is what I’ll be interested in seeing. Some of my street colleagues pounce on m/m readings and miss the plot. The broad trend to the volatile readings is unambiguously pointed higher and suggests pass through risk into consumer prices with a lag as shown in the chart. What happens to CPI and core CPI will be patiently observed as we remain at a highly nascent stage for evaluating inflationary pressures driven by pre-war and wartime influences.

FED’S WALLER STANDS OUT ON A QUIET CALENDAR

US markets will be focused on answering questions like what are you bbq’ing, who is invited, what’s your favourite beer, are you watching the game etc. It’s the Memorial Day long weekend and bonds get an early close at 2pmET while equities don’t get one, or at least not officially.

Fed Governor Waller’s speech at 10amET may be insightful. He’ll talk about the economic outlook. Waller hasn’t delivered a speech on economics since April 17th and since a lot has happened since then his views may help to inform a bias into the June FOMC when fresh forecasts and dot plot guidance will be offered.

HUM DRUM JAPANESE INFLATION

Japanese inflation was consistent with earlier readings for Tokyo. CPI in April was up by 1.4% y/y with ex-food up 1.4% and ex-food and energy up 1.9%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.