ON DECK FOR WEDNESDAY, MAY 20th

KEY POINTS:

- Bond sell off turns to global rally led by gilts

- FOMC minutes — how many prefer striking out that one line?

- The FOMC would be terribly unwise to overreact to recent bond market gyrations…

- ...as Treasurys may have approached the outer bound of sustainable yields…

- ...and most members should be patient toward evaluating dual mandate pressures

- UK CPI sparks rally in gilts...

- ...with BoE’s Bailey to react in pending testimony

- German producer prices undershoot, but were not light

- BI’s wild west approach stuns with 50bps hike

- Nvidia earnings on tap in the after-market

Hopefully experienced bond investors didn’t overreact to yesterday’s price plunge. Yields are backing off this morning and with modest conviction I’m of the view that US Ts are getting looking cheap to more patient investors (see below).

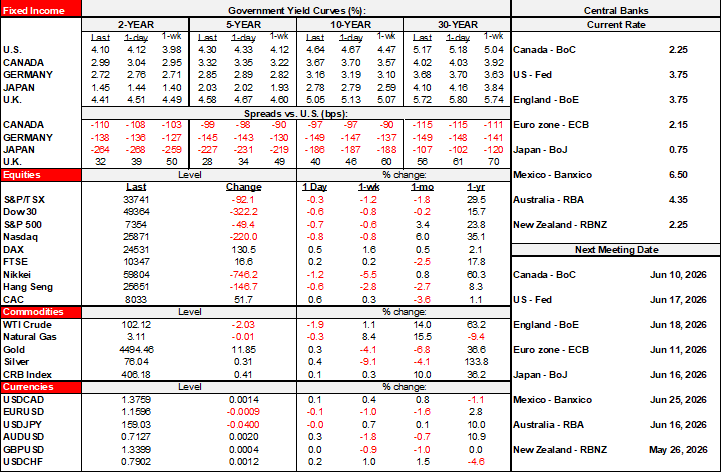

For now, sovereign yields are falling everywhere this morning and led by the UK which may be an overreaction to UK CPI. Oil prices are off by $2 or so, until some powerful person decides to front-run his own headline risk. Stocks are broadly higher by about ¼% to ¾% across major global benchmarks outside of Asia that merely followed yesterday’s US sell off. Currencies are mixed.

Overnight developments were focused upon UK CPI, German producer prices and a Bank Indonesia shocker. The North American session will focus upon FOMC minutes this afternoon (see below) and then Nvidia’s earnings in the after-market. As others claim that yesterday’s Canadian inflation report merits standing by forecasts over the year-ahead or changing them, I’d advocate being more patient; nothing got settled by a mixed report at a highly nascent stage of developments yet much of the commentary from other street shops was overly emotional and reactionary if not downright silly.

Gilts Rally Post CPI—BoE’s Bailey on Tap

Sterling is underperforming and gilts are outperforming with a bull steepener that has the 2-year yield down 10bps this morning. The catalyst was UK CPI that landed a bit beneath expectations.

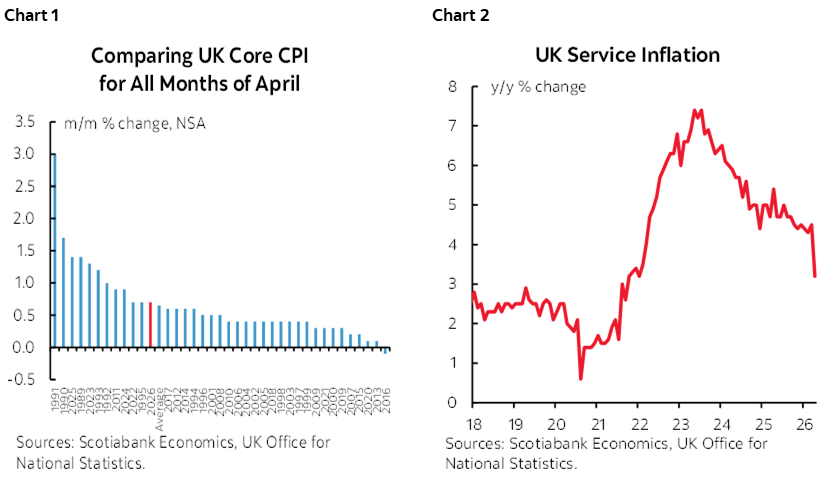

CPI was up by 0.7% m/m NSA (0.9% consensus) which was around the long-run average for like months of April (chart 1) and when combined with a shift in year-ago base effects this drove the y/y rate down half a point to 2.8% (3.3% prior, 3.0% consensus). Last April, CPI soared by 1.2% m/m NSA which was much warmer than usual for a month of April and this distorted the year-over-year math. Core inflation undershot for similar base effect reasons (2.5% y/y, 2.6% consensus, 4.5% prior) but also because the m/m seasonally unadjusted change of 0.7% was merely average for like months of April over time. Services inflation ebbed to 3.2% y/y (4.5% prior, 3.5% consensus) as shown in chart 2.

The most sensible commentary I’ve seen on the implications for the Bank of England emphasized more wiggle room and flexibility to continue assessing the inflation shock. One single report at such a nascent stage for developments and their impact upon data shouldn’t be viewed as changing a great deal about the rest of the year’s expectations and beyond. We’ll see what Governor Bailey thinks during his testimony before Parliament this morning (9:15amET).

German Producer Prices—Below Consensus, but Not Light

German producer prices climbed by less than feared but don’t confuse that as evidence they were light. Producer prices were up by 1.2% m/m NSA in April (2% consensus) after a 2.5% rise in March. Those are the hottest back-to-back gains in producer prices since 2022. Ex-energy producer prices jumped by 0.5% m/m NSA after a 0.4% rise in March for the warmest back-to-back readings since early 2023. Not light.

Bank Indonesia Stuns

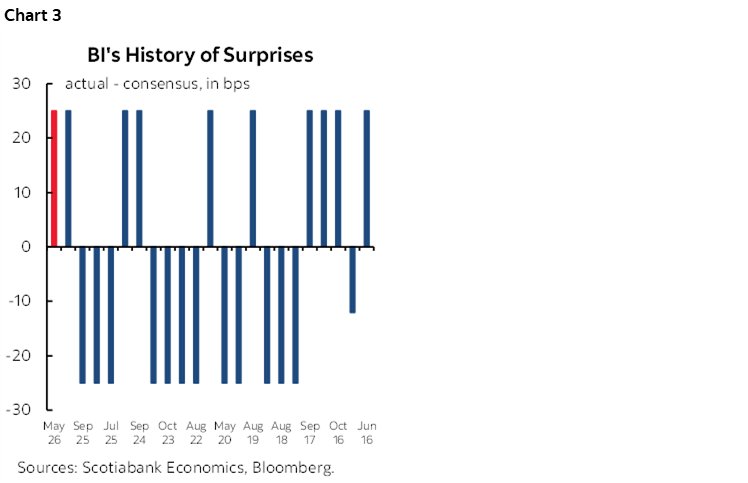

Indonesia’s reputation as the wild west of central banking was reinforced overnight. Bank Indonesia hiked its policy rate by 50bps versus all but one within consensus who were in the hold or 25bps hike camps. Guidance isn’t BI’s thing and it has a long history of volatility and surprising markets (chart 3). Clearly the aim was to address rupiah stability and it worked, for now. The rupiah appreciated sharply and is among the few strongest crosses to the USD in the aftermath. Concern about an oil- and currency-driven inflation and uncertainty around potentially expansionist fiscal policy prompted the move.

FOMC Minutes—Stability Needed

Minutes to the April 28th–29th FOMC meeting land at 2pmET today. I don’t expect much and hope we see signs of a steady hand on the tiller.

Key will be reference to the number of Committee members that prefer striking out the statement-codified reference to possible further easing that went as follows: “In considering the extent and timing of additional adjustments to the target range for the federal funds rate….” That implies an ongoing easing bias.

We know that three voting FOMC members (Logan, Kashkari and Hammack) dissented in favour of removing this reference. One additional nonvoting member (Collins) then came out supporting this stance. That makes for three out of twelve voting Committee members who preferred this option and four in total. The minutes will likely employ language such as ‘a few’ or ‘some’ or perhaps ‘several’ members preferring this option while ‘most’ or ‘a majority’ supported continued inclusion of the sentence.

If a greater number of members opposing inclusion of the sentence is revealed, then the front-end may sell off further or at least be validated. If I’m right and it’s still just a minority, then there could be a modest front-end rally.

In any event, this is a Committee that collectively only has one further cut this year and one more next year in the last set of dots/SEP that are poised to be updated in June. They have five more meetings on the docket this year. It would be silly to overreact to inflation and to overreact to the bond selloff at this juncture.

Why? For starters, markets are reacting to what can be readily and quickly observed which is prices. How growth and the full employment side of the dual mandate evolve is a much more patient debate that will be informed with lagging effects over time. It wouldn’t be terribly wise as a policymaker to a) assume US inflation risk will permanently challenge and b) that the job market and growth will hold up. Jobs might, but the downside risks to the outlook have risen with falling participation rates especially over-55, the energy shock, AI, tighter immigration, and weakening consumer fundamentals. Should the full employment side of the dual mandate waver and inflation temporarily overshoot then greater balance could be restored to the debate going on in markets but we won’t get the answers to this now, or next month, or the next one etc. We’ll get the answers gradually over time.

Also, the Committee would be rather wet-behind-the-ears should it overreact to the very recent bond sell off that has taken the 10s yield up by about 30–35bps since late April. First, that’s small in the grand scheme of bond moves.

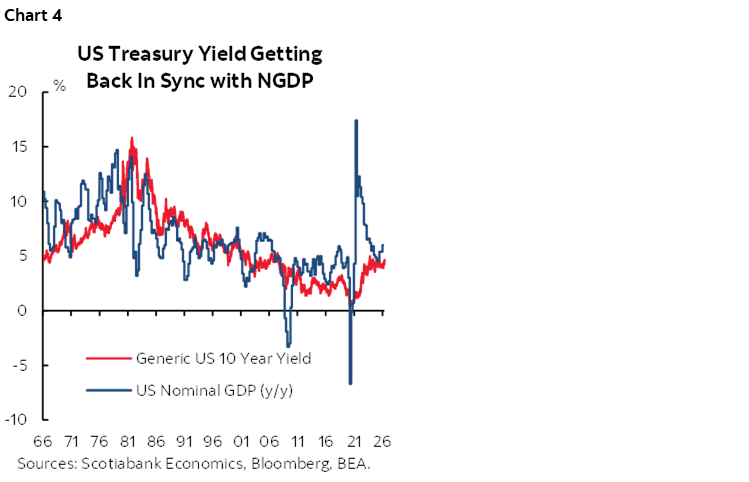

Second, over time the 10-year should ride around NGDP expectations (chart 4). Assumptions around potential real GDP growth plus long-term expected inflation would be a stretch to get up to 4.65% let alone sustainably higher toward 5%.

Third, there is a very, very high bar to the FOMC pivoting toward hikes as a consensus call with a new incoming Chair in Kevin Warsh. It would be the granddaddy of all about-faces for him to sound so dovish in the interview period and then pivot toward a hawkish stance in June and I don’t sense anything close to quorum in favour of entertaining hikes. Some say credibility requires striking out the sentence to contain the market; I say credibility requires not strongly pre-judging complex forces or overreacting to very recent market gyrations! One reason for this is that the Fed is already restrictive by contrast to many other global central banks like the BoC, ECB, BoJ etc. The policy rate is above most reasonable estimates of neutral and the dots already signal a Committee bias toward staying restrictive even at year-end and arguably even next year.

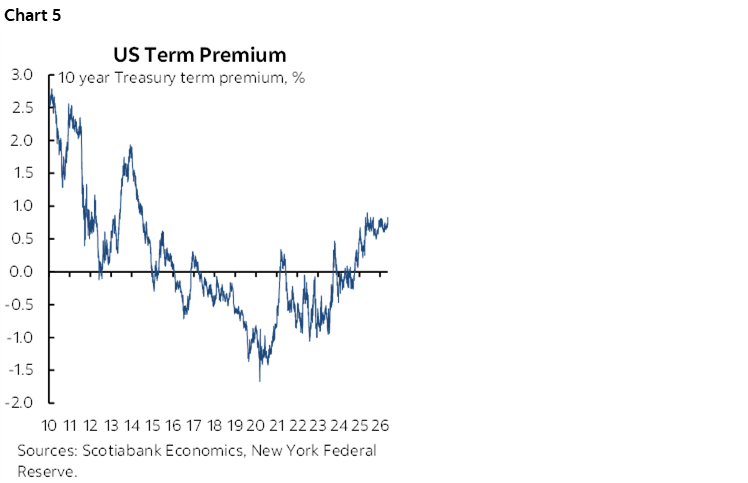

Fourth, term premia have risen (chart 5) but very suddenly against a historical pattern of abrupt swings and the estimated 10-year term premia from the NY Fed’s economists has only gone up by around 10bps above trend.

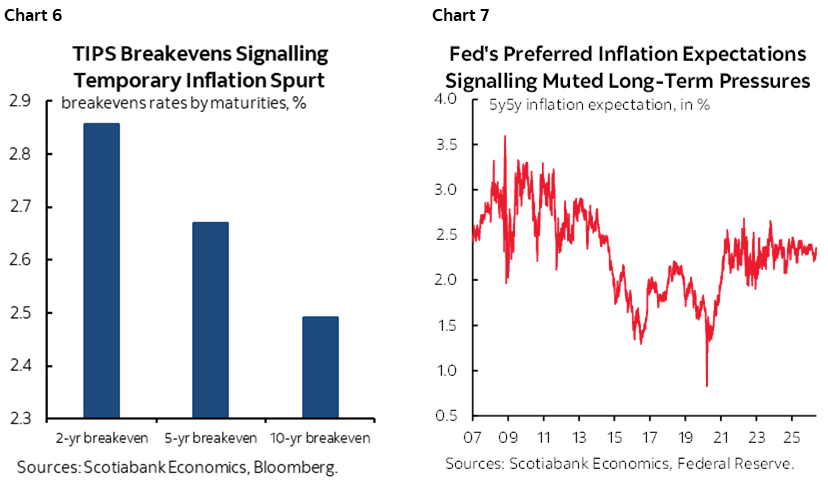

Fifth, inflation pricing has moved higher but mostly across nearer-term expectations. The US 2s breakeven rate has increased to 2.85% with the 10s breakeven at 2.5% (chart 6) while the Fed’s preferred five-year forward breakeven rate has moved up to about 2.35% (chart 7). I don’t put a lot of faith in measures of inflation expectations from markets or surveys, but for what it’s worth, the market is signalling this may be more of a short-lived inflation shock to the US that policy shouldn’t overreact against.

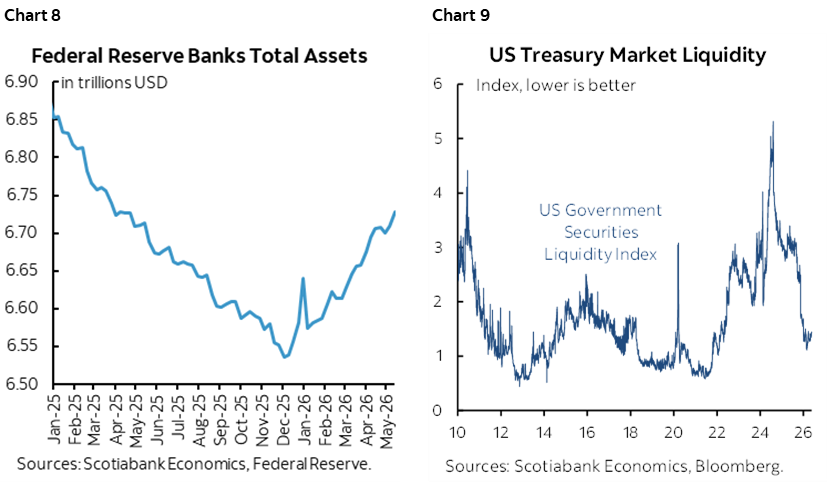

Sixth, it’s not clear that liquidity has been impaired to the point to which bonds are suffering. Far from it in my opinion. For instance, reserves continue to climb to US$6¾ trillion (chart 8). Measures of bond market liquidity are healthy; chart 9 shows one whereby lower is better because it measures deviations from estimated fair value on an equally weighted portfolio of Treasury securities.

There are many more potential drivers of bond yields. Among the ones not discussed above are intangibles like sentiment. Frankly, we need to call out market manipulation as a risk to the Treasury market. Investors face enough uncertainty. They cannot also deal with EM-like tendencies whereby policy front-running by the administration creates a more uncertain investing regime at higher risk.

Overall, however, I’m of the view that a lot of the commentary is engaging in pile-on behaviour. Can’t beat ‘em, join ‘em is the logic. Experienced forecasters have seen many sudden bond market moves and normally set a high bar to be knocked off longer-run views by short-term moves.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.