ON DECK FOR FRIDAY, MAY 15th

KEY POINTS:

- Markets unimpressed by US-China Summit thus far

- Summit developments point to potential one-offs versus any grand bargain

- UK economy was doing pretty well before the war’s effects

- US retail sales update to inform weak consumer spending

- US import prices likely to surge, fade jobless claims

- Canada to update minor data

- Peru’s central bank expected to hold ahead of coming election

Thus far, markets have thin gruel to trade on by way of anything substantive out of US-China talks during Trump’s visit to China with son in tow pursuing family business. That may change on the path to tonight’s second meeting between President Xi Jinping and Trump following this morning’s state banquet.

Yet so far, it’s almost as if the US side is pumping up simply worded positive rhetoric while China generally resists and warns the US about Taiwan. My impression is that the optics are more about China asserting control. Expectations were pretty low going into the trip as Trump is the eleventh foreign leader to travel to China this year while Xi stays home. China’s power and stature are rising on the world stage.

The timing of any communiqué and other announcements is uncertain. All we have to go by is talk—no announcements—on potential around a ‘Board of Investment’ and a ‘Board of Trade’ that could open up more room for China to invest and trade with the US, while Xi loosely pledged to open up China a little more to US businesses. There is also general talk of China buying more US agricultural products and planes and the US seeking to sell more oil to China in which case it should get in line. These sound like small one-offs against any grand bargain that wasn’t expected in any event.

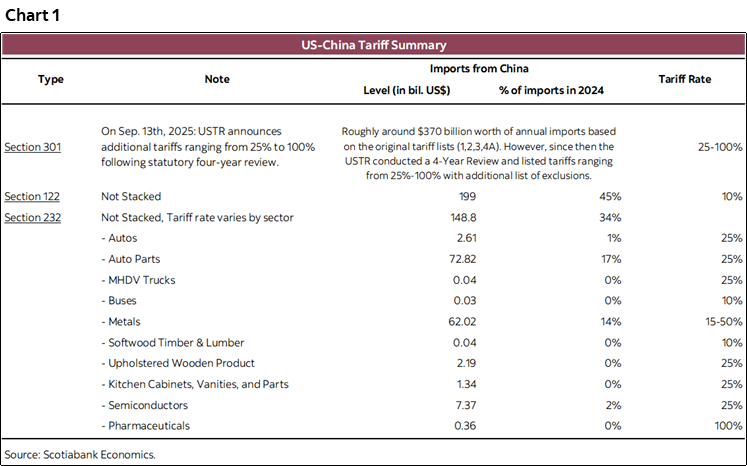

What markets would be interested in seeing would be any substantive progress toward meaningfully reducing tariffs shown in chart 1. Advance rumours suggested reducing tariffs on about 10% of US imports from China but the details are unknown.

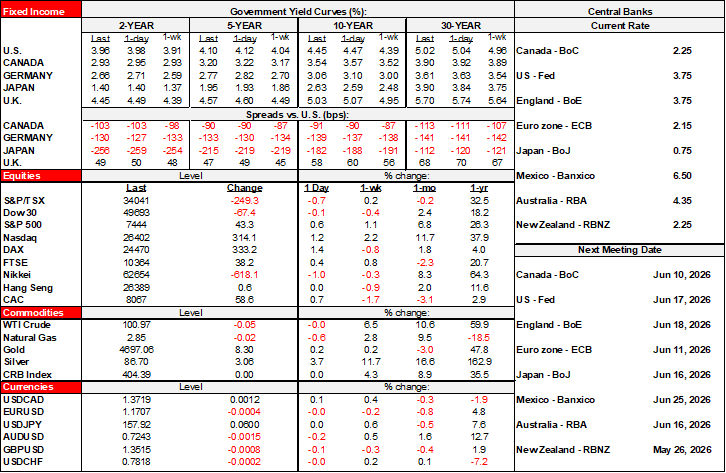

As such, markets are generally little changed this morning. Stocks have a small positive bias. So do bond prices. Oil is little changed. Ditto for major currencies.

N.A. TO FOCUS ON THE WEAK US CONSUMER

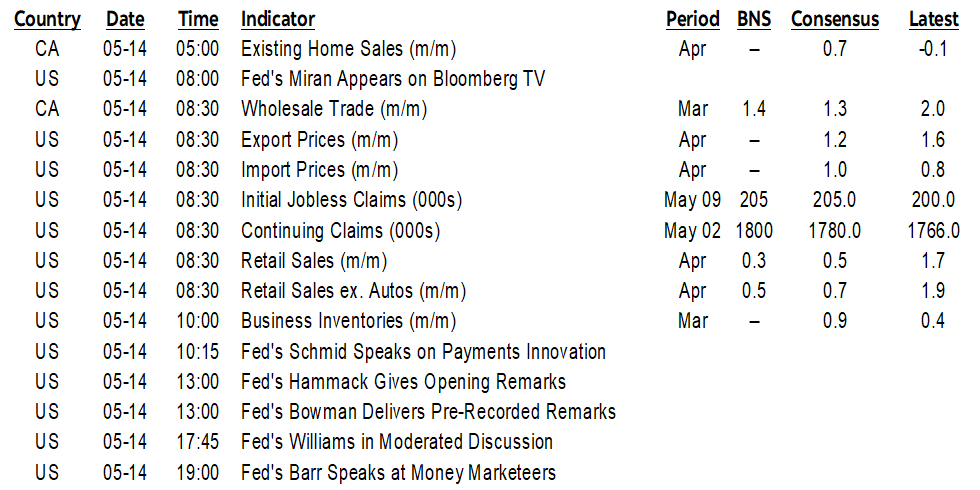

US retail sales in April will be the main N.A. reading (8:30amET) and it is expected to post a moderate nominal advance driven by a small gain in core sales, higher gasoline and other prices, and a decline in new vehicle sales. Growth in inflation-adjusted sales has stalled for several quarters with just 0.7% q/q SAAR growth in Q1 after -0.4% in Q4.

US inflation watch will continue with import prices for April that are likely to post another large rise (8:30amET). US jobless claims are also due (8:30amET) and see my weekly that included a view on why claims have been falling.

Canada posted a minor rise in existing home sales last month (0.7% m/m SA) after a string of soft readings and going into the heart of the Spring housing market (chart 2). Additional minor data will be delivered when wholesale sales during March are expected to post a strong gain (8:30amET). The bigger news was the positive development for democracy in Alberta after the Court of King’s Bench of Alberta rejected the list of signatures and blocked a possible vote on separation. Premier Smith’s close alignment with the separatist movement has pledged to appeal.

UK ECONOMY WAS DOING WELL BEFORE THE WAR’S EFFECTS

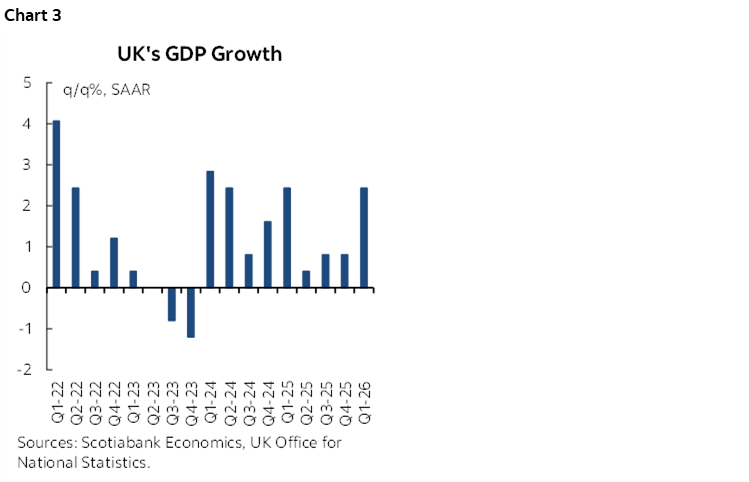

- The UK economy put in a solid performance across various readings but markets largely ignored them as stale on arrival. More important data on jobs, wages and inflation arrives next week.

- Q1 GDP landed on consensus at 0.6% q/q SA nonannualized. Annualized growth is shown in chart 3. Consumption grew by 0.6%, investment slipped by -0.6%, and net trade shrank as imports (+0.6%) outpaced exports (0.1%).

- Monthly GDP for March continued to grow strongly. It was up by 0.3% m/m after 0.4% the prior month.

- Industrial production shrank by -0.2% m/m despite manufacturing output being up by 1.2% m/m in March.

- Services expanded by 0.3% m/m after 0.5% the prior month.

- the net trade deficit widened considerably in March as imports soared (+5.3% m/m) while exports were little changed (0.2%).

PERU’S CENTRAL BANK ON HOLD

Peru’s central bank is widely expected to hold at 4.25% tonight (7pmET) ahead of the June 7th final Presidential run-off. That vote is a classic right versus left contest in which the leftist candidate was just charged for financing irregularities.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.