ON DECK FOR TUESDAY, MAY 12th

KEY POINTS:

- Oil continues to climb as US-Iran rhetoric heats up

- US CPI both extends and starts tracking of second-round effects

- Gilts underperform on inflation risk plus political uncertainty

- US Budget to temporarily swing into seasonal surplus

- Australia’s budget was a yawner…

- …but embraced a dicey path toward addressing housing affordability

Oil prices continue to rally and are back up to where they were last Wednesday before sliding in false anticipation of a US-Iran deal. WTI and Brent are up by about $3–4/barrel this morning with Brent at almost $108. Higher oil prices yesterday and today follow Trump’s ineloquent dismissal of Iran’s counter-offer as “a piece of garbage” while saying the ceasefire that isn’t much of a ceasefire is “unbelievably weak” and on “massive life support” which somehow seeks to draw a distinction from garden variety life support.

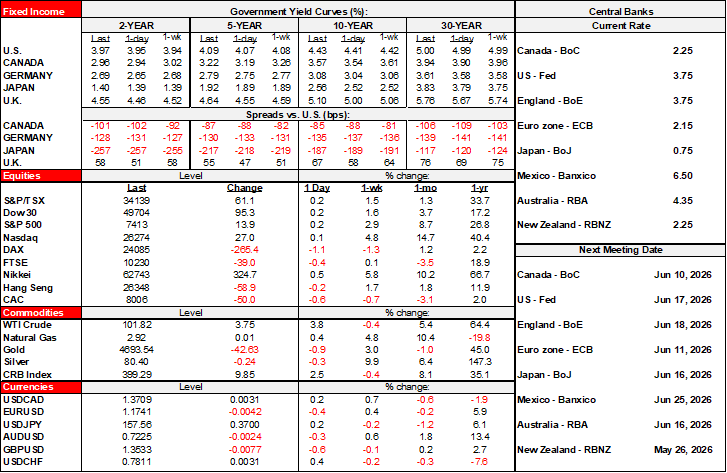

Bond yields are accordingly higher on a perceived increase in inflation risk. Gilts are underperforming with borderline double-digit basis point increases at the longer-end while all other major markets are cheaper by single digit moves led by Europe. Gilts have inflation worries and political instability on the mind as PM Starmer digs in against a rebellious cabinet that is stoking fear that a freer-spending leader could step in. Stocks are broadly lower by up to 1% in Germany. The dollar is generally firmer against major crosses but with oil-driven currencies like the krone and CAD outperforming others. Iran countered with a take-it-or-leave-it posture and noted it was “ready to respond and to reach a lesson for any aggression.”

And so, with that as the backdrop, it only seems appropriate to talk inflation.

US CPI—THE LONG MARCH OF SECOND-ROUND EFFECTS

US CPI for April (8:30amET) and tomorrow’s producer prices will set the stage for the last PCE inflation reading before Kevin Warsh takes the helm at the Fed although there will be another CPI release just before the June FOMC. This one is expected to be warm and tentatively begins the tracking of second-round inflation effects stemming from the surge in commodities layered onto pre-existing passthrough impulses.

Gains of 0.7% m/m (0.6% consensus) and 0.4% (0.3% consensus) are expected for headline CPI and core ex-food and energy. The year-over-year rates should rise to the high 3% and high 2% range for total and core CPI respectively.

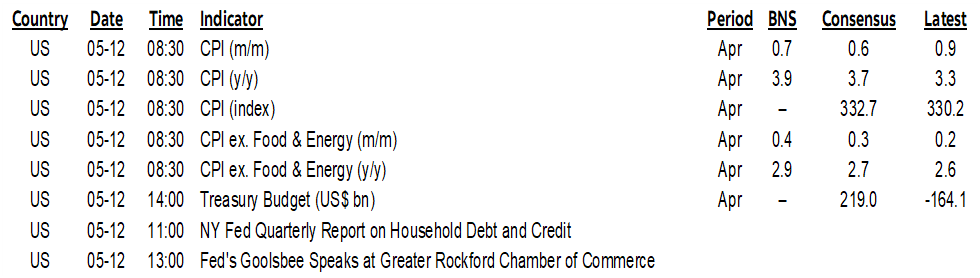

See my weekly for discussion of some of the drivers to the call. Watch the breadth of price increases that has been soaring of late (chart 1).

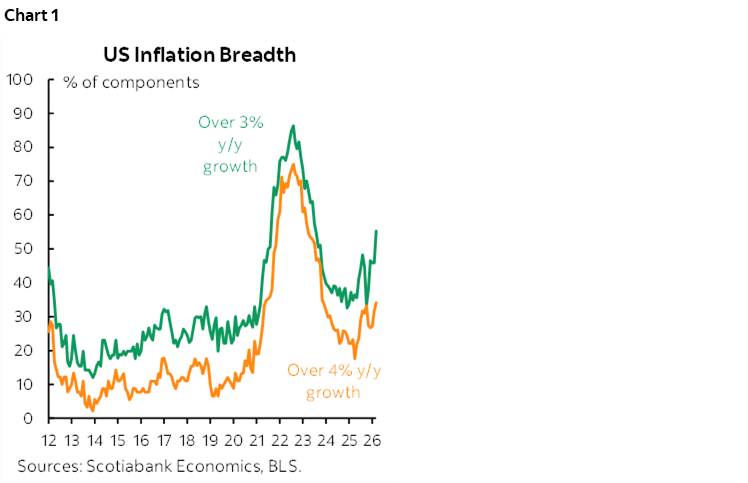

Soon afterward the Cleveland Fed will then updated its trimmed CPI measure. Recall that incoming Chair Warsh has indicated a preference for this measure which is controversial among other FOMC members. Still, it’s not surprising why Warsh’s dovish leanings would prefer the trimmed measure (chart 2).

OTHER—US ADP, US BUDGET UPDATE, AUSTRALIAN BUDGET

Other developments are relatively minor. The US also releases the weekly ADP payrolls measure after the monthly measure surprised lower than the guidance offered by the weekly estimates, implying some form of revision or recent disappointment. Treasury reports the federal budget balance for April (2pmET) which is not seasonally adjusted and usually surges into surplus in April given seasonal tax receipts.

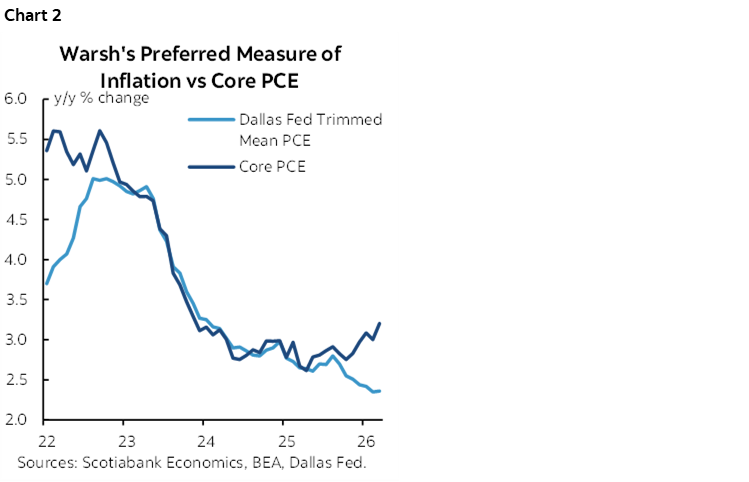

Australia’s budget barely drew any reaction in markets. The deficit was a smidge wider than expected, but at 1% of GDP it’s still lower than other roughly peer group economies and it is forecast by the government to stay around that level until decade’s end (chart 3). The Budget tightened property finance rules including higher minimum capital gains taxes and limits on negative gearing (deducting mortgage interest and other expenses on rental properties).

Mortgage interest deductibility never makes any sense but governments need to be careful about embracing policies designed to improve housing affordability by lowering prices. Expectations of capital losses can prompt a vicious cycle of falling prices that scares off prospective buyers, thereby worsening the situation. Policies designed to boost growth and incomes in sustainable, productivity-friendly ways would be wiser.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.