ON DECK FOR FRIDAY, MAY 1st

KEY POINTS:

- Markets are calm as much of the world is shut for May Day

- Japanese core inflation ebbed

- Will US ISM-mfrg be buoyed by AI spending?

- Peru’s last inflation report won’t affect the pre-election BCRP decision

- US vehicle sales probably dipped last month

- Canada may refresh auto sales today as well

- BoC’s Macklem finally acknowledges small spending impact on inflation

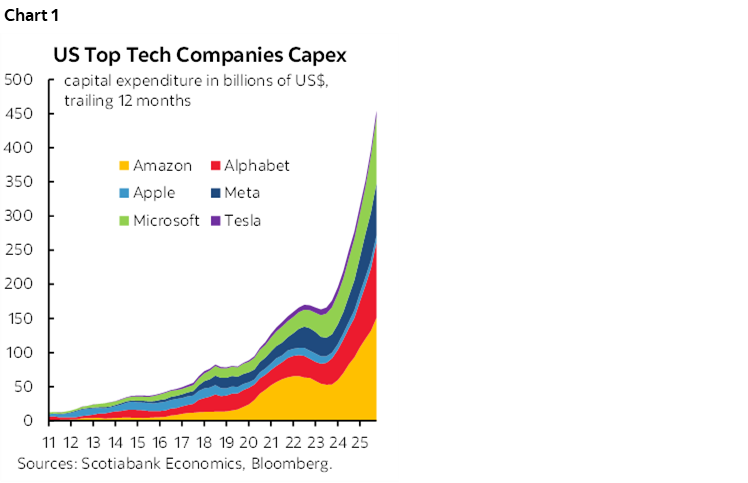

A jam-packed week is closing out with little by way of fresh developments as many of the world’s markets are shut for May Day aka Labour Day outside of N.A. Apple’s earnings release last evening is modestly supportive of risk appetite that is otherwise dealing with slightly higher oil prices again and month-end rebalancing transitions across portfolios as stocks outperformed sovereign bonds in April. Apple’s cap-ex plans were reined in a touch compared to the prior quarter but chart 1 continues to show explosive growth in ‘mag7’ spending. Elsewhere, parents may have rejoiced more than investors did as Roblox’s tumbling users in the aftermath of changed security measures tanked the stock.

Japanese Core Inflation Tumbles

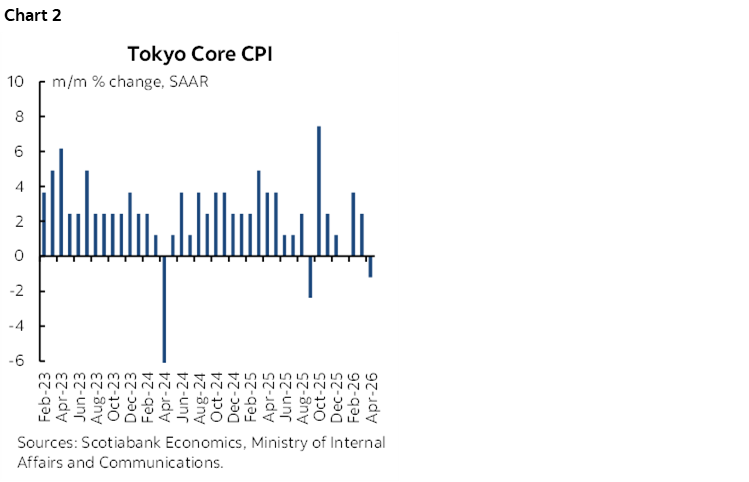

Japanese core inflation ebbed last month. The fresh Tokyo core CPI (ex-food and energy) reading fell by 1.2% m/m SAAR in April. That was the weakest reading since September (chart 2). The yen temporarily softened post-release until other global forces took over to strengthen it again which adds to sentiment that intervention moves like the previous day’s are fleeting.

US, Canada to Updates Manufacturing Indices, Vehicle Sales

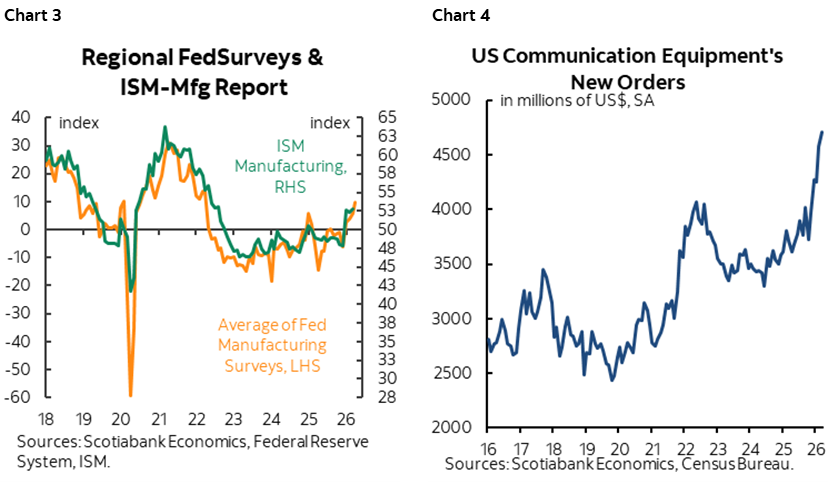

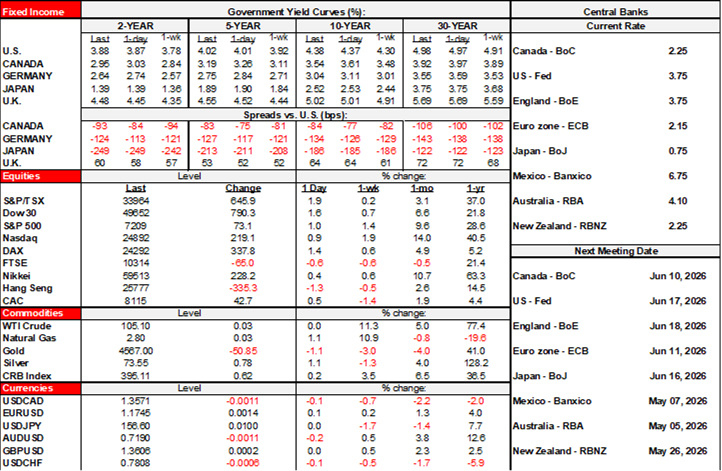

The US and Canada update some PMIs this morning starting with Canada’s little watched manufacturing PMI for April (9:30amET). US ISM-manufacturing in April (10amET) is expected to be little changed from March. The regional manufacturing gauges provided by Fed District banks were somewhat mixed but generally sound as rough guides (chart 3). Surging cap-ex orders that are driven by AI-related demand for telecom equipment could be distorting (chart 4), so keep an eye on the accompanying remarks for breadth signals.

The US will also update vehicle sales during April but after markets shut when no one is paying attention. A modest decline is widely expected. Canada might also update auto sales today or early next week following a pull back over the past two months from elevated sales in January.

BoC’s Macklem Finally Acknowledges Ottawa’s Spending Increase

BoC Governor Macklem remarked yesterday that Ottawa’s spendapalooza in Tuesday ‘s Spring economic statement will have little impact on the bank’s views on inflation. Of course it will be little relative to other forces, but quantify little, after not even mentioning it on Wednesday given the added spending would be about ½% of NGDP this year and about ¼% next year. Sequential, additive shocks to growth and inflation risk mean all of them need to be considered in holistic fashion which the BoC will be under pressure to do more thoroughly in the July MPR. Macklem did not mention surging non-energy commodities in his interview yesterday which remains unusual. Markets continue to price over a half percentage point of tightening this year.

Peru to Refresh Meaningless CPI

Peru will refresh CPI for April (11amET). It’s the last reading before BCRP’s rate decision on May 14th that may extend a hold in place since September and ahead of the run-off Presidential vote on June 7th which will probably keep the central bank out of the fray. It’s a classic left-versus-right fight with right-of-centre candidate Fujimori in a polling toss-up with leftist candidate Sanchez. Neither side should much worry, I suppose, given the longstanding pattern that shows there will be another election shortly thereafter!

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.