ON DECK FOR TUESDAY, MARCH 3RD

KEY POINTS:

- Middle East energy production disruptions drive energy prices higher…

- ...hitting Europe the hardest, given dependency on imports

- Fed, BoC forecast revisions depend critically on the longevity of the energy shock

- RBA’s Bullock puts March hike on the table, Aussie bond yields soar

- Stale Eurozone CPI took a backseat…

- …to soaring European energy prices in driving EGB yields higher

- Canada, US to update vehicle sales

- Fed-speak may react to Iran developments today

It’s all about Iran and all things related to Iran. Trump warned yesterday that “the big one is coming soon” in reference to the potential for escalated attacks on Iran as energy infrastructure is taking hits across the Middle East and adding to energy price spikes. Vague guidance pointed to this happening in a roughly 24 hour window which is keeping markets on edge toward what may transpire.

Overnight we also had hawkish talk from the RBA that drove Australian bond yields skyward. European energy prices are soaring as major production facilities for oil and natural gas are being impacted across the Middle East and that is driving EGB yields much higher while paying little heed to Eurozone CPI that surprised higher only in relation to a stale consensus. There will also be some Fed-talk—Williams 9:55amET, Kashkari 11:45amET—and light data out of the US and Canada with both countries releasing vehicle sales figures for February toward the end of the day.

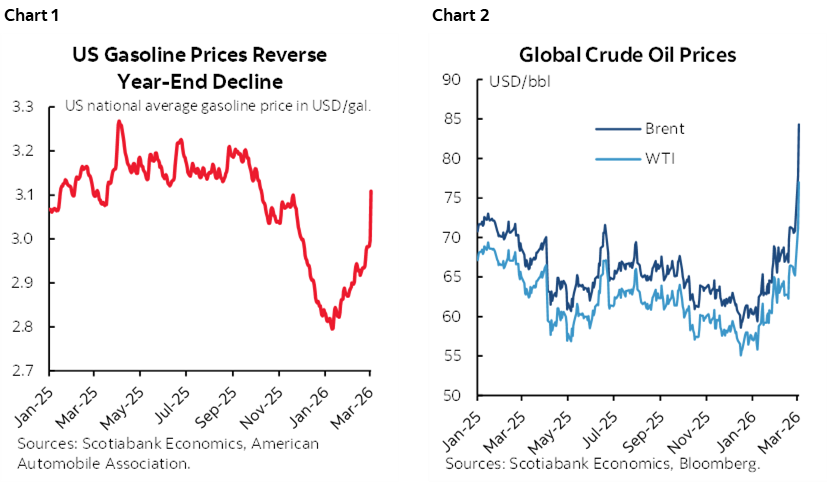

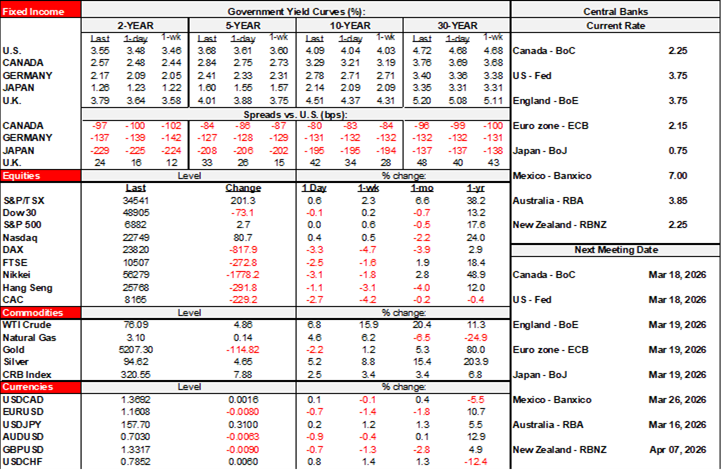

US Treasury yields are up by about 7bps in 2s and a little less at the longer-end. OIS markets have reduced full-year Fed cut pricing to about 40bps or so, having removed almost a quarter point cut since Friday. The duration of the conflict and hence the permanent or temporary nature of an energy price spike is directly tied to how far markets should go in repricing the Fed outlook over the longer term. Emotions can’t take over central bank calls. So far, US gasoline prices have reversed the year-end decline and are ‘only’ back to where they were in the fall (chart 1). As crude prices spike (chart 2) there could be more of a lift to gasoline prices given customary estimates that about half of the rise in crude flows through to gasoline prices with a lag. Key would be any persistence of this shock into the summer driving season which brings us right back to your guess versus mine versus anyone else’s about how long this lasts.

Bank of Canada pricing has shifted toward half of a quarter-point hike being priced by December. The BoC usually reacts hawkishly to a sustained rise in energy prices given the terms of trade pass through to domestic incomes and related spending. Canada 2s are up about 9bps with similar moves across much of the curve. Here too, what the BoC does is going to be critically dependent upon the longevity of the energy price spike.

Stocks are broadly lower with N.A. futures down by around 1½% – 2% across the benchmarks. European cash markets are down by roughly 2½% – 4% across major indices. This follows declines in overnight Asian equity markets of about 3% in Tokyo and as much as 7% in Seoul.

Oil prices are up by another 7% with Brent at about US$83 and WTI at about US$76.

Gold is down US$113/oz to $5,205.

Dollar debasement? Yeah, not. The dollar is capturing the safe haven flows and is up against every major cross once more with CAD in second place outperforming most others.

RBA’S BULLOCK WARNS OF BACK-TO-BACK HIKE RISK

Australia’s bond curve lit up after comments by RBA Governor Bullock. She said “I’m not making a prediction about March, but it will be a live meeting.” ‘Live’ is a term used to describe an open possibility of a policy move that in that in this case would be a hike after the RBA hiked in January. Bullock went on to say:

“We have inflation at 3.8% headline, and we have unemployment at 4.1. The board will be actively looking at whether or not it needs to move more quickly. So I would discourage people from thinking that we necessarily only meet every quarter.”

As a result, Australia’s bond yields jumped by 11bps in 2s as the curve bear flattened.

ENERGY PRICES MATTERED MORE THAN EUROZONE CPI TO EGBS

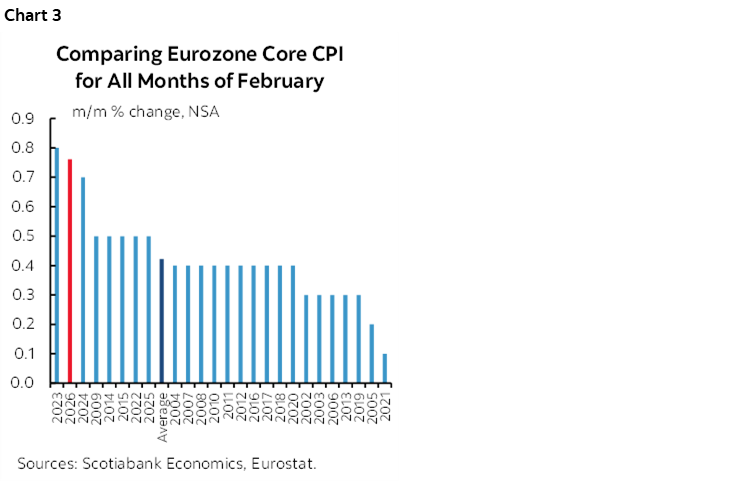

Eurozone CPI surprised a touch higher than expected within a stale consensus. February’s reading was 0.7% m/m NSA (0.5% consensus) which boosted the y/y rate up to 1.9% relative to 1.7% prior and consensus. Core CPI was up 2.4% y/y (2.2% prior and consensus) as the month-over-month seasonally unadjusted reading was among the hottest on record compared to like months of February over time (chart 3). European government bond yields were already on an upswing before the data that was probably a surprise because consensus was stale. We’ve had CPI from several major Eurozone countries since Friday and yet most of Bloomberg’s consensus was dated before then.

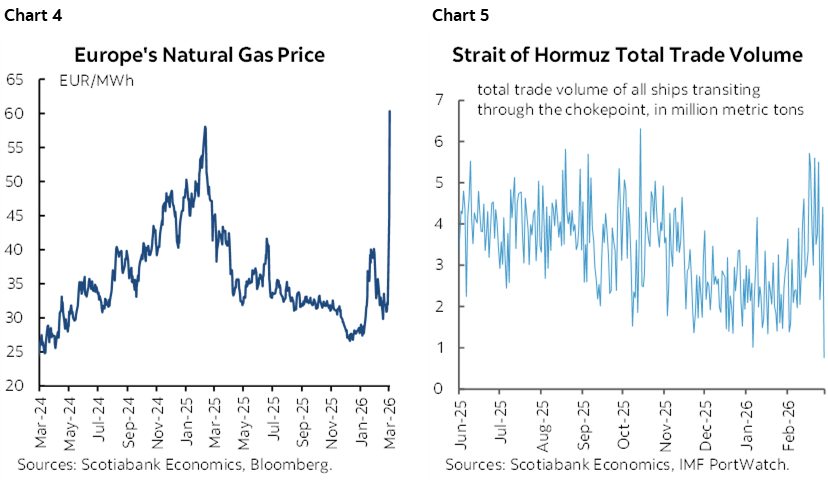

What mattered more was forward-looking inflation risk. European natural gas prices are soaring (chart 4) as inventories are low in seasonally normal fashion. Europe imports about 90% of its natural gas via pipelines and natural gas with the main sources being Norway, the US Algeria and Russia. Europe also imports about 95% of its oil. Middle East production is being significantly impeded as evidenced by a fire at the UAE’s Fujairah oil hub, and suspended output at a large oil refinery in Saudi Arabia and Qatar’s LNG plant. The Strait is now basically shut (chart 5).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.