ON DECK FOR FRIDAY, MARCH 27th

KEY POINTS:

- Markets are rightly sceptical toward Trump’s deadline extension

- Trump’s Iranian deadline extension is repeating last year’s trick…

- ...which should have markets on edge in the nearer term

- Spanish inflation accelerates in a first glimpse of the war’s effects

- UK retailers were tracking a great quarter before war broke out

“We’ve won this war.” [Pssst…ummm, Pete…send 10,000 more troops.]

This kind of conflicting guidance from the Trump administration combined with ongoing bilateral strikes and learned scepticism toward fake deadlines have markets in disbelief toward Trump’s 10-day extension of the deadline for negotiations with Iran that was supposed to have expired tonight.

And rightfully so. This piece reminds us that two-week extensions are a favourite tactic of Trump’s across many issues but that he usually violates his own deadlines and in both directions.

For instance, when the US extended the deadline last summer before Operation Midnight Hammer, it bombed Iran almost immediately after issuing the extension. Trump said this on Thursday June 19th 2025:

“Based on the fact that there’s a substantial chance of negotiations that may or may not take place with Iran in the near future, I will make my decision whether or not to go within the next two weeks.”

And then Operation Midnight Hammer bombed Iran two days later over June 21st –22nd.

Is the exact same tactic being employed once more? If so, then be on guard for nearer term actions and possibly into this weekend or early next week. It seems that Mr. Trump is totally fabricating claims that Iran is interested in negotiating. If Iran’s regime learns from Trump’s deadlines, then they won’t be letting their guard down on this one. It’s called game theory and in multi-period games you learn from your opponent’s favourite tricks especially if they unimaginatively fail to mix up their tactics. Perhaps set aside the social media account and play a little chess every now and then...

And so markets are on edge this morning and should position accordingly into the weekend. Oil is up by 2½% with Brent back above US$110/oz. Tell that to Ontario that used mid-January macro forecasts including oil price assumptions of US$59 this year and $62 next year; fresher numbers would have no doubt meant bigger deficits. Even the ECB and Fed made an effort to use fresher forecasts!

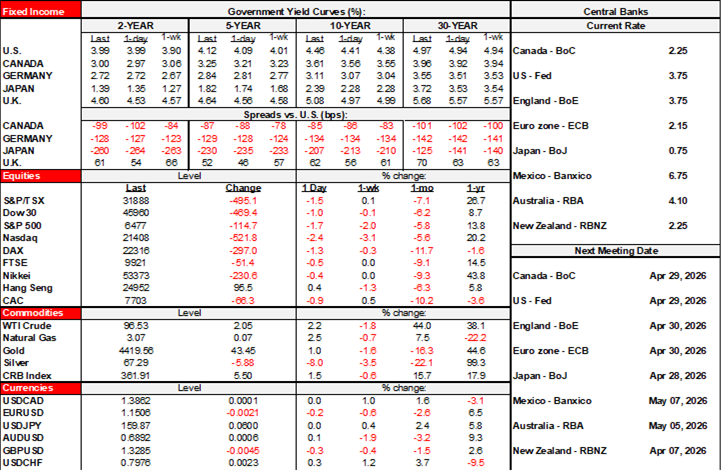

Sovereign bond yields are up across maturities and countries by single digit basis points except for a little more at the long-ends in the UK and Japan.

Stocks are pushing lower again with N.A. futures down ½% and European cash markets down by over 1%.

Across currencies, the Mexican peso is underperforming the most after a surprisingly dovish Banxico yesterday afternoon that merely positioned the energy shock as a risk.

STUFF OTHER THAN IRAN

There was a light line-up of calendar-based risks overnight. There is nothing material on tap in either the US or Canada.

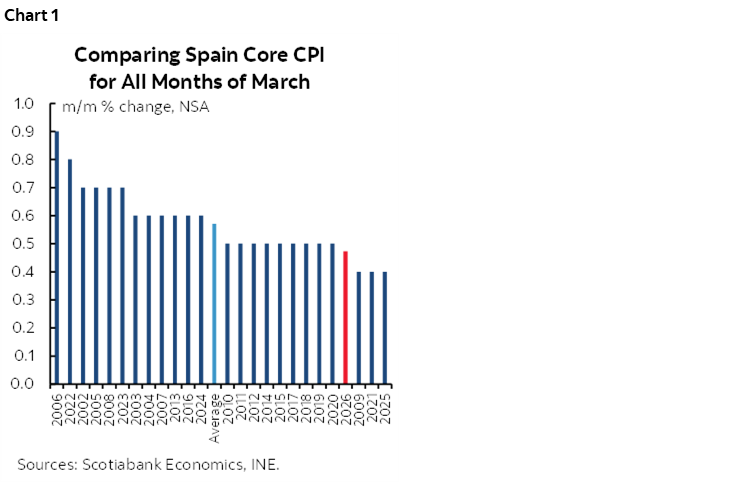

Spain’s CPI inflation surged in March by 1.5% m/m on an EU-harmonized basis. Core CPI was up by just under ½% m/m which was among the weaker readings comparing like months of March which is the comparator because it’s not seasonally adjusted (chart 1).

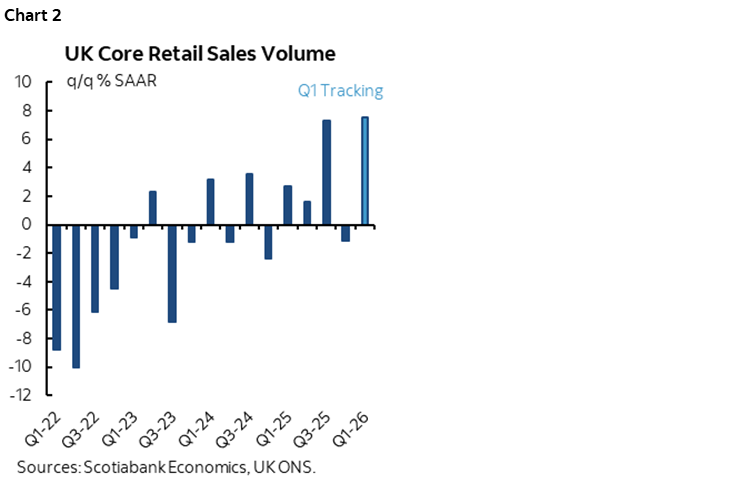

UK retail sales volumes gave back a little of the prior month’s surge. February sales volumes slipped by -0.4% m/m after an upwardly revised 2% m/m surge in January. Sales ex-gas also fell by -0.4% and after an upwardly revised prior gain of 2.2%. Markets faded the backward-looking data. Nevertheless, the overall quarter is on fire with sales volumes ex-fuel tracing a surge of 7½% q/q SAAR (chart 2).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.