ON DECK FOR THURSDAY, MARCH 26th

KEY POINTS:

- Oil up, everything else down as Iran negotiations stall

- Iran’s five demands basically rejected negotiations…

- …calling Trump’s bluff as the weekend deadline approaches…

- ...prompting Trump to escalate his warnings this morning

- Norges Bank pivots toward hiking

- What the BoC could say in today’s talk on the economy and policy

- SARB expected to hold

- Banxico faces a divided consensus

- Ontario’s budget arrives after the close

- Light data: Canada’s lagging and volatile payrolls, US claims

Oil’s gyrations continue this morning after Iran’s wildly unrealistic counter demands amount to thumbing the country’s nose at Trump (see below). The US claims that negotiations continue but there are no transparent signs of this on Iran’s behalf as the Revolutionary Guard appears to be more broadly in charge of Iran. In fact, Trump’s social media post this morning (here) makes it sound like he’s stunned that his bluff is being called and upping his threats, but to say Iran is “begging” for a deal seems contrasted by all of the other evidence. Trump also ranted against NATO again; recall my ten pointer on why allies are not rushing in to help here.

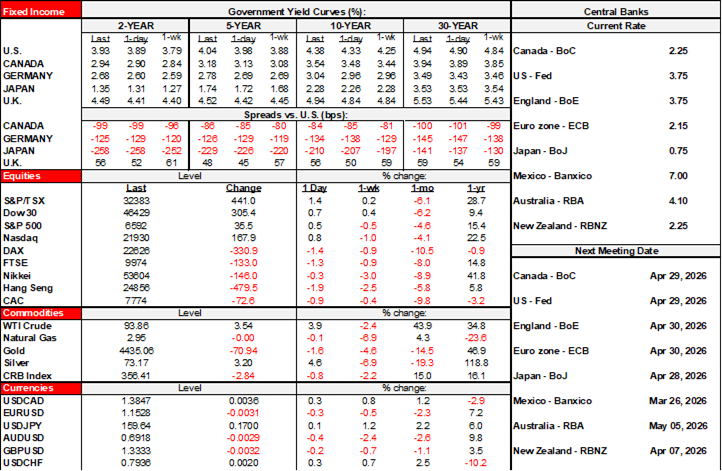

And so Brent and WTI are both up by around 4%. With knock-on effects on inflation concerns go less demand for gold that’s off by about $60/oz.

Sovereign bond yields are rising everywhere by single digit basis points across US Treasuries, Canadian govies, gilts, EGBs, JGBs, Aussie bonds etc. A contributing catalyst is more evidence that central banks are in tightening mode (see below).

With higher yields go lower equities everywhere with N.A. futures down by about ¾% to 1% and European cash selling off by either side of 1% after a weak Asian overnight session.

IRAN’S DEMANDS — FAT CHANCE

Iran’s counter-demands to the US set their conditions for a ceasefire and are nonstarters.

- A complete cessation of the adversary’s “aggression and assassination” operations.

- Establishment of concrete mechanisms to ensure the war is never again imposed upon Iran.

- Guarantees and clearly defined procedures for payment of compensation and reconstruction costs resulting from the war.

- Cessation of hostilities across all fronts and across all resistance groups involved throughout the region.

- International recognition and guarantee of Iran’s sovereign right to exercise jurisdiction over the Strait of Hormuz.

As conditions for a ceasefire, they say “No negotiations will take place before this,” and reiterated that Iran’s “defensive actions” will continue until all the above conditions are fulfilled.

Fat. Chance. Imagine a US taxpayer funded version of a Marshall Plan to rebuild Iran that flows straight into the pockets of what’s left of the regime and the Revolutionary Guard. A guarantee not to attack in future would be worthless anyway; ask Ukraine about long-term guarantees with 1994 in mind. Stopping “hostilities across all fronts” and “all resistance groups” presumably includes Iran’s proxy groups like Hezbollah which is going nowhere. And having over control of the Strait of Hormuz is never going to happen.

The US administration just doesn’t get it. Iran is not a democracy. Iran does not face any election timeline like the US does. Iran is not an openly capitalist economy. Iran is used to hardship. Iran has fought many vicious wars and experienced enormous suffering. Iran’s geography makes escalating a conflict a high risk venture. Iran has friends in low places with similar characteristics. Iran’s vicious tentacles reach across the world. Iran’s regime hates the west and everything it stands for. This is why you don’t fire off all the folks in your state department. This is why maybe you don’t increase your country’s dependency on fossil fuels in a US replay of Germany’s past decision to shun nuclear reactors in favour of imported Russian gas.

BOC TO ELABORATE UPON VIEWS ON THE ECONOMY AND MONETARY POLICY

The BoC’s Rogers speaks on ‘economic developments, monetary policy and affordability’ in Manitoba. Speech headlines hit the privileged media outlets that get embargoed copies to pre-write their stories at 1:10pmET. There will be moderated Q&A after she speaks, but no press conference which is a bit unusual.

I’d be surprised if she said anything materially different from what Macklem said last week, though the heat is on the BoC to say more about how it views the broad commodity shock and what to do about it.

The most important part of last week’s BoC communications (recap here) in a why’d-you-do-it sense was striking out the final paragraph’s reference to the policy rate being “appropriate.” They do things like that very deliberately. They’re not going to be cutting into a broad commodity shock. They could have gotten away with leaving it in now and saying we’ll see. But they struck it out. Why. To give policy flexibility to hike if needed?

The second most important thing about last week’s communications was the line that said "Governing Council will look through the war's immediate impact on inflation but if energy prices stay high, we will not let their effects broaden and become persistent inflation.” Look through has its limits is the clear signal in a warning that depending upon the course of developments they are warning of policy tightening.

That is a major change for the BoC. Recall that Macklem spent ages totally ignoring inflation’s ascent in the pandemic versus taking out insurance hikes like the Bank of Korea did in 2021. The BoC had to violently catch up by hiking in dramatic fashion from 0.25% to 5%. I’m encouraged that this time they are signalling earlier awareness of the inflation risk than previously after learning that perhaps there is merit to insurance hikes and stagging your policy options earlier to avoid more calamity later.

It’s also a marked change from the slowness of the BoC’s to respond in some past oil shocks. Consider 2014–15 for example when the opposite situation of tumbling oil prices occurred. Oil was in freefall from over US$100 on WTI in mid-2014 to under half that by year-end into early 2015. Do a keyword search of statements over that period and they never even mentioned oil or energy. Then Poloz suddenly cut in January 2015 and pinned the cut on lower oil.

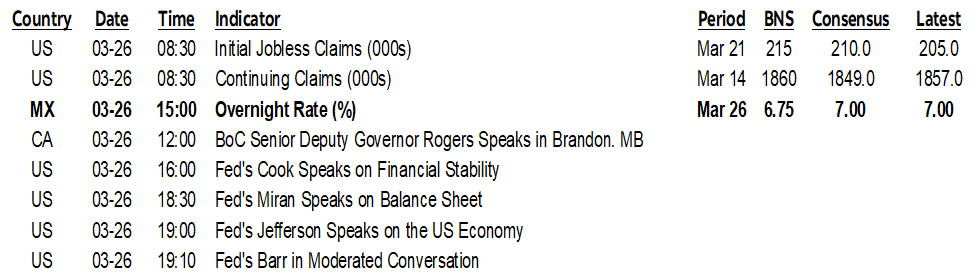

We may hear continued reference to how slack gives the BoC some time to assess what to do. That may be true, if you trust estimates of the level of potential GDP and potential GDP growth. It may be true if you believe we’re in a sustained soft patch on core inflation despite industrial prices chomping at the bit to pass through to core CPI (chart 1). It may be true if commodity markets suddenly collapse and all the bad people in the world go away. But I wouldn’t bank on all of that. We’ve upped our inflation forecast toward 3¼% y/y by year-end which implies the real policy rate has now plunged toward –100bps; if that stays, the BoC has passively eased into a broadly positive commodities shock which makes no sense.

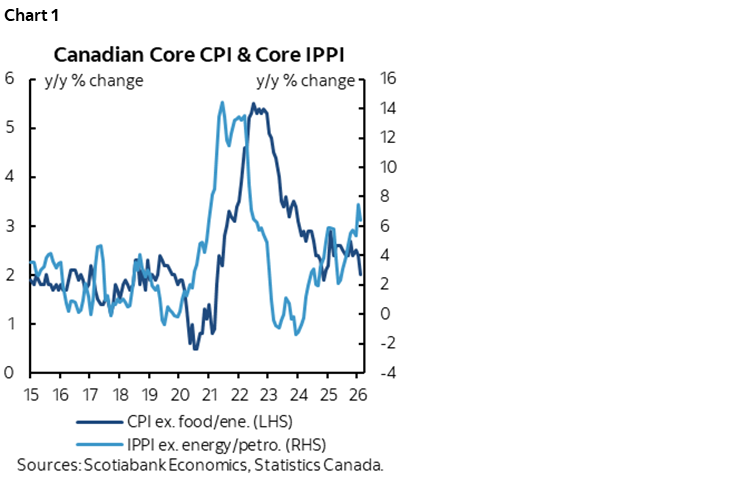

And on risks to the job market, don’t neglect the supply side. Canada’s population is shrinking because of tighter immigration policy and the Labour Force Survey will catch up to that in lagging fashion because of the quirky way in which it counts the nonpermanent resident component (chart 2). When LFS population catches up to what the folks in Statcan’s population division are telling us it will shrink the supply side and tighten the labour market.

NORGES IN HIKE MODE

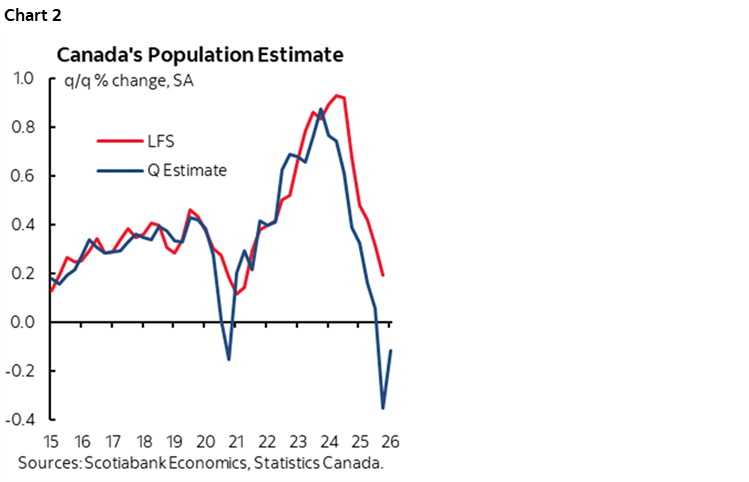

Norway’s central bank pivoted toward a tightening bias in its policy communications this morning. They left the deposit rate unchanged at 4% as universally expected but said “it will likely be necessary to raise the policy rate at one of the forthcoming monetary policy meetings.” That’s significant to other central banks in commodity dependent countries —in Norway’s case especially oil.

This is one of the central banks that provides explicit forward rate guidance and their updated rate projection shows mild hikes of 25–50bps this year before slipping back down thereafter on the expectation the inflation will return to cooling thereafter (chart 3). Obviously everyone’s longer-term views are highly uncertain, so emphasize the nearer-term guidance.

That’s what markets did in pushing the odds of a hike at the next meeting on May 7th to over 60% while pricing a 25bps hike and almost half of another at the June 18th meeting.

SARB EXPECTED TO HOLD

South Africa’s central bank is expected to stay on hold at a repo rate of 6.75% today (9amET). It has been cutting the policy rate since September 2024 and now faces market pressure to pivot toward tightening policy.

At 3% y/y, headline inflation’s continued descent into February might be construed as providing room for policy easing. That’s unlikely as backward data is put on the backburner in the face of forward-looking risks.

South Africa is dependent upon energy imports (here). The rand has been among the worst currency performers in the world, having lost about 5% of its value to the dollar since late January. The combination of higher oil prices and a falling currency adds to imported inflation risk.

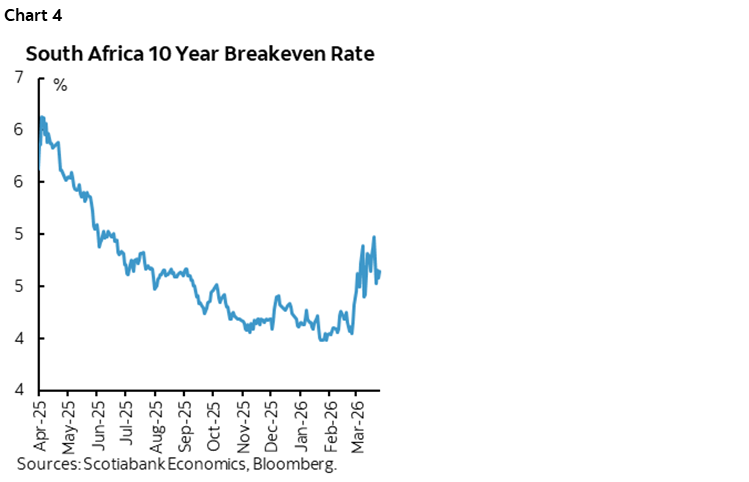

That hasn’t exactly gone unnoticed by markets. Longer term inflation expectations have been rising sharply (chart 4). SARB is sure to take note, putting in place either the risk of a hike and/or hawkish forward guidance.

BANXICO FACES A DIVIDED CONSENSUS

What Mexico’s central bank elects to do this afternoon (2pmET) is a close call with roughly half of consensus holding and half (including our team in Mexico City) expecting a cut. Watch the bias which may be more important.

When Mexico’s central bank last weighed in on February 6th, they paused the easing cycle because Governing Council was concerned about ongoing inflation risk. The easing campaign before that meeting was dividing members who pivoted toward full agreement to halt cuts.

You might think they would be hesitant to restart it now. Hawks like Deputy Governor Heath—who was previously warning and dissenting against easing—have already weighed in. He said about a week ago that “I think we should have paused in March, and now, taking into account a more complex scenario due to the armed conflict in the Middle East, even more so.”

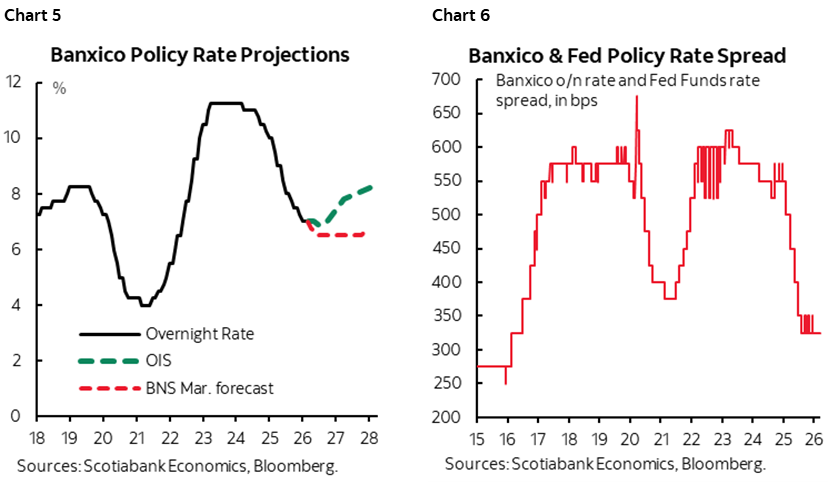

The further unmooring of market-based measures of inflation expectations is bound to be of concern to Banxico and to markets that are pricing the next moves to be upward as soon as later in the year relative to our Mexico team’s projection (chart 5). So are the limits of acting independently of the Fed when the policy rate spread is toward recent lows (chart 6).

LOW DATA RISK

Data risk is very low. Canada releases the severely lagging SEPH payrolls report for January (8:30amET). It’s revised so heavily each and every month (unlike annual LFS revisions) that it can’t be taken seriously on top of only be a payrolls measure and hence missing a lot of important small businesses.

The US only refreshes weekly jobless claims (8:30amET).

ONTARIO BUDGET

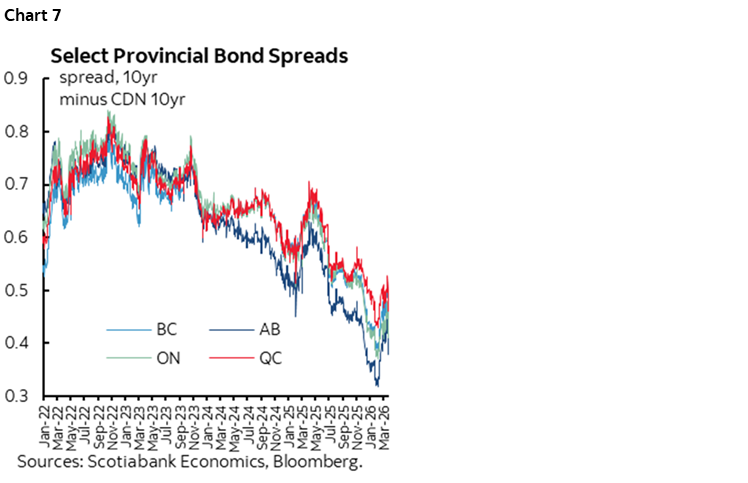

Ontario will release its 2026–27 (FY27) budget at around 4pm ET. Provincial bonds are barely noticing budget season (chart 7) as they’re driven more by other factors like proxies for broader risk appetite and relatively safe yield pick-up over Canadian government bonds. What follows are comments by Mitch Villeneuve.

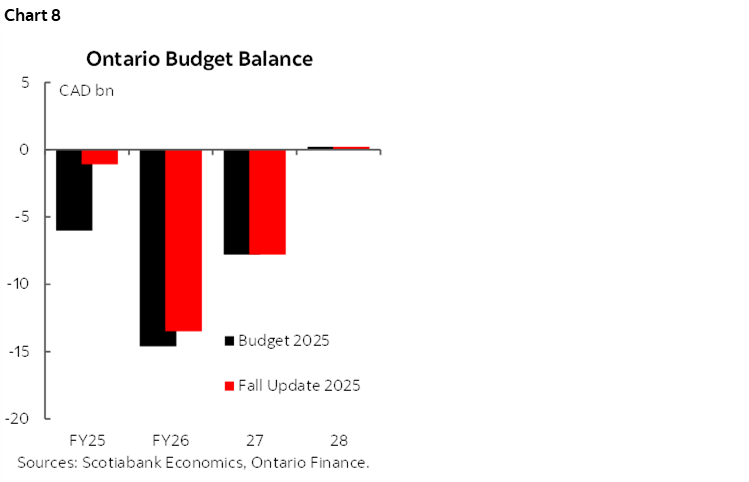

Its recent fiscal plans have set out a return to balance in FY28, and the province has been one of the few that has decreased its deficit projection for this year as the year as gone on—reflecting considerable prudence in the fiscal framework as well as spending discipline (chart 8). We expect the updated deficit number for FY26 to come in lower again, given the nearly $5 billion in contingency buffer and forecast reserve remaining as of the Q3 fiscal update—though the largest revision is likely to come in the fall when the FY26 Public Accounts are finalized. The deficit number for future years could come in lower as well, depending on the new economic assumptions and cost of new measures. The finance minister has signalled that the budget will have several priorities, including: productivity and innovation; a competitive business environment; infrastructure and housing; trade; talent and workforce; and reliable, affordable, clean energy. The government has already announced that the budget will temporarily (for FY27) remove the HST from all new home purchases (building on the existing incentive for first-time home buyers), in collaboration with the federal government.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.