ON DECK FOR WEDNESDAY, MARCH 25th

KEY POINTS:

- Markets play the waiting game

- It’s unclear who or what to believe about US-Iran talks…

- …but most signs hardly indicate agreement is near at hand

- UK core inflation slightly firmer than expected

- Aussie inflation was slightly weaker than expected

- Danish vote falls short of giving lefties a clear mandate

- US: Fed-speak, import prices

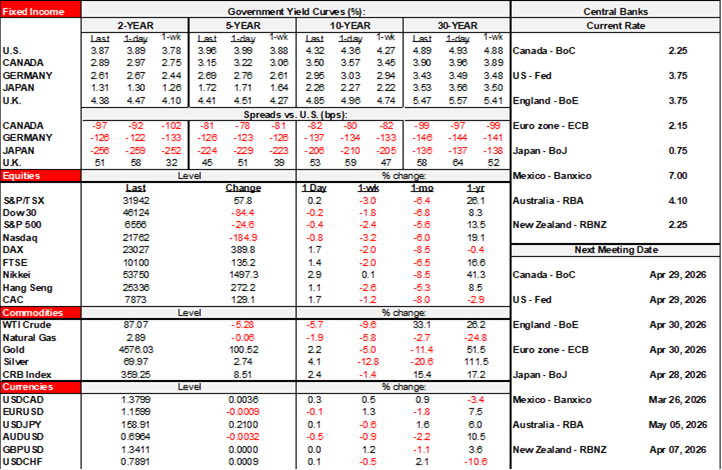

Markets are erring on the side of mild optimism that the US and Iran will be able to strike some sort of agreement that deescalates the war. That’s highly unclear amid signals to the contrary. Nevertheless, oil prices are down by about $5–6/barrel with WTI below $90 and Brent below $100. Gold is getting a bounce for a change with about a 2% gain. Sovereign yields are broadly lower with declines of 4–12bps across maturities and regions. Stocks are broadly higher in the 1%+ range across N.A. futures and European cash markets. The dollar is a touch softer against most crosses as higher-beta crosses gain.

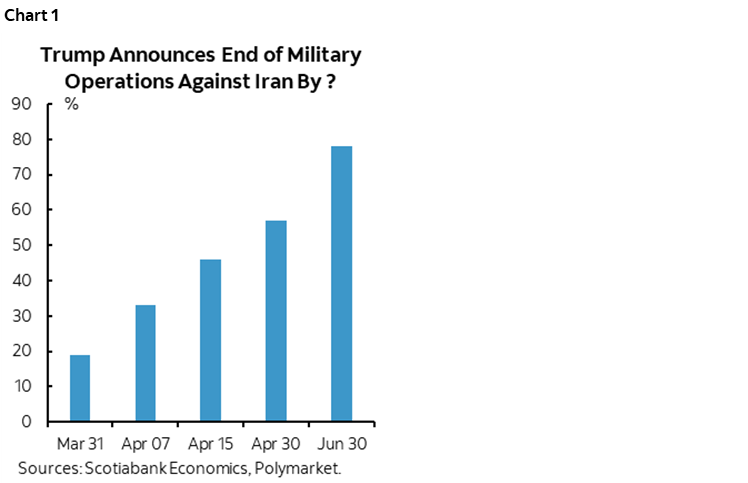

Who are we to believe when both the US administration and Iran are merchants of disinformation? The wisdom of crowds—an oxymoron if I’ve ever heard one—is scattering its bets all over the map on when a ceasefire may be announced, when US forces may enter Iran, when military operations may end (chart 1), when Iran may attack someone else, etc (here). Maybe there will be clarity on the platform’s odds when someone in the administration’s orbit places their bets.

The signs from Iran are hardly indicative of accepting the agreement that Trump’s extended family members have purportedly negotiated with an unknown Iranian leader with unclear power to sell and enforce any agreement. Iran continued to attack neighbours overnight. The head of its military and Revolutionary Guard—at least until the Israelis pop him off—said overnight that “someone like us will never come to terms with someone like you.” US marines continue in transit to the region with more orders given yesterday. Israel wants nothing to do with negotiations and was reportedly surprised by the US gestures while pursuing its own aims. Can the US control Israel and would Iran settle with the US while the Israelis keep attacking?

As far as I’m concerned, Iran holds all the cards in a midterm election year as the GOP is looking set to be utterly destroyed on November 7th. Maybe get a CUSMA/USMCA 2.0 deal through Congress before January, just sayin’. Ditto for the always mischievous Russians as they dramatically escalate Spring attacks on Ukraine while rather enjoying seeing the US President practically on his knees begging for Iran to stop the war he started. So we wait. And wait. For someone to blink. For missiles and drones to stop being flung. For concrete signs of deescalation.

Meanwhile in the Department of All Things Irrelevant—which is experiencing a hiring boom by the way—we have a pair of stale inflation readings from the UK and Australia.

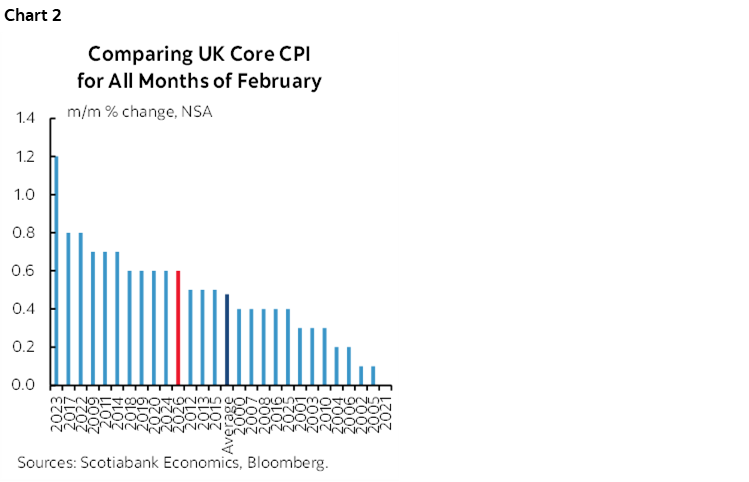

- UK CPI in pre-war February landed at 0.4% m/m seasonally unadjusted (ie: NSA), matching consensus expectations and up 3% y/y. Core inflation ex-food and energy was up 3.2% y/y (3.1% prior and consensus). The NSA core CPI reading in m/m terms was ever so slightly warmer than an average February which is the comparator when using seasonally unadjusted readings (chart 2). Services inflation continued to ebb but was not light (chart 3). And next up is the war’s effects in March CPI onward combined with Ofgem’s price changes.

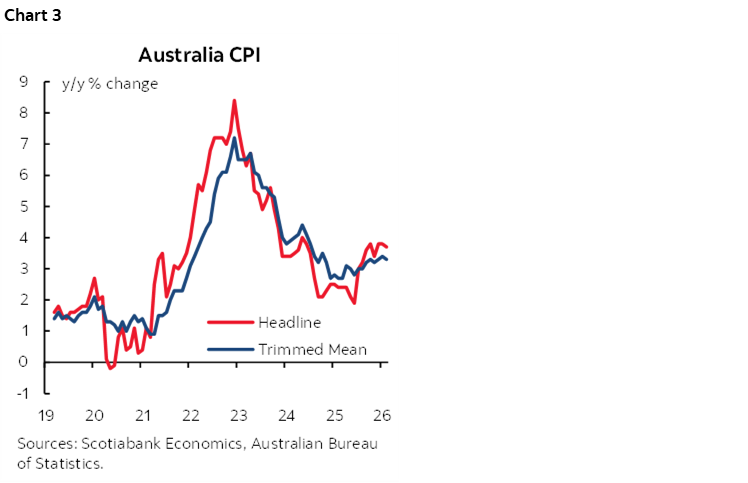

- Australian CPI was a smidge softer than expected. Prices were flat in m/m NSA terms in February and up 3.7% y/y for a tick beneath consensus. Trimmed mean core CPI which removes outlier price changes in both tails to focus on central tendency price pressures was up 3.3% y/y (3.4% consensus). It’s hard to tell whether the A$ and Australian rates cared amid other developments. Chart 3.

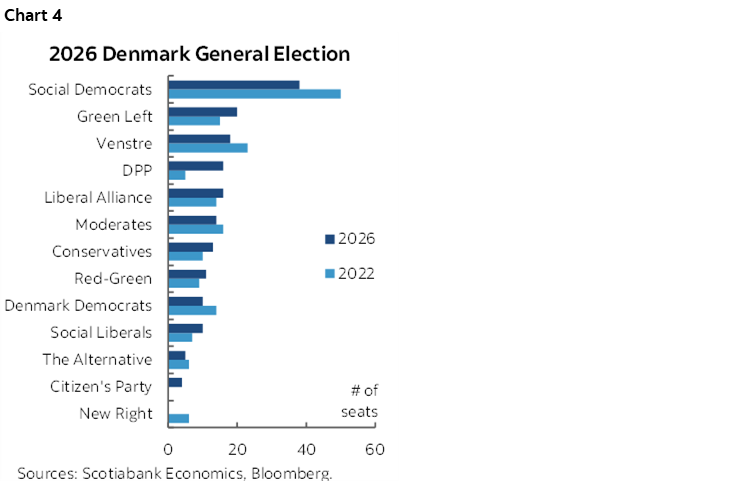

Danes voted to give PM Mette Frederiksen the largest single share of the vote but not enough for her left-wing faction to form a government while underperforming her previous election results (chart 4). Trump made her Great Again over Greenland compared to her muddling and uninspiring performance beforehand, but not great enough.

The N.A. calendar is very light today. Fed Governor Miran speaks after the close and was the lone dissenter in favour of easing last week. Import prices during February (8:30amET) will be cast aside until we get meaningful data over coming months.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.