ON DECK FOR TUESDAY, MARCH 24th

KEY POINTS:

- Global markets restore some calm after yesterday’s violent moves

- Understanding Trump’s about face is key to understanding the path forward

- Global PMIs signal broadly weaker growth, higher inflation

- A pair of curious BoC departures

- Why Canada’s unemployment rate is more likely to fall than rise

- Danes vote today

- Other light data

After yesterday’s violent moves across asset classes, today is positively dull by comparison. Oil is up by about 2% with Brent at about US$102 and WTI at just over $90. Equities are little changed with a slight negative bias across N.A. futures and European cash markets after Asian equities spent the overnight session merely catching up to the Trump-fed rally in western markets. Sovereign bond yields are little changed but with a slightly higher bias across the US and core Eurozone front-ends versus slightly lower UK yields after Asia-Pacific benchmarks rallied in lagging fashion to the west. Canada’s rates curve is little changed. Currencies are mixed but with little change overall as outlier moves are limited to the Antipodeans, rand and won.

Today’s markets may tread water barring any sudden surprises as they wait for Trump’s coming weekend deadline for talks with Iran to arrive. We’re left interpreting PMIs, curious moves at the BoC and debating how gullible and easily manipulated markets proved to be once again yesterday.

UNDERSTANDING TRUMP’S ABOUT FACE IS KEY TO UNDERSTANDING THE PATH FORWARD

My, aren’t markets gullible and they quite possibly never learn from the manipulative tactics. Why did Trump delay attacks on Iran and stand down yesterday? Here are a few theories and they’re not necessarily mutually exclusive. On net, I think they point toward a high degree of continued caution toward the very real prospect that the war intensifies and that markets overreacted in no small part due to violent market positioning swings that exaggerated the responses.

- to wait until the marines are in place by this coming weekend. Just like when Trump threatened Iran and backed down temporarily upon realization that US warships and planes were still a long way from being in place.

- Iran counter-threatened with its own escalation and Trump backed down for now.

- Trump is finally realizing the soaring cost of the war, the low probability of achieving the initial aims, and the political consequences and is therefore looking for an exit. You could interpret his comments about Hegseth as an attempt to make it sound like it’s all his fault that the US got into this mess.

- someone in his orbit wanted to float a trade and made a lot of money (here and here). Multiple accounts have noted that trading volumes spiked unusually in the immediate lead up to Trump’s social media post. Competent and distanced regulators would normally investigate.

- to push out the strikes until next weekend after markets shut rather than the start of the week’s trading.

- to lower the enemy’s guard before boots hit the ground.

- to divide Iran’s reportedly divided leadership even further in a classic Trump tactic.

- to temporarily lower oil prices so they can stock up the strategic petroleum reserve.

GLOBAL PMIS — WEAKER GROWTH, HIGHER PRICES

Global purchasing managers’ indices indicated a sharp economic slowdown across the world along with a sharp intensification of price pressures. Who’s surprised? Cricket, cricket… The readings generally reaffirm broader market sentiment and pricing that has hit growth assumptions and pushed market measures of inflation expectations higher across the world. You could argue that the fact service sector readings tumbled more than manufacturing PMIs was a bit of a surprise given the nature of the shocks. Recall that the PMIs capture sentiment across purchasing managers and hence theoretically reflect information at the level of transactional decision making within firms. They can be buffeted by volatile sentiment while 50 is the dividing line between economic expansion (above) and contraction (below). Onto the cheery details now to accompany charts 1–3.

- The UK composite PMI fell 2.7 points to 51.0 with weakness driven primarily by services (51.2, 53.9 prior) as manufacturing was little changed (51.4, 51.7 prior). Input prices in the manufacturing sector climbed by the most since October 1992 when sterling depreciated after Black Wednesday (here). Output prices also accelerated by the most since last April as respondents noted “the need to pass on higher raw material prices to customers.”

- The Eurozone composite fell by 1.4 points to 50.5 with the weaker reading driven entirely by services (50.1, 51.9 prior) as manufacturing accelerated (51.4, 50.8 prior). Both Germany and France experienced weaker composite PMIs, weaker services PMIs, but somewhat firmer manufacturing PMIs. Respondents noted the fastest rise in input price inflation in three years which takes us back to higher inflation coming out of the pandemic, and a pick-up in selling prices. Shipping delays were cited as a factor and S&P noted that the price gauges indicate “inflation accelerating close to 3%” from 1.9% y/y up to February.

- India’s composite PMI fell by 3.4 points to 56.5 which continues to signal the quickest economic growth of any of the regions. Manufacturing decelerated the most (53.8, 56.9 prior) and services decelerated by less via a 0.9 dip to 57.2. Input prices climbed by the most in nearly four years with prices for aluminum, chemicals, electronic components, energy, food, iron ore, leather, oil, rubber and steel getting nods. Output prices climbed by the most in seven months.

- Australia kicked it off in miserable fashion as their composite PMI fell by a whopping 5.4 points to 47 and hence into outright contraction territory. Services bore the brunt of the drop (46.6, 52.8 prior) as manufacturing decelerated a touch (50.1, 51.0 prior). Input and selling prices climbed by the most since 2023.

- Japan’s composite PMI fell by 1.4 points to 52.5 on both services (52.8, 53.8 prior) and manufacturing (52.5, 53.9 prior). Input costs climbed by the most since February of last year as the yen, labour costs, fuel and broader supply chain challenges were cited.

- The US releases its PMIs at 9:45amET this morning.

OTHER DEVELOPMENTS

Also keep an eye on a pair of minor US releases. The Richmond Fed’s manufacturing gauge for March (10amET) could break the tie between the deterioration in the NY Fed’s Empire manufacturing measure that fell versus the Philly Fed’s measure that slightly accelerated. KC’s measure is out in two days, and the Dallas Fed’s is due on Monday as oil country laps up higher prices.

The US weekly ADP private payrolls measure is also on tap (8:15amET). It decelerated a touch the prior week, but this update will start to push into war territory as it covers the week ending March 7th.

Chile’s central bank is universally expected to stay on hold at an overnight rate of 4.5% (5pmET). Markets are pricing a modest chance at a hike over coming meetings.

Japan’s CPI inflation pulled back to 1.3% y/y in February with core slipping to 1.6%. And no one cared since, well, it’s February.

Even better in the stale category will be Mexico’s economic activity index—a GDP proxy—that covers January (8amET).

Danes are voting in their general election today. We should get the results of exit polls after 3pmET when local polls close. PM Mette Frederiksen wasn’t inspiring many locals until Trump came along and gave her a boost.

WHY THE UNEMPLOYMENT RATE OUTLOOK IS UNLIKELY TO HINDER THE BANK OF CANADA’S POLICY DECISIONS

Would the Bank of Canada’s policy response to what is emerging to be a major positive inflation shock be hindered by fear that the unemployment rate would soar?

Obviously the first issue is that the formal target is 2% inflation over the medium-term.

Labour market conditions indirectly feed into that if correlated with a broadly weakening economy. You might argue it’s a touch less obvious than it should be because Freeland changed the wording of the five-year review in 2021 to price stability as the “primary” goal and with the statement peppered with references to fully inclusive maximum employment. That, in my view, should be left out of a monetary policy dialogue.

The second issue is going to be what do you expect to happen to the UR. Our forecast is for it to decline—yes, decline—partly on employment forecasts but mainly because of a shrinking population and labour force. The Labour Force Survey’s quirky methodology that applies lagging smoothed trends to counts of temporary residents (the category of immigration that drastically overshot) lags Statcan’s quarterly population counts such that LFS will show a downward correction in population and the labour force going forward. It’s as if one division at Statcan doesn’t talk to the other division on something as rudimentary as what’s the nation’s population count and trend! From 6.7% at the moment, we could reasonably push lower toward 6% and possibly lower.

Now, when I hear doves talking about a rise in the UR should the BoC begin hiking, the number I’m hearing is 7%. Are you kidding me? It’s 6.7% right now. Governor Macklem would hit snooze on that forecast. And again, it’s more likely to go down as argued.

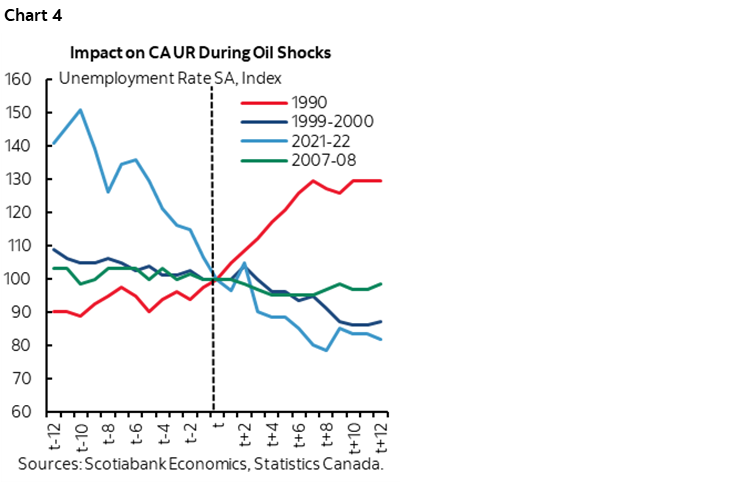

The third issue is to consider what actually happens to employment during positive oil price shocks. We can look at four episodes in the modern era (chart 4). The only time it spiked was 1990–91. I don’t think people who recall that period would say so, including me as I started my career coming off that spike. Fiscal policy was turning contractionary with ratings downgrades and widening spreads over the US. Canada was in the early days of adjusting to the Canada-US FTA and then NAFTA 1.0. Rates were already sky high going into it in the early days of adopting explicit inflation-targeting in the Crow years.

THE BOC’S CURIOUS DEPARTURES

It’s unusual for the Bank of Canada to lose two Deputy Governors on the same day (here), not to mention at a possible policy inflection point and in a 5-year review year for its mandate. Kozicki was nearing retirement age, Mendes was not and there was no mention of pursuing another opportunity.

Maybe we’ll learn more, but for now, the BoC’s Governing Council becomes rather thin in short order (April 10th for Mendes, July 15th for Kozicki). The wall of fame is left with only two permanent qualified economists on Governing Council (here). The stated intention to fill the positions (plural) with a narrowed pool of only internal candidates seems unusual as they usually cast a wider net and may indicate that either the decisions happened fast or the BoC’s budget cuts imposed by the Federal government are working their way through the rank and file. The BoC’s DepGov pay might be a factor in limiting the pool to internal candidates as well. Scroll down to the executive leadership for possible candidates among the ones with suitable training with names like Coletti, Gosselin, Murchison, Santor and Sarker theoretically among the possibilities.

What were the views of the departing DepGovs on Governing Council? Kozicki is tagged on the street as a dove, yet her speech at the start of this month didn’t sound so dovish to me. Here’s the money quote:

“When a supply shock has small or short-lived effects on inflation, central banks tend to look through the impacts as they set monetary policy. When the economy is weak, they may be able to wait for inflation to return to target on its own. But a look-through strategy has limits. Central banks generally should respond when the impacts of a shock on inflation are larger and more persistent.”

So, is today ‘small or short-lived’ or ‘larger and more persistent’? I’d lean to the latter in which case she may lean in the direction of tighter policy at the next three decisions she will work through before departing. For now, we’re sticking to hikes commencing in Q3 with openness toward Q2 pending further developments within a highly fluid situation.

Mendes, however, is gonezo before the next decision on April 29th and his views were generally more difficult to read. His last speech touched on the five-year review and indicated yet more core inflation readings may be offered—as if there are not enough already.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.