ON DECK FOR MONDAY, MARCH 23rd

KEY POINTS:

- Wild market volatility is being caused by Trump’s social media posts

- Trump escalates, then stands down

- A round-up of central bank pricing

- The BoC’s real policy rate is inappropriately plunging

- Two inexcusable behaviours

- ECB’s wage tracker points to pick-up

- Very light data US, Mexican data on tap

- Global Week Ahead — Inflation Insurance (reminder here)

Broad asset classes were selling off into a fresh trading week until moments ago. The driver of the negative sentiment was Trump’s Saturday night ultimatum to Iran to “fully” reopen the Strait of Hormuz by about 7:45pmET tonight “without threat” or the US will “obliterate their various power plants, starting with the biggest one first” which is presumably a reference to the 2,900 megawatt Damavand plant. Iran responded by threatening to indefinitely close the Strait, to attack “all energy, information technology, and desalination infrastructure” across the region as well as financial entities, and by escalating missile strikes against Israel. Markets were left pricing a game of chicken.

Then this post from Trump hit just moments ago. Trump claims that the US and Iran have had talks and deescalation is in order as he has “instructed the department of war to postpone any and all military strikes” against the targets he laid out earlier.

As a result, markets swung from double digit basis point increases in sovereign debt yields across major markets to notable rallies in the high single digit declines in basis points to double digits. Oil prices went from slightly higher to double digit percentage point declines at the time of writing. Market moves are likely being overstated on position swings.

I’ll leave you to decide whether it’s true that talks have evolved in such fashion, or whether Trump chickened out perhaps upon seeing markets or seeing Iran’s response, or whether someone benefited from the market swings etc. To say that US foreign and domestic policy are in a state of utter chaos would be an understatement as uncertainty is being driven through the roof to the detriment of the economy and markets.

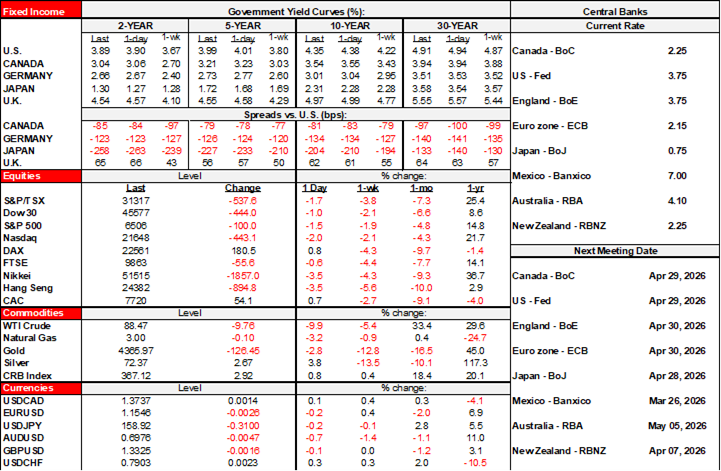

Market pricing is in turmoil at the moment here was market pricing across many central banks just before Trump’s latest post:

- Fed: OIS markets are leaning toward a mostly priced 25bps hike by year-end.

- BoC: Markets have about 100bps of hikes priced by year-end. This includes a one-in-four chance at a hike in April and a mostly priced June hike.

- ECB: A 25bps hike in April is fully priced followed by another fully priced hike in June and then a path toward nearly a cumulative 100bps of hikes by year-end.

- BoE: A 25bps hike in April is mostly priced and so is another in June on the path toward nearly 100bps of hikes by year-end.

- BoJ: Markets are on the fence between an April and June hike toward 50bps by year-end.

- RBA: 75–100bps of hikes are priced by year-end including two-thirds pricing of an April hike.

- RBNZ: Almost 100bps of hikes are priced by year-end starting as soon as May which is a clear affront to the central bank’s stale guidance.

- RBI: A hike is priced for the April 8th meeting with about 75bps of hikes within one year.

- Banxico: Markets would be surprised to see a cut this week with nothing priced until 25bps+ by Fall along a continued tightening path into 2027.

Many of these central banks are easing in real terms if the energy price shock persists even at materially lower prices than at present and they don’t raise their policy rates.

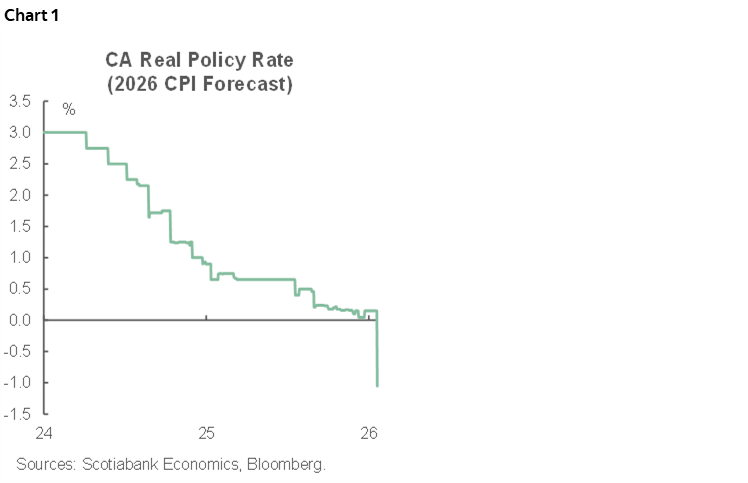

One example is shown in chart 1 for the Bank of Canada. Using our tentative CPI inflation forecast toward year-end as the measure of inflation expectations the BoC’s real policy rate has dropped by about 100bps. It would be unusual for the central bank to allow this to happen into a durable energy shock against which the BoC would tend to invoke a more restrictive stance. It’s the real policy rate that governs how monetary policy works through the economy and financial system.

Which leads to the first of two inexcusable behaviours on the street: the closed minds among the doves after their disastrous forecast errors throughout the pandemic.

The second inexcusable behaviour today involves believing in and reacting to every word that President Trump and his obsequious administration offer to markets. Late Friday, Trump said the war was going to end soon and he was leaning toward deescalation which drove oil prices lower into the close. And then there was Saturday night and then there’s today.

OTHER STUFF

There is nothing material by way of releases or anything other than the war to consider.

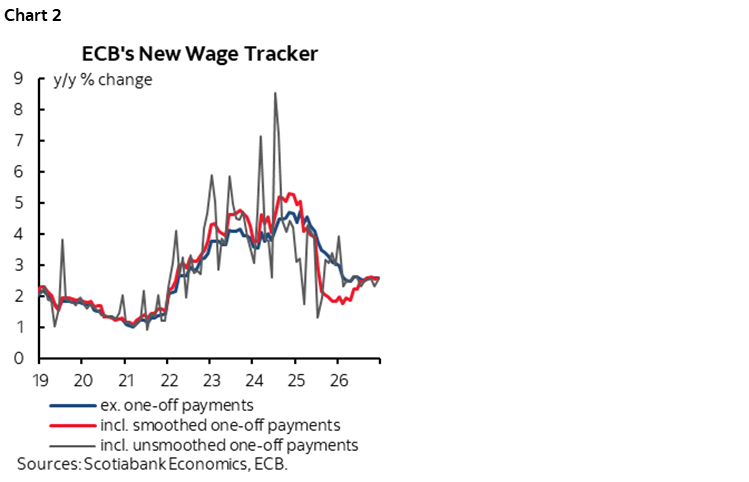

The ECB said last Thursday that it would be closely monitoring wages. Its Wage Tracker of expected wage changes accelerated in March to 2.6% for 2026Q4 and 2.5% for 2026Q3. That’s up from expected wage adjustments in the first half of this year (chart 2).

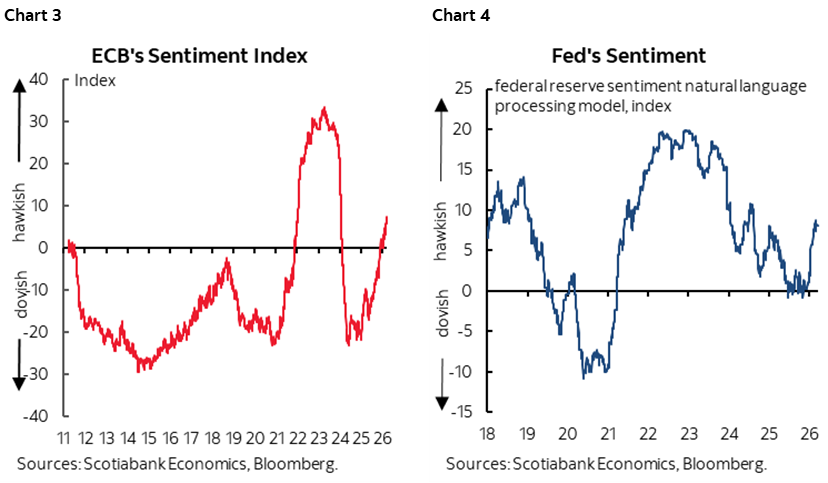

Hawkish ECB talk is continuing this morning as VP Luis de Guindos posted this interview and said “we are ready to respond as necessary” and “at the next Governing Council meeting in April, we will have more data on the conflict, which is the main source of uncertainty, and we will decide from there.” ECB Governing Council Member and Slovakian central bank Governor Peter Kazimir said in a blog post that if inflation risks remaining above the ECB’s target for a prolonged period, “we will act with appropriate forcefulness to bring inflation back down to our target.” He concluded: “People can rest assured we will not waver in delivering our mandate. If the path ahead gets harder, we will say so. If it requires bold action, we will not hesitate."

Sentiment among policy officials is clearly shifting (charts 3, 4).

The US only updates the Chicago Fed’s national activity index for February (8:30amET) and construction spending for January (10amET). Both will be treated as stale on arrival.

Ditto for Mexico that updates retail sales for January (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.