ON DECK FOR FRIDAY, MARCH 20th

KEY POINTS:

- Repricing of global central bank moves drives sharply higher shorter-term yields

- Oil up as Iran attacks Kuwaiti energy, Trump leaning toward major escalation

- Bets pile into Q2 hike pricing for the BoC as markets push the BoC

- Canadian retailers may be tracking a Q1 rebound

- Canadian producer price update to further inform coming upside risk to CPI

- Russian central bank cut, guided more

Oil is under renewed but mild upward pressure as Iran attacked Kuwaiti energy infrastructure and Axios reported that the Trump administration is considering plans to occupy or blockade Iran’s Kharg Island through which most of Iranian oil transits. So much for Trump’s claim that nobody really believes anyway when he says the war is almost over. Doing so would likely escalate Iran’s attacks elsewhere with more long-lived damage done to energy infrastructure which means higher for longer oil prices. So Brent is up a bit to about US$110. Gasoline futures are up by 2%.

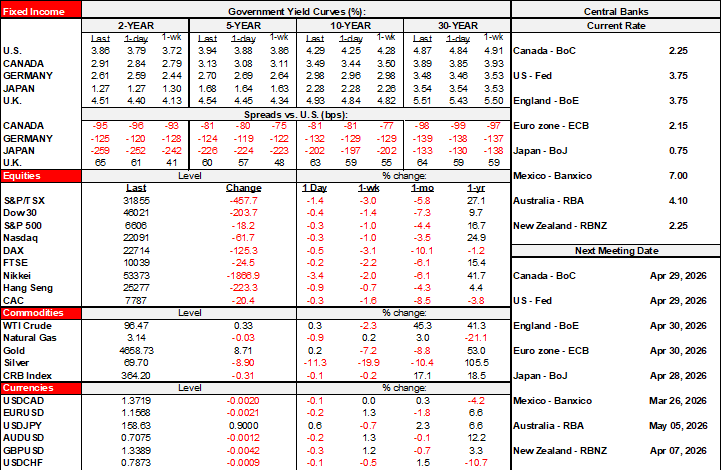

Sovereign yields are accordingly under upward pressure with the added driver being hawkish ECB sentiment and a broader repricing of the global central bank space. After post-meeting headlines indicated yesterday that the ECB would consider an April hike, this morning’s comments from ECB officials are mixed with Bundesbank President and Governing Council member Nagel indicating a bias toward hiking as soon as the April meeting while the rest of his colleagues are a little more cautious and circumspect—but not rejecting the option. Markets are about 70% priced for an April ECB hike with about 75bps of hikes priced through to year-end.

So let’s take stock here for a moment. There are important differences across their various back drops into the oil shock, but central bankers move as a herd. We have the RBA already hiking twice which started before the shock but got a boost from it. The BoE is sounding like it’s teeing up a nearer-term hiking bias. So is the ECB. The FOMC is signalling restrictive policy for a while yet.

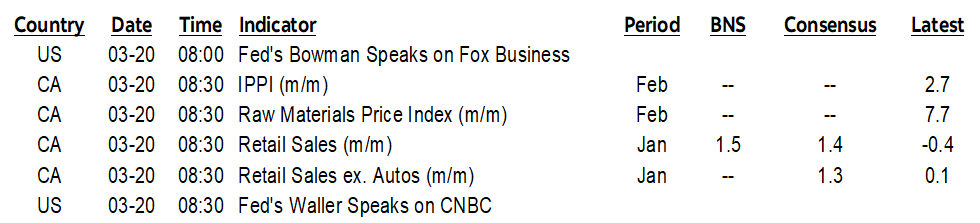

Enter the more commodity-sensitive central banks. I’d find it untenable that the BoC—which operates in a net energy exporting economy and generally commodity-intensive one—would choose to be the hold out among the majors and semi-majors despite being at the low end of the neutral rate range and at or below 0% in real policy rate terms. Layer on other arguments, like the mixed demand and supply side effects of trade negotiations and my bias that monumental stupidity would impose a larger trade shock along an oil shock into US midterms when the US administration is already drowning (chart 1). Fiscal policy remains in motion as well after the tentative budget the feds didn’t wish to present in the Fall gives way to future updates on more spending.

And so this morning we have someone—perhaps a leveraged hedge fund—clearly piling on a more hawkish bet that’s rapidly moving April OIS pricing a bit higher and pushing June pricing toward half of a hike priced which makes sense to me as previously argued. Canada 2s are up 7bps. It’s still early and a lot could happen, but if we go into Q2 with a hike priced into those meetings, then it’s probably done.

We’ll hear from other commodity-sensitive central banks next week that I’ll preview in my week ahead but they’re all probably going to sound incrementally more hawkish. The one exception being Russia’s central bank that cut 50bps this morning and guided perhaps another cut at the next meeting but it’s operating against a vastly different backdrop and, well, no luck is wished upon them!

Yields on gilts are continuing to lead the way higher after the BoE’s hawkish messaging yesterday; 2s are up 12bps and the curve is mildly bear flattening with OIS pricing about 70% odds of an April hike and about 75bps of hikes by year-end which is a full 125bps turn around from the end of February. US 2s are up 8bps. EGBs are broadly cheaper. Antipodean 2s were clobbered with Australia up 17bps and NZ up 13. South Korea’s 2s were up 10bps.

Across currencies, CAD is the shining beacon of resilience as it outperforms all others this morning.

Equities aren’t so happy. N.A. equity futures are off by ½% to ¾% with European cash markets faring a touch better. Let’s not get too carried away with the equity softness, however, as the S&P is only down 5% from the peak and back to November levels. In my view, that’s immaterial to forecasters so far from a smoothed wealth effect standpoint, but it could well worsen.

DATA RELEASES FOCUSED UPON CANADA

Friday ends with relatively light calendar-based risk in the wake of the deluge of central banks we’ve taken down this week. Developments in the Middle East will likely hold court.

Canadian macro data may be influential through tracking the consumer in Q1 and tracking producer price inflation. I think they’ll be important parts of the narrative.

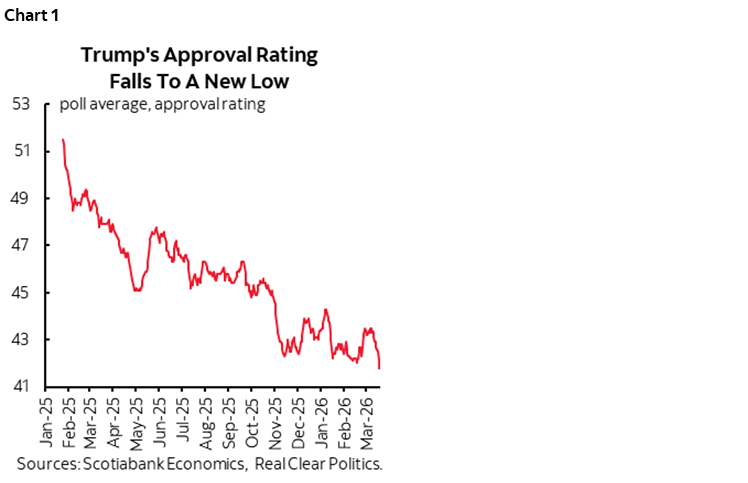

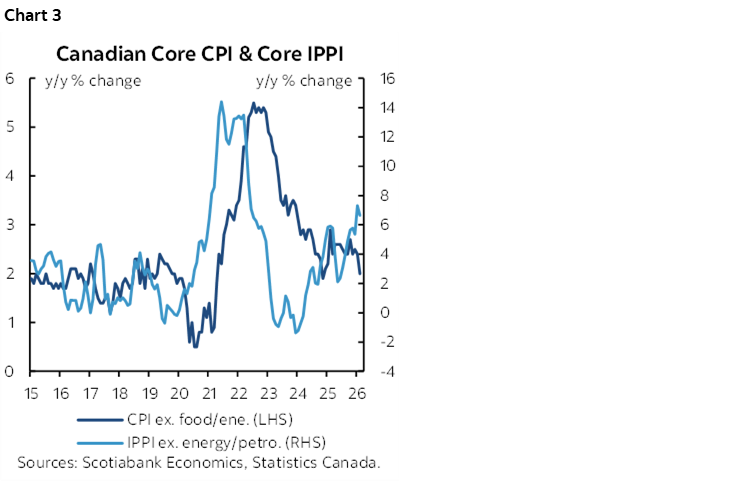

Statcan had previously guided back on February 20th that January retail sales (8:30amET) were estimated to be up by 1.5% m/m in nominal terms. Part of that gain is likely to be autos. Key will be volumes and breadth. The other key will be the advance guidance they provide for sales in February sans details for which I would expect some moderation from the prior month.

That said, because of the way Q1 started with a strong gain in January, we could be looking at a solid q/q annualized gain in retail sales volumes that represent around 40% of consumer spending to help inform Q1 growth tracking (chart 2). Tracking will be updated after the data. Weather and a bad flu season might dampen the way the quarter ends but that in turn could provide room for another math-driven gain in Q2.

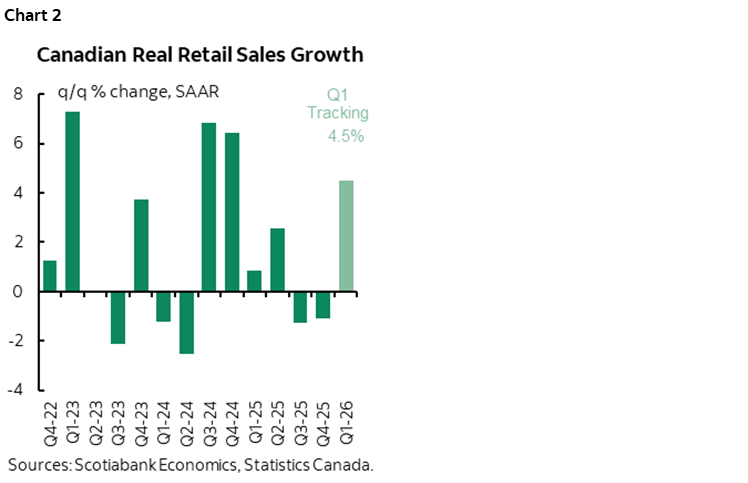

Canada also updates February readings for industrial and raw materials prices (aka producer prices) at the same time as retail sales (8:30amET). They’ve been on a sharp upswing of late which informs debate over pass through into consumer prices given lagging historical correlations (chart 3). Ergo, inflation risk remains pointed higher. Pay particular attention to core industrial prices ex-energy that jumped 2.8% m/m in January.

This has been part of an upswing since the start of 2024 that is showing no signs of abating. Core industrial product prices have risen by about 15% since then including tomorrow’s likely gain and tend to precede core CPI gains by 6–12 months. #notdead.

The US calendar will be dead quiet.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.