ON DECK FOR THURSDAY, MARCH 19th

KEY POINTS:

- Surging oil is hammering global markets

- Risk management should have the BoC open to earlier tightening

- UK jobs up, wages decelerated into the BoE

- BoE holds, delivers a nearer-term hike bias that drives yields sharply higher

- ECB will let its numbers do the talking and defer judgement

- BoJ holds, generally reinforces market pricing for nearer term hike

- CBCT warns about Q2 hike

- Riskbank’s extended hold challenged by markets

- SNB warns about the franc

- Aussie jobs gain on mixed details

- NZ GDP disappointment ignored

- Canadian small business inflation expectations ratchet higher

- US claims, new home sales on tap

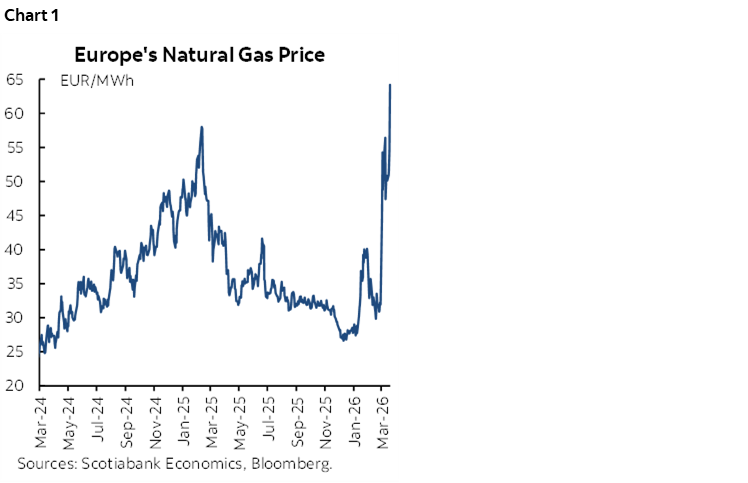

You really just need to know one thing about this morning’s markets and it involves looking at energy markets. Brent is up by about $14 since early yesterday as bilateral attacks on energy infrastructure intensify in the Middle East. WTI is relatively tamer this morning. European natural gas prices continue to skyrocket (chart 1). Sovereign yields are under upward pressure especially in the UK with 2-year gilts up 14bps and Down Under with Aussie and Kiwi curves bear flattening and, in both cases, aided by solid labour market readings. Stocks are broadly lower especially in Europe given its dependency on imported oil and gas. The USD is not picking up any safe haven flows as most currencies are gently firmer except for a flat CAD.

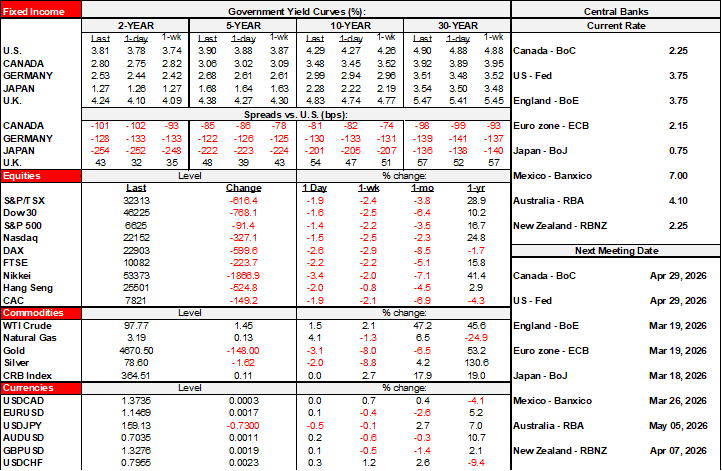

Recaps of the Bank of Canada and FOMC communications are available here and here. One point I made in my write-up is that I think the BoC is at risk of waiting until the cat is out of the bag on inflation risk. Again. They want clear evidence that the energy (and hence food and other commodities) shock is long-lived and clear evidence it passes into core before they will react. By that time it’s too late and that's how they blew it the last time. At some point, you need to know when to go off-model and impose judgement while taking a risk with imperfect information. If we get to the April MPR meeting or the June meeting and we have ongoing evidence of an energy shock, then I would take out an insurance hike at that time. Deliver it with dovish/neutral guidance if you wish, but don't leave the full adjustment until you are staring an inflation problem squarely in the face. Act in stages as information rolls in and be prepared to adjust in either direction in dynamic fashion as new information arrives rather than a sudden later rush to the exits that could make it harder to contain a broadening inflation threat.

BOE — FROM WHY ARE YOU EASING, TO WHEN ARE YOU HIKING?

Governor Bailey and the rest of the MPC were widely expected to pass on a rate change this morning and did exactly that in unanimous fashion. Key, however, was the remark that the MPC members “stand ready to act” which is code language for a pivot toward a hiking bias. As a result, the gilts curve exploded with the 2s yield up 30bps and counting this morning, sterling firmer, and markets learning toward a hike at the April 30th decision. One motivator is the war with Iran but frankly it’s also an opportunity to abandon an easing campaign that was increasingly making little to no sense. Here’s the full passage:

"Monetary policy cannot influence global energy prices but aims to ensure that the economic adjustment to them occurs in a way that achieves the 2% target sustainably. The MPC is alert to the increased risk of domestic inflationary pressures through second-round effects in wage and price-setting, the risk of which will be greater the longer higher energy prices persist. The MPC is also assessing the implications for inflation of the weakening in economic activity that is likely to result from higher energy costs.

The Committee will continue to monitor closely the situation in the Middle East and its impact on global energy supply and energy prices. It stands ready to act as necessary to ensure that CPI inflation remains on track to meet the 2% target in the medium term."

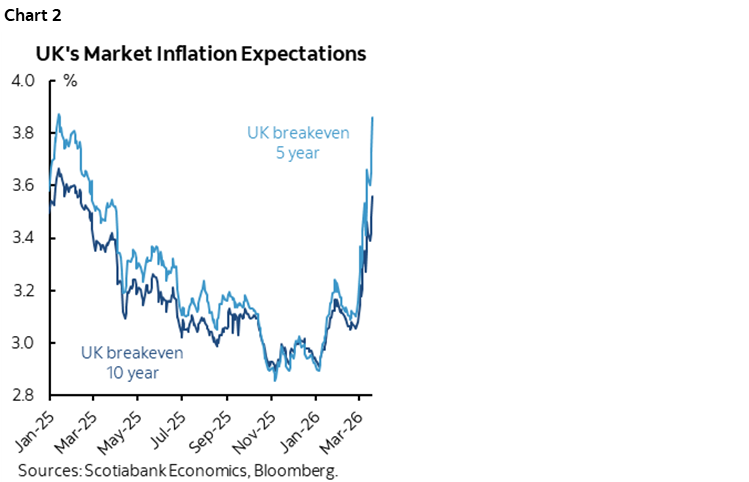

With the rise in Brent oil prices has gone an increase in inflation expectations derived from inflation-linked bonds (chart 2). Recall that the starting point for UK CPI inflation is 3% y/y as of January with core inflation at 3.1% and services CPI up 4.4%, making the UK very different from the Eurozone’s starting point. Progress toward reduced inflation has been made even over the past six months or so, but mission accomplished is nowhere in sight especially with the uncertainty of an oil shock looming overhead. The BoE took down constructive labour market readings for January and February this morning.

In short, the market is quite rightly questioning why the BoE would be contemplating further easing given the starting point and the added layer of uncertainty over how energy prices drive headline inflation and perhaps spill into core inflation.

ECB — THE NUMBERS WILL DO THE TALKING

No policy changes are expected when the ECB delivers its decisions this morning (9:15amET) and President Lagarde speaks 30 minutes later. The deposit rate is expected to stay at 2%. Key may be the forecasts.

Markets have brought forward hike pricing and see 50–75bps of tightening before year-end. Lagarde is likely to sound patient and reticent to prematurely judge further developments in the Iran war.

Key will be the degree to which the Eurosystem staff macroeconomic projections update the inflation forecast. The last forecast in December expected total inflation to gradually ease to 1.9% in 2026 and 1.8% in 2027 with core inflation at 2.2% and 1.9% over the two years respectively.

Higher oil and natural gas prices put upside risk to this projection for total inflation, but only if sustained. Further, we’ll want to hear President Lagarde’s judgement being applied to the prospect of a generalized inflation shock or a relative price shock attributed to higher energy prices.

The Eurozone economy is neither in a state of material excess demand nor supply but facing downside risks to growth while wage growth has eased but remains above the 2% inflation target. Therefore, a surge in energy prices could add to near-term inflation risk but quash inflation through second-round effects by crimping purchasing power of consumers.

If so, then the ECB may not wish to make the same mistake that former President Jean-Claude Trichet may have made in 2011 when he hiked the deposit rate on the heels of the Global Financial Crisis because of commodity-induced inflation risk only to reverse the hikes months later. Oil prices had been rising by over one-third from late 2010 to early 2011. Back then, core inflation peaked at about 1½% y/y and then began sliding back to under 1%.

BANK OF JAPAN—MILDLY HAWKISH, SUPPORTING MARKET PRICING FOR A NEARER TERM HIKE

Markets slightly increased the odds of a hike at the April 28th meeting to 60% with June 85% priced for a hike in the wake of BoJ communications overnight. Governor Ueda and his team held at a target rate of 0.75% as universally expected, but guidance was a touch more hawkish. Ueda flagged that more Board members were concerned about upside risk to inflation stemming from higher oil prices and emphasized Spring wage negotiations that are driving another strong gain. Overall, he noted that it’s early to assess the effects of the war with Iran, but said that if the economy is dented by higher oil only temporarily “then of course it will be possible to raise interest rates.” He did not provide explicit forward guidance on timing another hike.

RIKSBANK’S EXTENDED HOLD CHALLENGED BY MARKETS

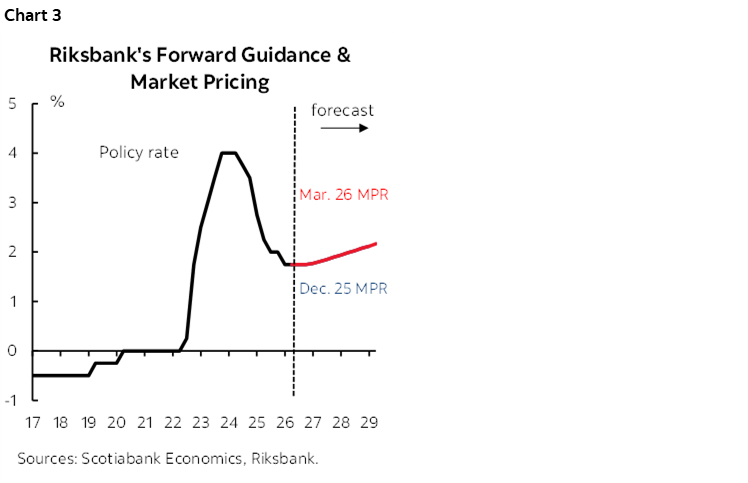

Sweden’s Riksbank held at a policy rate of 1.75% as widely expected. Updated explicit forward guidance pointed to a rate hold “for some time to come” that the numbers backed up by showing no move until possibly 2027 and only a single 25bps hike (chart 3). Markets aren’t having it, however, as they price a solid chance at a hike later this year and 50–75bps of tightening through to next year.

CBCT GUIDES POTENTIAL HIKE IN Q2

Taiwan’s central bank left its benchmark rate unchanged at 2% as widely expected. Guidance sounded incrementally hawkish. Governor Yang Chin-long said “If the conflict drags on, it could have a relatively large impact on energy prices, and correspondingly, a greater impact on global economic growth. Our monetary policy will move in a tighter direction; the key lies in the second quarter.”

SNB WARNS MARKETS ABOUT THE FRANC

Switzerland’s central bank left its policy rate at 0% as widely expected. SNB warned markets against treating the franc as a safe haven by stating “Given the conflict in the Middle East, the SNB’s willingness to intervene in the foreign exchange market has increased. The SNB thereby counters a rapid and excessive appreciation of the Swiss franc, which would jeopardise price stability in Switzerland.”

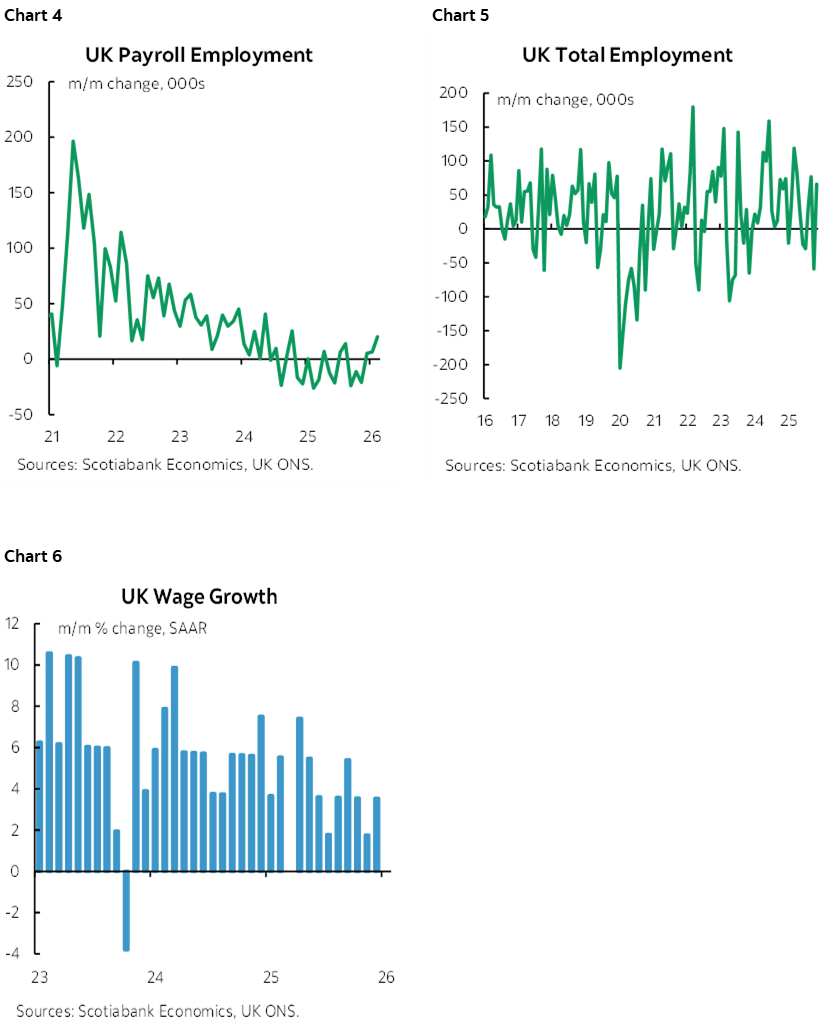

MIXED UK LABOUR MARKET READINGS

UK job market readings just ahead of the Bank of England will lend support to a hawkish hold. Charts 4–6.

- Payroll employment increased by about 20k jobs in February for the third straight monthly gain.

- Total employment rebounded with a 66k gain in January after dropping by a similar amount in December. Gains have been registered in three of the past four months.

- job vacancies fell a touch and remain slightly above a long-run average.

- wage growth, however, came to a halt in January (0% m/m), cooling the three-month moving average to 1.8% m/m SAAR.

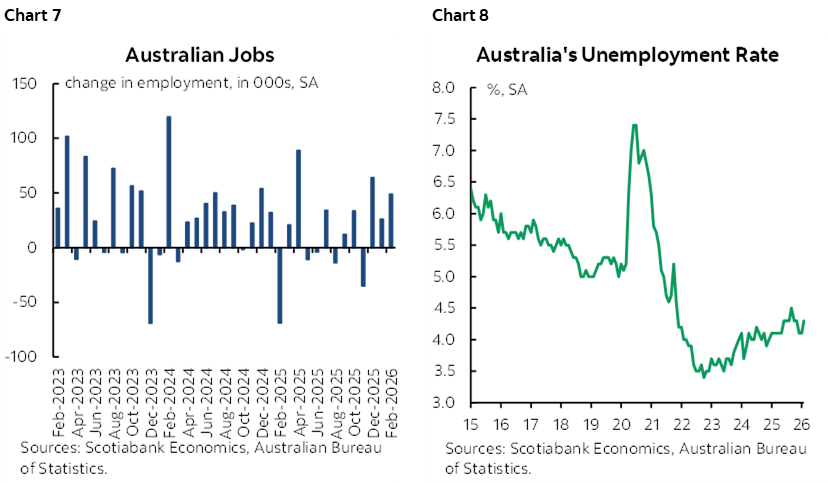

AUSTRALIAN JOBS REINFORCE HIGHER YIELDS

Australia’s yield curve was already vaulting higher before fresh jobs figures that added to the upward pressure. Total employment climbed by 49k with an upward revision to +26k in January (from 18k). It was all part-time jobs, however, as they climbed by 79k with full-time jobs down 31k and with both readings reversing prior moves in the opposite directions. The unemployment rate climbed two-tenths to 4.3% because the labour force expanded with the labour force participation rate up two tenths to 66.9%. Charts 7–8.

NZ GDP DISAPPOINTMENT IGNORED

New Zealand’s GDP growth disappointed in Q4 by coming in at 0.2% q/q SA along with negative revisions to Q3 (0.9% from 1.1%). The figures were dismissed by the currency and NZ rates curve as oil dominated.

LIGHT N.A. DATA

Canada will be quiet today with just the CFIB’s small business survey indicating higher inflation expectations that lead the BoC’s measures given greater freshness and frequency (chart 9). Still, even the CFIB measures are likely to be lagging the fast pace of developments and so stay tuned for next month’s readings and subsequent ones.

The US updates weekly jobless claims (8:30amET) and new home sales during January (10amET) that are expected to fall.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.