ON DECK FOR TUESDAY, JUNE 9th

KEY POINTS:

- Calmer markets await ramped up developments

- Bonds don’t always know best when it comes to the Fed

- Canada’s stupidly timed youth social media ban

- Bank Indonesia surprises again

- Modest overnight readings

- US, Canadian trade and US home sales on tap

A calmer market landscape awaits more material developments starting tomorrow with US CPI and the BoC and then Thursday’s ECB communications. For now, oil is off by US$2/barrel as the daily gyrations on war headlines are never ending. Sovereign bond yields are lower by about 1–2bps across global benchmarks. Stocks are broadly higher across NA futures and European cash markets (except London) and following a mixed Asian session where the outlier move was South Korea’s Kospi that gained over 8% after losing the same amount the previous day.

BONDS DON’T ALWAYS KNOW BEST

A narrative across markets remains that the market knows best and the Fed is going to hike. This is used as justification for not only the priced quarter-point hike by year-end and perhaps another in 2027, but also a view that the Fed could hike much sooner than that. Be careful.

The bond market has delivered some accurate calls, and many spectacular failures throughout years of the market-knows-best hubris. Take the aftermath of the GFC around 2010, for instance; the bond market was convinced that the Fed would be hiking on the view that the GFC would be quickly shaken off and policy would be normalized; instead, the policy rate wasn’t raised until the end of 2015. Or take 2023, when the market was pricing Fed rate cuts in response to the regional banking crisis marked by the failure of Silicon Valley Bank without understanding the argument that the Fed had tools other than the policy rate to use in addressing the funding and liquidity challenges. Or how about 2021–22 when the bond market slept its way into the inflation shock, pricing very few rate hikes back in early 2022.

The bond market represents the distillation of all views based on publicly available information and serves as a clearing house for the street’s opinions. It is hardly infallible, however, as it makes spectacular mistakes. For my two cents, it’s wrong to be pricing hikes now.

As previously noted, Friday’s jobs report was probably a FIFA World Cup report on hiring in the leisure and hospitality sector with little breadth to the payroll gain. This was part of my reasoning for going toward the top of consensus for the May payroll estimate and the coming effects were cited in my May 1st weekly:

“FIFA World Cup hiring may begin to make contributions in May but with the bulk of the hiring focused upon June and July before this effect reverses afterward. Estimates of the number of folks who will be hired or volunteer on a temporary basis push into the hundreds of thousands.”

This also feels like a different inflation shock that shouldn’t merit an overreaction by the already restrictive Fed. AI is driving some prices higher for now, tariffs are doing likewise for some goods prices but this effect may be waning, and the energy shock is raising limited passthrough risk to date. Warsh will shift inflation metrics toward some central tendency measure like trimmed mean which is behaving much better than core pce, indicating that this is more about a relative inflation shock than a generalized outburst. Annual nonfarm benchmarking revisions in September—one week before the FOMC—and downside risk to payrolls over H2 could pivot the Fed narrative pretty significantly.

MODEST DATA DEVELOPMENTS

There were few fresh developments overnight and what’s on tap isn’t likely to be terribly impactful.

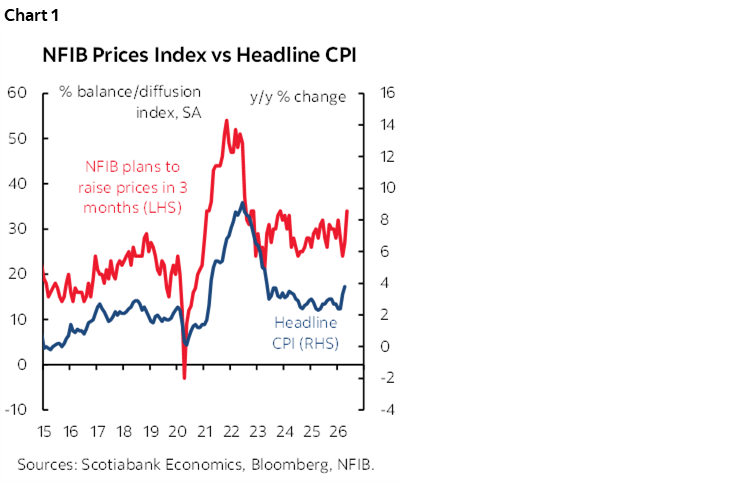

The US NFIB small business confidence readings for May were notable for hitting the highest share of businesses planning to raise prices over the next three months since November 2023 (chart 1).

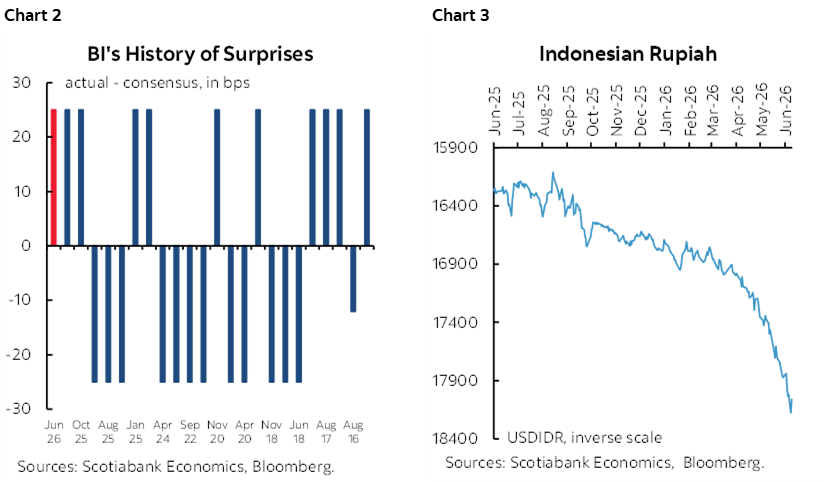

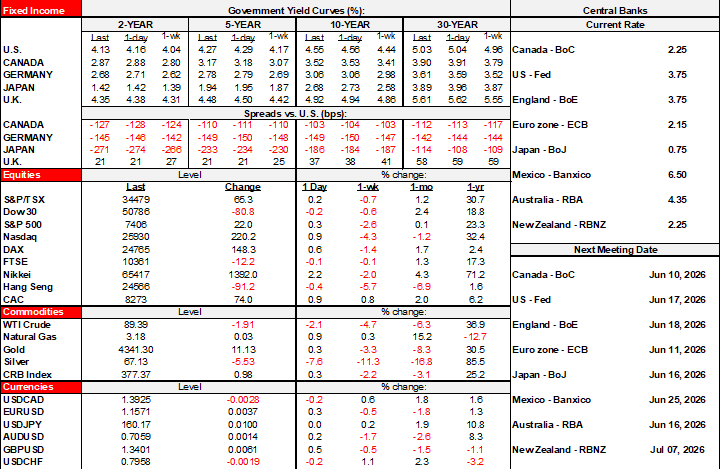

Bank Indonesia surprised markets with another unplanned intermeeting rate hike of 25bps to 5.5%. The aim was to support the tumbling rupiah as southeast Asian currencies have been getting hammered for a while. It worked, somewhat, as the rupiah slightly appreciated overnight to lead Asian crosses against the dollar. Still, the policy rate has been raised by 75bps since May 20th (+50bps) including last night’s 25bps move, yet the rupiah has continued to depreciate by about 2% throughout the cumulative hikes. The history of wild-west surprises continues (chart 2) and the rupiah trend shows that further reforms are needed (chart 3).

Germany’s economy posted solid export, import and industrial output readings in April. Exports climbed by 0.9% m/m against expectations for a drop, imports grew by 1.2% m/m (consensus -2%), and industrial output was up by 0.4% which matched consensus but there were solid upward revisions.

On tap into the N.A. session will be a handful of US and Canadian readings. The US trade deficit should narrow given we already know the goods component (8:30amET). Canada’s trade figures will help to inform Q2 growth tracking (8:30amET). The US ADP weekly gauge of payroll changes isn’t terribly helpful given revisions when the monthly measure arrives and because it tracks initial nonfarm private payrolls poorly (8:15amET). US existing home sales will probably be little changed during May (10amET).

CANADA’S SOCIAL MEDIA BAN IS POORLY TIMED

Should Canada ban social media for kids under 16? That’s the government’s plan with possible exemptions should social media firms prove they can keep kids safe while using their platforms. That exemption could be the way out if companies—including gaming platforms that are notorious for poor controls—continue to tighten their standards. The effort would resurrect Bill C-63 that went nowhere in the transition from former PM Trudeau to PM Carney.

I have my personal views on social media for kids and don’t support a blanket ban, but will stick to the main point on the economics in asking this question: Canada, do you want a trade deal with the US, or not?

This could add a potentially new trade irritant into the middle of CUSMA/USMCA trade negotiations. At a minimum, the timing is off, in a left-hand doesn’t know what the right-hand is doing kind of way which has been all too common as a practice. The US tech bros have close ties to the Trump administration including their explicit financial support. Just as they lobbied against the Online Streaming Act and the Digital Services Tax, they may make the social media ban an issue that holds up negotiations and do so out of their own self-interest. Regardless of what one thinks of the merits, your timing stinks, in other words. As in ‘why now???’ You knew that the Trump administration opposed Australia’s ban and you’ve heard the warnings to the Starmer regime in the UK (here) but went ahead anyway. The own goals by the feds and provincial governments risk scuttling the talks in the absence of a more disciplined approach focused upon the overall welfare of Canadians. I smell another policy error about to be humbled.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.