ON DECK FOR MONDAY, JUNE 8th

KEY POINTS:

- Oil, bond yields spike on escalating conflict in the Middle East

- South Korea counters won depreciation

- Peru faces ongoing political instability with no clear election outcome

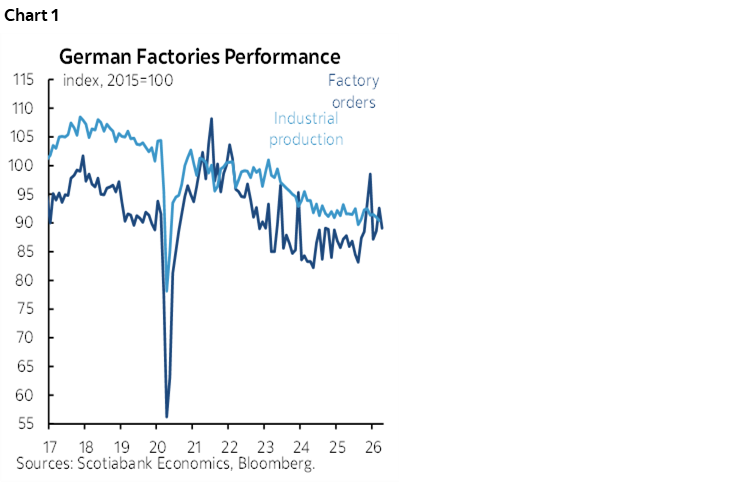

- German factory orders give back prior gain

- Chile CPI to be the last reading before next week’s BCCh decision

- Global Week Ahead — Looking Through Everything and Nothing (reminder here)

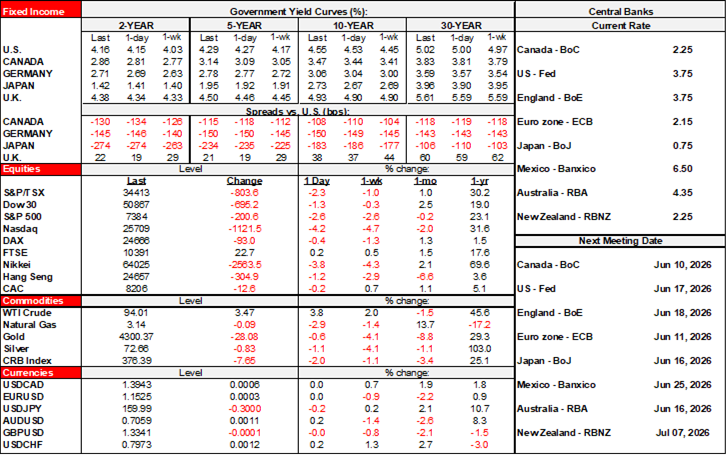

A risk off tone is marking the start of a fresh week. Oil is up by about US$4/barrel. Higher inflation fears are driving sovereign bond yields higher across all markets. Stocks are mixed with US and Canadian futures a touch higher while European cash markets are gently lower after bigger selloffs across Asian benchmarks. The dollar is slightly firmer against several majors except the yen while the won is the strongest performer after the government took steps to lean against currency weakness that are at least temporarily effective.

Some of all of this is the lagging Asian market reaction to Friday’s nonfarm payrolls. Some of it may be in anticipation of the week’s developments. Much of it is driven by escalating conflict in the Middle East after Israel attacked Beirut, Iran fired retaliatory missiles at Israel and then Israel retaliated against targets in Iran. This followed earlier clashes between the US and Iran. Clearly there is no peace in sight and despite stomping around on social media, Trump has absolutely no control over the circumstances. The combined effects are driving Treasury yields up by 2–4bps in a bear flattener move and minor dollar strength.

Peru’s markets may be volatile into their open as the second-round Presidential election is too close to call in exit polls thus far. Recounts are likely which means that the official results could take many days or weeks to become available. Whatever the outcome, political instability is likely to continue with this being the ninth leader to be elected in ten years; one would be forgiven for not remembering any of their names.

German factory orders fell by a whopping 3.8% m/m SA in April but this reverses the 4.5% surge the prior month (revised from 5%). The trend remains volatile but generally pointed higher over the past year (chart 1).

The only release on tap today will be Chilean CPI for May (8amET) that is expected to accelerate to over 4% y/y ahead of next week’s policy decision by Chile’s central bank.

Having said all of that, it’s just the tip of the proverbial iceberg in terms of an active week ahead. My weekly explores previews for the Bank of Canada (Wednesday), ECB (Thursday), US CPI (Wednesday), expected holds by central banks in Peru and Turkey, SpaceX’s whopping IPO (Friday), Peru’s elections and several global data releases.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.