ON DECK FOR THURSDAY, JUNE 18th

KEY POINTS:

- US Treasuries continue flattening the day after the FOMC

- The US waved the white flag in its MOU with Iran

- BoE held amid MPC divisions

- UK job growth ebbed as wages accelerated

- Canadian small businesses point to increases in BoC’s inflation expectations

- Canadian producer price update to inform lagging consumer pass through

- BI hiked again and tightened FX rules

- BSP might have hiked by more given the peso reaction

- SNB warns on FX intervention

- Norges Bank held, issued lukewarm hike guidance

- US quiet with just claims on tap

The day after Kevin Warsh’s debut is offering a calmer market backdrop in US and Canadian markets as the rest of the world catches up. My FOMC recap is available here. The US Treasury yield curve is flattening a touch with 2s slightly cheaper and the longer end rallying on hope that the Fed will act to contain inflation pressure. Canada’s curve is doing likewise. Gilts and EGBs are catching up to yesterday afternoon’s FOMC communications and driving curve flatteners with shorter-term yields up by about 5bps across Europe. Antipodean yields performed similarly but the kiwi curve is underperforming everyone else.

Stocks are mixed, with US and Canadian futures up a touch but European cash markets are in the red as they catch up. The dollar is a bit firmer again this morning in an extension of yesterday afternoon’s reaction.

Bank of England — Holds Amid MPC Divisions

The Bank of England left Bank Rate unchanged at 3.75% as priced and universally expected. The 7–2 vote positioned the majority against two MPC members who called for a 25bps hike (Pill and Greene). Divisions on the MPC were substantial as some members were more encouraged by the US-Iran MOU with fewer concerns about second round effects on inflation, while Governor Bailey noted he accepts that inflation risks are skewed to the upside and pressures from the war are still in the inflation pipeline.

The two-year gilt yield is about 5bps higher this morning but was little affected by the BoE’s communications. Ditto for sterling. Markets eased off nearer-term pricing for a BoE hike but retained pricing for about 30bps of tightening by year-end.

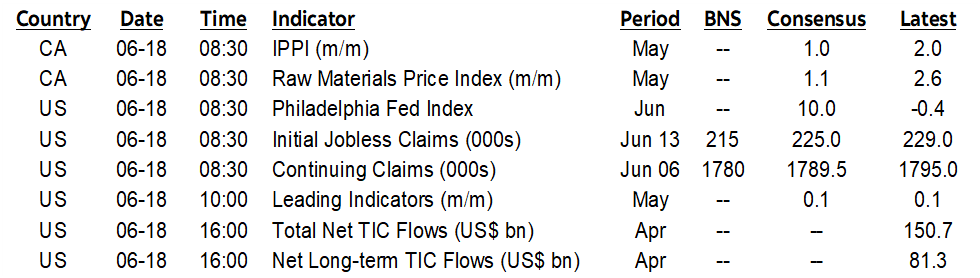

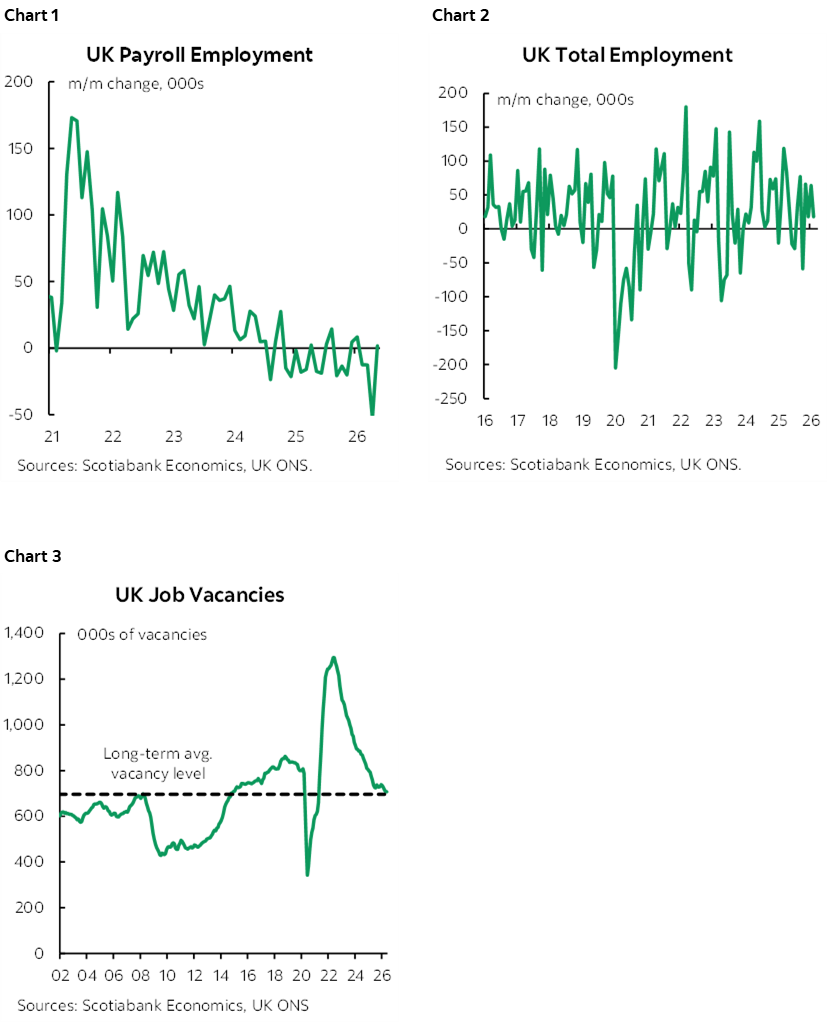

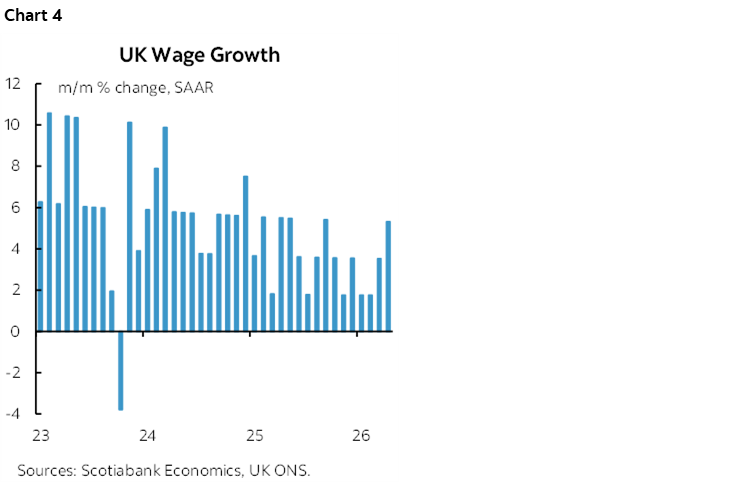

UK Job Growth Ebbs, Wages Accelerate

UK job growth basically ground to a halt as wage growth accelerated just hours before the Bank of England’s decision. Payroll positions were little changed with just 1,733 new spots added in May. Total employment lags, but April was also little changed with just 18k overall jobs added. Both have been decelerating for a while (charts 1, 2). There was also little change in job vacancies (chart 3).

Yet wage growth accelerated to the fastest pace since September. Wages were up by 5.3% m/m SAAR (chart 4).

Bank Indonesia — It Worked, for Now

Indonesia’s central bank hiked its policy rate by another 25bps overnight, matching the expectations of the majority of forecasters notwithstanding a significant minority who thought they’d hold and a pair who called for +50. BI also tightened some of the regulatory rules around FX activity. The one-two punch was aimed at controlling the rupiah’s weakness and it had been depreciating post-Fed and pre-BI. The move worked for now as the rupiah bounced back following the decision to reinforce the pattern of gains since the emergency meeting delivered a hike back on June 9th.

BSP — Should’ve Hiked by More?

If the aim of the overnight rate hike that was delivered by Bangko Sentral ng Pilipinas was to control the peso’s slide, then it didn’t work so well. The peso slipped further after the overnight rate went up by 25bps to 4.75% for the second hike following the one on April 23rd. Governor Remolona guided that BSP is prepared to hike again amid concern that inflation would persists above the 4% target ceiling throughout the forecast horizon. Given the peso reaction and BSP’s forecast for inflation to persistently target the upper ceiling, perhaps BSP should have appeased the sizeable minority who called for +50bps and were disappointed by the aftermath.

New Zealand’s Economy Beats on Revisions

Kiwi Q1 GDP grew by 0.8% q/q SA nonannualized, matching expectations, but the prior quarter was revised up by three-tenths to 0.5% for an overall net beat. Q1 growth was led by services (+0.5% q/q), agriculture/forestry/fishing (+1.2%) and manufacturing (+1.9%) as mining shrank (-11.6%) along with construction and utilities output. The NZ$ was soft but outperformed other major crosses against the USD overnight.

SNB — FX Intervention Warning

To no one’s surprise, the Swiss National Bank stayed on hold at a policy rate of 0%. A warning that it is increasingly prepared to intervene in FX was met by currency softness as the franc slipped overnight against the dollar and euro but was flat to sterling.

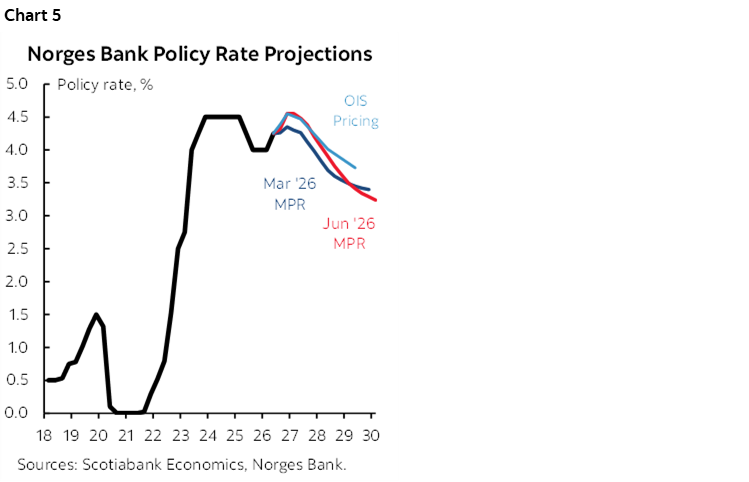

Norges — A Lukewarm Hike Warning

Norway’s central bank held its deposit rate unchanged at 4.25% after hiking on May 29th. The krone fell even as Norway’s short-term bond yields spiked higher on guidance that further policy tightening is likely. Explicit forward guidance (chart 5) noted that the rate outlook was raised compared to the last time in March “and is just above 4.5% at the end of the year.” Chart 5 demonstrates that this forward guidance is nevertheless expected to represent temporary tightening to thwart second-round effects on inflation as tightening subsequently reverses later on in the forecast horizon. Having said that, the guidance around the risks to this outlook was fairly even handed, as Norges noted much depends on the speed of normalization in energy markets and how domestic data evolves.

Light N.A. Data Focused on Canadian Inflation

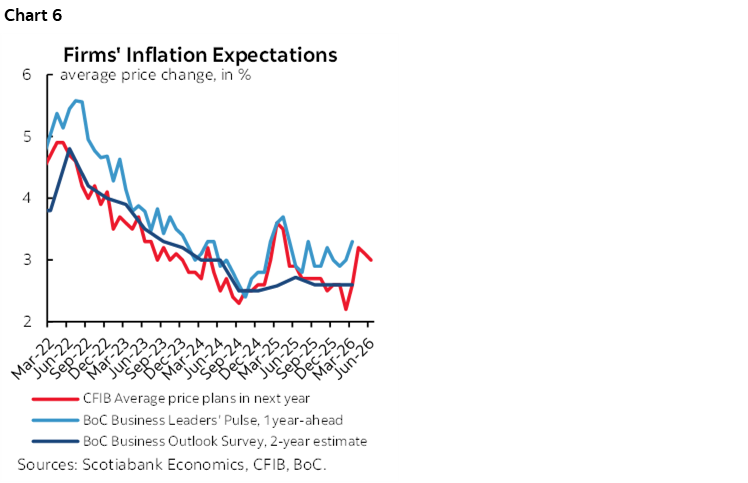

Canada is getting a pair of inflation teasers ahead of next week’s CPI refresh. For one, the CFIB—a small business association and lobby group—released its monthly survey this morning. Its monthly measure of inflation expectations tends to lead the Bank of Canada’s quarterly business survey and is more timely than the BoC’s monthly Business Leaders’ Pulse survey. Chart 6 shows that the CFIB survey points to the next quarterly BOS measure of inflation expectations in July moving much higher and there is a strong correlation notwithstanding mismatched 1- and 2-year horizons. The CFIB measure tends to track beneath the BLP monthly measure which suggests that the Pulse measure of 1-year ahead inflation expectations could remain elevated with upward pressure.

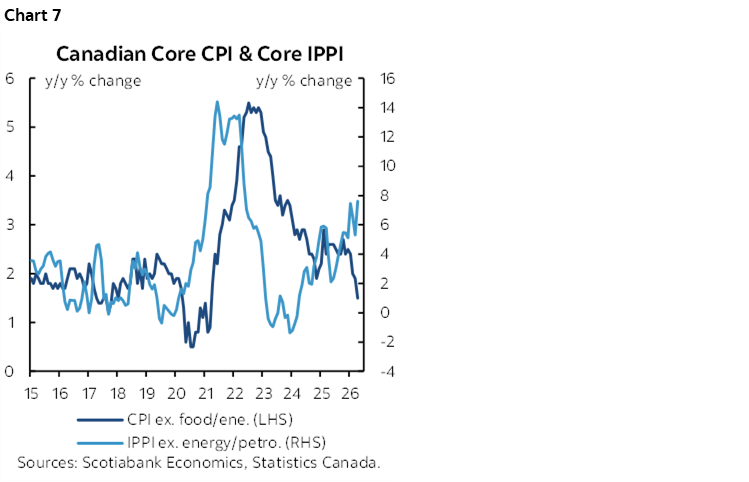

Canada will also refresh producer prices for the month of May this morning (8:30amET). Further gains in industrial and raw materials prices are likely, but key remains assessing the trend in core industrial prices. April’s industrial prices ex-energy jumped by 1.1% m/m which lifted the year-over-year rate to 7.6% and that serves as a leading indicator of coming pressures on core CPI (chart 7).

The US goes relatively quiet today with weekly jobless claims on tap (8:30amET).

US-Iran M.O.U. Text

The text is finally out from both sides at first from the US yesterday following earlier leaks and this morning from Iran’s President (here). The US may as well have sounded the bugle retreat call and waved the white flag in my opinion. Trump’s low bar for deal success points to the stock market’s reaction which is an odd arbiter of foreign affairs lacking the foresight to anticipate future developments in the Middle East including deferred conflict. I mean, seriously, have you learned absolutely nothing about the stock market and Middle East tensions dating back to the Gulf War??

There is plenty of scope for the MOU to fall apart including the open window beyond 60 days.

Take, for instance, point #1 that calls for the end of conflicts on all fronts including Lebanon. That requires Israel to be onside. Good luck.

Point 4 requires the US to end its blockade within 30 days and remove all US forces in “proximity of Iran.”

Point 5 says Iran will open up the Strait of Hornuz with no fees, for 60 days but Iran’s President noted that Iran and Oman will then discuss the future administration of the Strait including fees.

Point 6 explicitly notes the creation of a fund worth at least US$300 billion for the reconstruction and development of Iran. The form of the fund will be established over the 60 day negotiating period. Trump has said that US taxpayers won’t foot this bill. Who will and how remains a mystery.

Point 7 ends all sanctions against Iran including UN Security Council resolutions and ones imposed unilaterally by the US. How and when will be part of the negotiations. This is likely to involve Congress in which case the Iran hawks will probably resist.

Point 8 gives Iran’s Scout’s honour pledge not to develop nuclear weapons which Trump emphasizes over and over. It’s a hollow offer. Iran has proven itself to be untrustworthy as it kicked inspectors out of the country, secretly worked on a nuclear research program hidden deeply underground and built stockpiles of enriched uranium. Trump says they have cameras everywhere, but Iran is good at moving things around and hiding its actions with the scientific support of the Russians. I think the US administration is foolishly counting on Iran’s word and what to do about the enriched uranium stockpiles is to be part of the negotiations over the 60-day window.

Point 11 states that the US will “make fully available frozen or restricted funds.” This too is a gift to Iran that enables it to redeploy frozen assets toward rebuilding including its armed forces.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.