ON DECK FOR WEDNESDAY, JUNE 17th

KEY POINTS:

- Markets playing it safe ahead of key developments

- FOMC preview—Dots versus the press conference

- US retail sales to inform Q2 consumer spending

- Trump may offer more Iran details at this morning’s press conference

- UK CPI sets up a patient BoE tomorrow

- Riksbank warns of coming hike but guidance may be stale

- Brazil’s central bank expected to cut post-Fed

Global markets are playing it safe so far this morning ahead of several developments. They include this afternoon’s FOMC communications, this morning’s update on US consumer spending, and Trump’s press conference at 10:20amET on the sidelines of the G7 Summit. At that presser, Trump has pledged to discuss more about the apparently R-rated MOU with Iran that us adults have not been allowed to see thus far. Trump noted this morning that the MOU is not finalized, batted away some of the rumoured content, and said that if he doesn’t like what he sees, then the US will strike Iran again. This is a problem of his own making as there is no available text. Also note that Iran is claiming that the deal includes a requirement for Israel to withdraw from Lebanon which I’d give about 0.000001% odds of happening.

And so at present we’re staring at oil prices moving a few dimes higher this morning, slight strength in the USD against multiple crosses except the yen and Swiss franc, and small gains in most equity benchmarks. Rates curves are performing rather blandly except for outperformance in gilts (post CPI, see below) and Sweden’s curve (post Riksbank, see below).

FOMC — DOTS VERSUS THE PRESS CONFERENCE

The FOMC statement and Summary of Expectations including the dot plot arrive at 2pmET and will be followed by Chair Warsh’s first press conference at the helm thirty minutes later. A comprehensive preview was provided in my weekly here which I won’t repeat here but encourage readers to review given there are a lot of potentially moving parts into this one.

I would expect the balance of the dots projection to remove the median participants call for a rate cut this year but for Warsh’s press conference to sound more neutral-dovish than the dots which he’ll likely boycott. The March dot plot had seven participants in the no cut camp, seven in the -25bps camp, and five expecting more than one cut. The bottom part of the distribution expecting more than one cut is likely to be trimmed or removed and the balance is likely to shift to a hold with some hike projections. That could be a set up for a different tone in the press conference which could drive meaningful market volatility this afternoon.

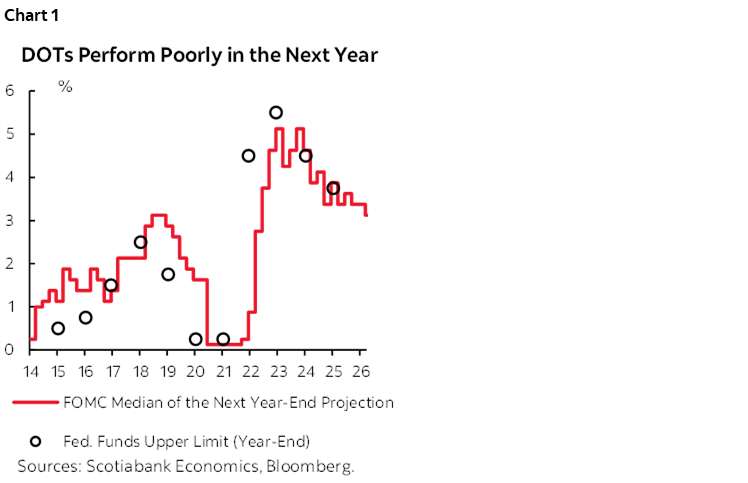

And who cares. The dots perform terribly relative to what the FOMC actually winds up doing (chart 1 for example) which is part of the reason why Warsh loathes forward guidance.

My weekly lays out further expectations.

US RETAIL SALES EXPECTED TO POST A SMALL GAIN

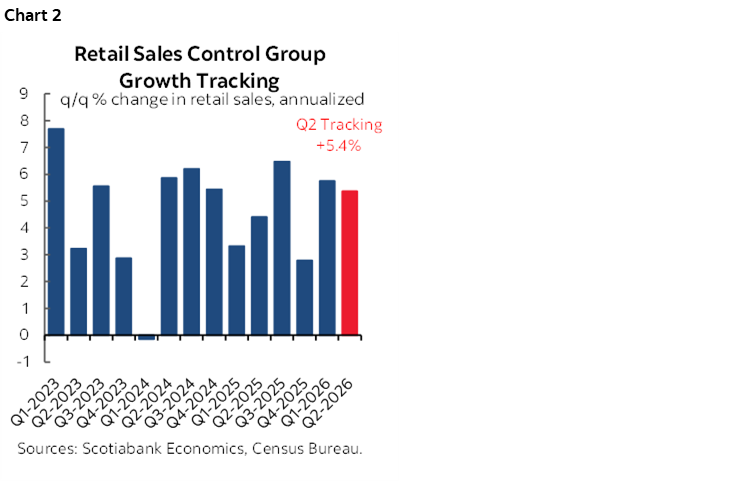

Before the Fed we’ll get US retail sales for May (8:30amET). A small rise in vehicle sales and higher gasoline prices should contribute to a modest gain with consensus at 0.6% m/m and I’m at 0.4%. Key will be sales ex-autos and gas but that too will only be in nominal terms including price effects so turn quickly to volume estimates in the aftermath. For purposes of estimating consumption in the GDP accounts key will be the control group that omits categories like gas, autos, building materials and food services and which is tracking a solid gain but this is in nominal dollar terms not adjusted for price effects (chart 2).

Post-data we will also be able to refresh tracking of retail sales volume growth. Q1 was up by just 1.2% q/q SAAR after applying linear interpolation to fill in an estimate for October given missing data due to the government shutdown. So far, Q2 is tracking 2.3% q/q SAAR based only on the Q1 average and April.

SOFT UK CPI SETS UP A PATIENT BOE TOMORROW

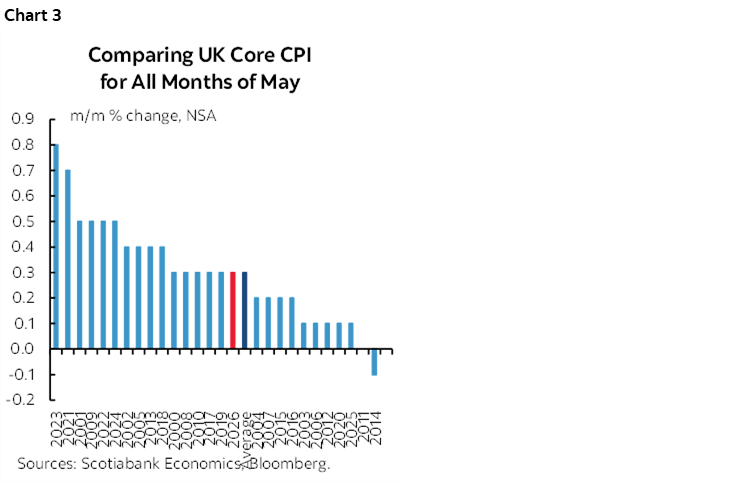

UK inflation came in beneath expectations on the eve of the Bank of England’s decision. Headline CPI at 0.2% m/m seasonally unadjusted (NSA) was half of consensus with the year-over-year rate at 2.8% (consensus 3%). Core CPI at 0.3% m/m NSA was relatively soft compared to a normal month of May (chart 3) which contribute to the year-over-year rate of 2.6% slightly undershooting consensus by a tenth. Services inflation, however, warmed up to 3.7% y/y (3.2% prior, 3.6% consensus). Other price gauges like the retail price index (0.2%, 0.5% consensus) and producer prices (0.5% on consensus) reinforced the general bias.

As a result, the gilts curve rallied by 5–6bps across maturities, sterling slipped a touch, and markets lowered pricing for Bank of England hikes. Nothing remains priced for tomorrow with only a slim chance at a hike next month, half a hike in September, and a full hike isn’t priced until December but is down a few basis points post-data.

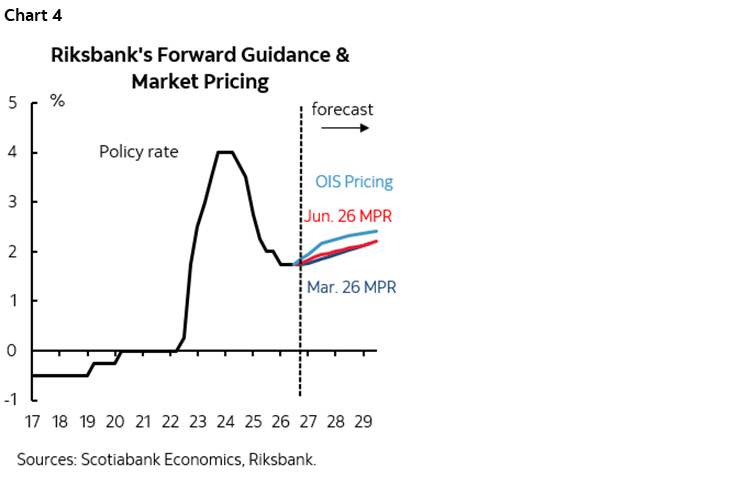

RIKSBANK GUIDANCE WARNS OF A COMING HIKE BUT MAY BE STALE

Sweden’s Riksbank left its policy rate unchanged at 1.75% as widely expected. Key, however, was that the explicit forward rate path provided by the bank was nearly identical to the path it prescribed back in March and which continues to rest below market pricing (chart 4). The central bank warned of a rate hike later this year, but also noted that its projections were set last week before news of a potential deal between the US and Iran to end hostilities. That last point could be why Sweden’s rates curve bull steepened with the 2-year yield down about 4bps on the day while the krona depreciated to the dollar and slightly underperformed other crosses.

BRAZIL’S CENTRAL BANK EXPECTED TO CUT

Brazil’s central bank is widely expected to deliver another 25bps rate cut down to a new Selic rate of 14.25% (5:30pmET). This would be the third cut since March after a prolonged period of restrictiveness. Expect guidance to be measured and data dependent as the effects of the inflation shock work through. Headline CPI climbed to 4.7% y/y in May with trimmed inflation performing identically. This is why markets foresee only a modest additional chance at easing thereafter.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.