ON DECK FOR TUESDAY, JUNE 16th

KEY POINTS:

- An optimistic, softening disinflation trade continues to sweep through markets

- The US lost the war and got stuck with the bill

- BoJ hikes, signals coming end to JGB purchase reductions

- Is this the turning point for Canadian housing as sales soar?

- RBA holds, has tough time convincing markets it could raise again

- China’s economy sputtered along last month

- Light US data on tap: weekly ADP, import/export prices, housing

- BCCh expected to hold

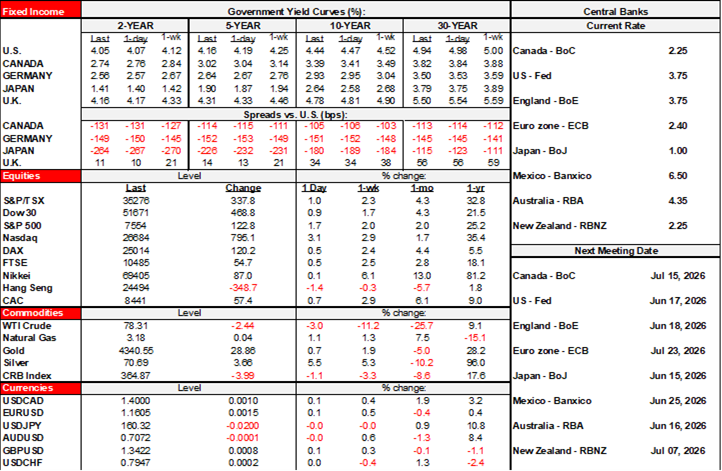

Disinflation remains in vogue across financial markets. Energy markets continue to believe that a durable peace has been achieved in the Middle East, as oil prices fall by another couple of bucks. WTI in the high US$70s now is well off the peak but still elevated from the mid-US$50bs at the start of the year and before war broke out. Sovereign yields are down by about 2–4bps across major markets except for a JGB steepener move following the BoJ’s communications. Stocks are a little more guarded this morning with US futures flat to slightly higher across indices, TSX futures up by about ¼% and European cash markets up by ½% to 1¼%. Most major currencies are little changed versus the dollar.

KEEP TELLING YOURSELF IT’S NOT OBAMA’S DEAL

There remain conflicting signals on what the US and Iran agreed to depending upon which side and which source you listen to, and still no text. That’s likely deliberate as negotiations continue and Trump masks its content from the prying eyes of the hawks in Congress. Trump is trying to convince folks that his agreement that lifts sanctions and offers cash in exchange for nuclear commitments isn’t a rehash of Obama’s deal and then some, but with little success insofar as I’m concerned. Reports of a massive US$300 billion reconstruction package for Iran amount to a similar sum to what all of the allies pledged in support to Ukraine since Russia invaded for the second time in 2022. If the idea is a Marshall Plan for Iran, then someone forgot that the post-WWII plan followed the defeat of the axis powers and the eradication of their regimes. So, you were defeated, and then got stuck with the bill? In my opinion, Trump’s war—like his trade wars—achieved nothing and political expediency ahead of the November 7th midterms drove him toward settling for basically the deal signed in July 2015—the Joint Comprehensive Plan of Action (JCPOA)—that he spent so much time attacking Obama over, plus cash.

BOJ HIKES, SIGNALS COMING END TO JGB PURCHASE REDUCTIONS

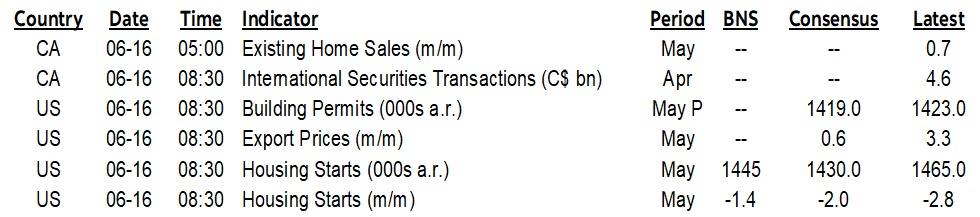

The Bank of Japan largely met expectations by hiking its policy rate by 25bps to 1% and indicating that reductions in its JGBs purchase plan would stop after next April. Markets reacted by driving a steeper JGB yield curve as 2s were unchanged but the 10s yield climbed by 6bps while the yen was little changed. Chart 1 shows the recent quarterly path for monthly JGB purchases and the planned quarterly path from 2026Q2 to next April that involves a ¥200B quarterly reduction until flatlining at ¥2 trillion per quarter starting next April. Those purchases have declined by almost two-thirds over roughly the past couple of years over which the yield on the 10-year JGB has risen by about 160bps. Neither decision was unanimous as the vote to hike was 7–1 and the vote to cease tapering JGB purchases after next April was also 7–1 with different dissenters on each decision. Forward rate guidance was highly dependent on the course of domestic data, developments in the Middle East and annual wage negotiations. Deputy Governor Uchida stood in for the hospitalized Governor Ueda. The BoJ is between forecast rounds and so new information and fresh forecasts next month may further inform the forward bias.

IS THE CANADIAN HOUSING MARKET TURNING?

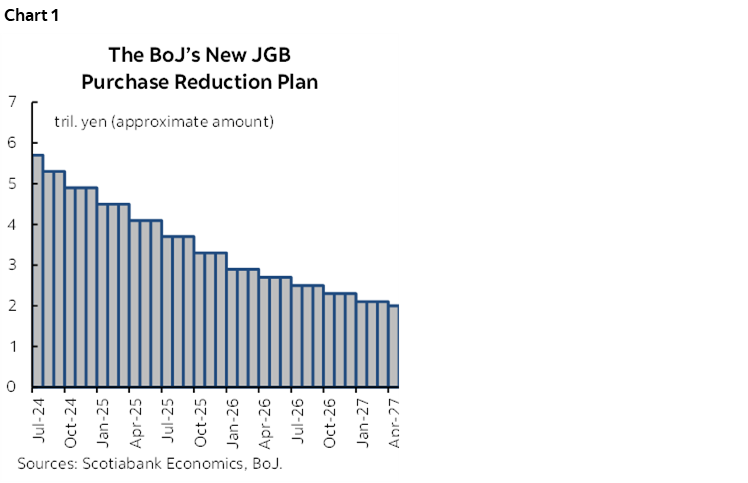

Could this be the long-heralded turning point in Canadian housing? Canada posted its biggest gain in existing home sales since October 2024 (chart 2). Sales were up by a seasonally adjusted 5.5% m/m in May. It’s only the second gain this year but follows a mild increase in April. New listings fell by 1% m/m, months supply fell by 0.3 to 4.8 months of inventory, and the national sales-to-new-listings ratio increased to by three percentage points to 49.2%.

RBA HOLDS, STRUGGLES TO CONVINCE MARKETS IT MAY NOT BE DONE

The RBA left its cash rate target unchanged at 4.35% as universally expected and priced. Governor Bullock said there was no consideration given to hiking at this meeting but sounded cautious on inflation risk by noting she still thought there were upside risks and that growth needs to slow with a higher unemployment rate in order to cool inflation. She refused to rule out further tightening and the statement guided a willingness to hike again if required. Australia’s bond yield curve was little affected and the A$ was little changed overnight. OIS markets are pricing a slim chance at a further hike later this year or early next year.

CHINA’S ECONOMY SPUTTERED LAST MONTH

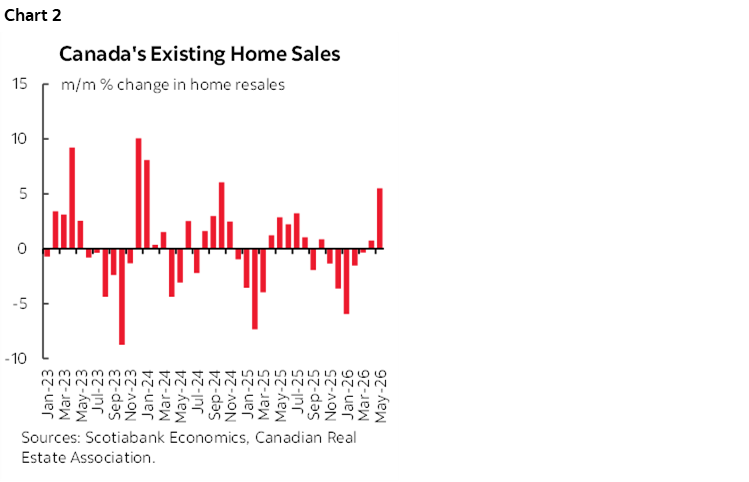

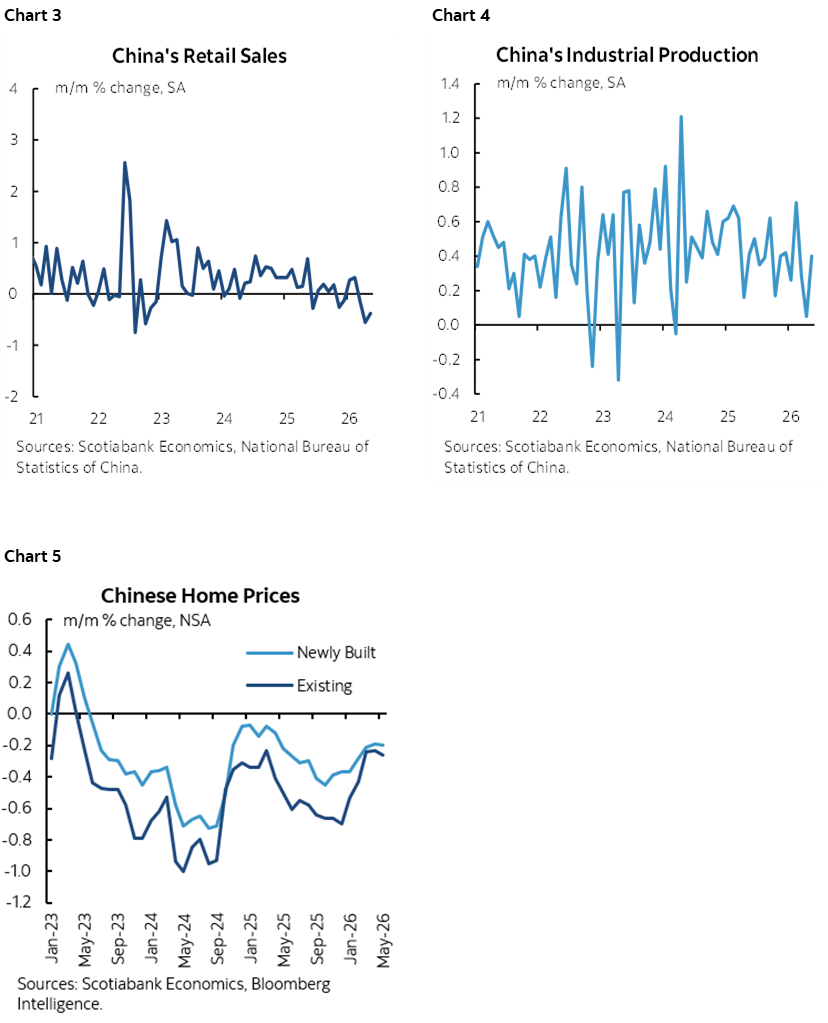

China’s economy sputtered along in May. Retail sales fell by -0.4% m/m SA for the third straight monthly decline (chart 3). Industrial output climbed by 0.4% m/m SA for the firmest gain since February (chart 4). The jobless rate ticked lower to 5.1%. Investment stumbled and is tracking a year-to-date drop of -4.1% with property investment down 16.2% ytd over the same period last year. Further, home prices continue their descent as new home prices fell by -0.2% m/m and resale prices were down by about 0.3% m/m. Resale prices have declined every month since May 2023 and new home prices since June of that year (chart 5).

LIGHT US DATA

Light US data is on tap including weekly ADP private payrolls on a 4-week moving average w/w basis (8:15amET). Import and export prices for May along with housing starts and permits are also due at 8:30amET.

CHILE’S CENTRAL BANK TO HOLD

Banco Central de Chile is widely expected to hold its policy overnight rate at 4.5% today (6pmET). Inflation at 3.9% y/y is mostly driven by commodities thus far, as core inflation is tamer at about 2.3%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.