ON DECK FOR MONDAY, JUNE 15th

KEY POINTS:

- Markets rejoice as the US and Iran strike an initial deal

- A US-Iran ‘deal’ sure sounds like Iran won…

- …while leaving plenty of uncertainty and risks intact

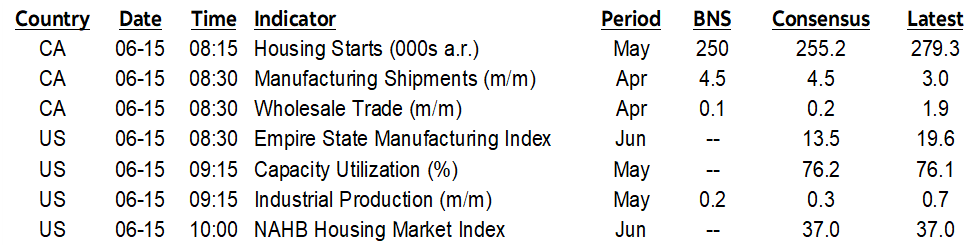

- Light Canadian, US data

- Global Week Ahead — Warsh’s Grand Entrance (here)

Is it genuine peace or are the market bots being overly gullible? I’ll fuss over this in a moment, but first is the good news to start your week.

The Everything Except Oil Rally

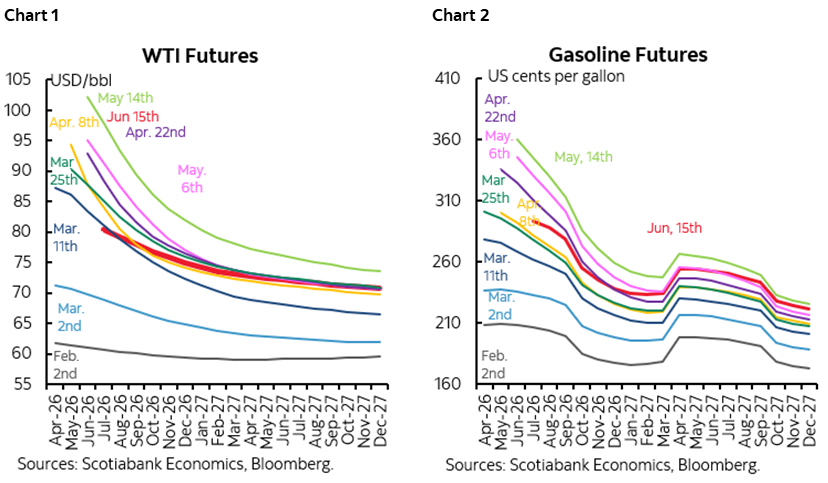

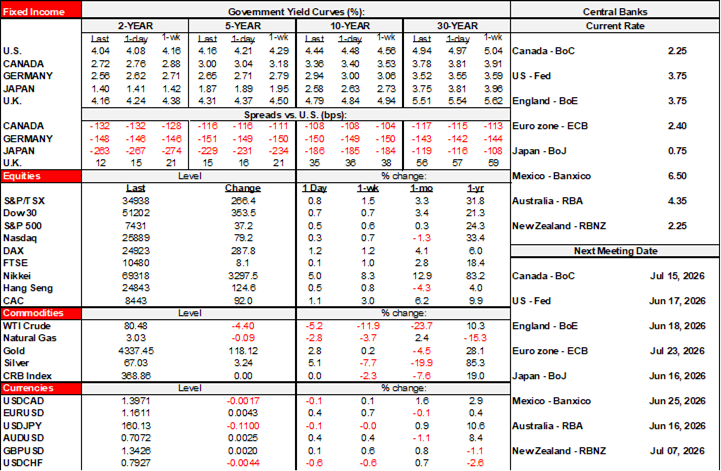

Oil is down by almost $5/barrel to the low $80s in WTI and Brent terms; the oil futures curve remains well above pre-war levels as a material shock remains intact amid ongoing vulnerabilities (chart 1). Ditto for gasoline futures into summer driving season, thin inventories and strained capacity across refineries. That’s driving a well-timed rally in sovereign bonds ahead of the week’s deluge of central banks especially the Fed, with most global benchmark yields down by about 2–7bps as curves mildly bull steepen. Stocks are broadly higher by ¾% to almost 2% across N.A. futures and around 1% across Europe except for London that is little changed with the Starmer administration stoking US trade tensions by (unwisely imo) following others with an under-16 social media ban. The dollar is broadly retreating as most major crosses appreciate albeit with mild underperformance by petro-crosses like CAD and NOK.

Reality Check

Now the reality check which is where you can stop reading in favour of moving onto some other fairy tale. Or read the G7 communique that lauded the agreement probably as a vain effort to appease Trump into two days of fruitless meetings starting today. The market driver is an alleged peace framework between the US and Iran that does have the advantage of getting oil flowing through the Strait of Hormuz at least for now. The problem is that I’m just not sure what else it achieves in a durable sense. I’m extra not sure about what the heck the point of the war was in light of so little having been accomplished.

Here’s what we know:

- we do not have any formal text. That is supposed to arrive by Friday in a formal signing in Switzerland if all goes well through negotiations in Qatar this week.

- A memorandum of understanding to reopen the Strait of Hormuz was struck which at least temporarily ends US and Iranian hostilities and embargoes. Reopening will take some time given the need to clear mines and make repairs to regional energy and port infrastructure. Iran’s Fars news agency has indicated that Iran plans to demand the right to impose levies on transits through the Strait after the 60-day period which means tensions over this matter will persist.

- The agreement will last for 60 days during which further negotiations are to continue. There is reportedly a provision to allow for this period to be extended if agreement on more complex matters cannot be reached which I’d put money on happening.

- Within that 60-day window it is expected that negotiations toward a grander agreement will be pursued. At stake are tying Iran’s compliance to anything that is agreed upon in terms of its stockpile of enriched uranium and its nuclear program to potential sanctions relief and freeing up Iran’s frozen assets. Iran also seeks to have all sanctions ended which would reach beyond Trump’s abilities and require the US Congress and its hawks to approve removals.

- Israel is clearly left out and not onside, which maintains risk of ongoing frictions with Hezbollah in Lebanon and with Iran itself. The ceasefire is supposed to include Israel and Hezbollah but colour me sceptical that either side will comply. Iran was reportedly preparing to attack Israel yesterday before the deal. Since this is a PG-rate note I won’t repeat Trump’s expletive riddled rant against Israel after Israel attacked Hezbollah in retaliation for a strike against Israel that almost scuttled the agreement yesterday and reportedly delayed it by several hours.

What Was the Point of All This?

Now, what on earth has been accomplished? Whippee, the Strait will reopen, for now, but what else? Iran will use this 60-day window to replenish their coffers, rearm and rebuild, potentially making it a bigger regional threat in future. Iran’s brutal regime remains in place. There is no agreement on its enriched uranium and nuclear program and Trump stated that failure to achieve agreement could restart US attacks. There is no word on the future of its ballistic missile program. It still has enormous stockpiles of missiles and drones. There is no guarantee that Iran would comply over time in any event, given its cheating history. Iran’s proxies remain functional. Israel views this as a half-baked truce. The US blew up a bunch of things, lots of people died, there was heavy damage inflicted on regional infrastructure across multiple countries, and relations between countries in the region are in tatters with more distrust across several of them than previously. Most damning of all is that none of the supposed reasons for entering into conflict were achieved.

In short, it’s hard to argue against an interpretation that posits Iran won the war. The US unquestionably has more military might, but would be wise to learn once more that this doesn’t assure victory when up against a foe like Iran and given no US appetite for a ground war. Trump’s desire for a deal is because he faces a scathing setback on November 7th. Trump faces the likelihood of having to craft an agreement that gives a great deal to Iran much like the past deals he has severely criticized. Let the American voting public cast their judgement.

Light N.A. Data on Tap

While it’s guaranteed to fade into the background given other developments, Canada and the US will update a few minor reports that will be particularly focused on the industrial space.

Canadian manufacturing shipments are expected to post strong growth of about 4½% m/m SA based on advance guidance from Statcan (8:30amET) but watch volumes as higher prices probably played a significant role in April. Canadian wholesale sales are expected to post a small rise with similar arguments (8:30amET). Canada also refreshes housing starts for May (8:15amET) that may pull back.

The US refreshes industrial output for May (9:15amET) that is forecast to post a small rise. The Empire manufacturing gauge of conditions around the NY Fed’s district will kickstart the latest monthly march to the next ISM-manufacturing report (8:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.