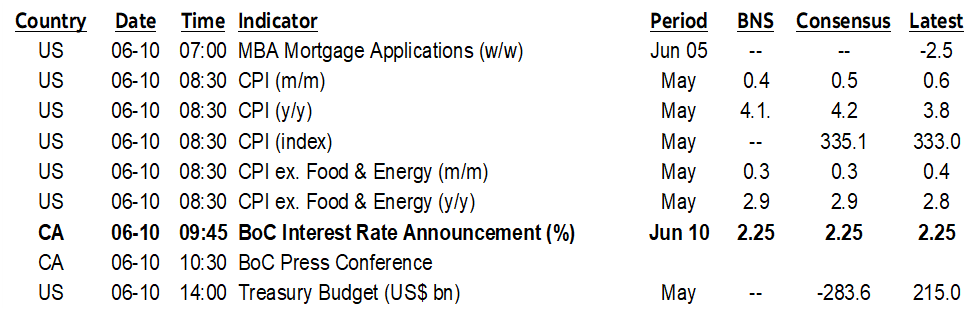

ON DECK FOR WEDNESDAY, JUNE 10th

KEY POINTS:

- Anxious bonds await US CPI

- Oil ignores US-Iran attacks

- US CPI: conflicting trimmed measures

- BoC — Keep it short and sweet

- Norges Bank hike pricing increased after CPI

- China’s CPI remained tame

- BoJ’s Ueda will skip next week’s meeting

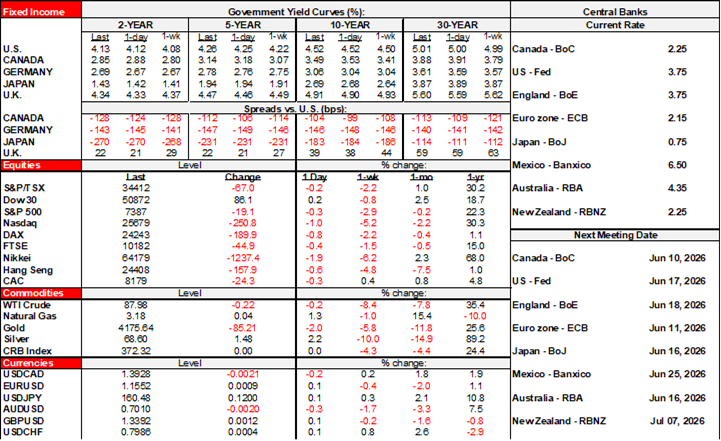

The week’s developments heat up quickly starting today with US CPI and the BoC ahead of the ECB tomorrow. There was little fuss over the US and Iran exchanging fire overnight as oil is basically flat. Sovereign bond yields are a touch antsy ahead of US CPI as evidenced by a mild cheapening bias across US Ts, gilts and EGBs. Equities are broadly in the red with losses of ¾% to over 1% in US futures, -½% in TSX futures and around –½% across European cash markets. The dollar is mixed as it’s losing ground to the won, CAD, and European crosses but up against the yen and Antipodeans.

The yen is stable despite reports that BoJ Governor Ueda has been hospitalized and will skip next week’s meeting but probably be there in July. Markets are priced for a hike next week.

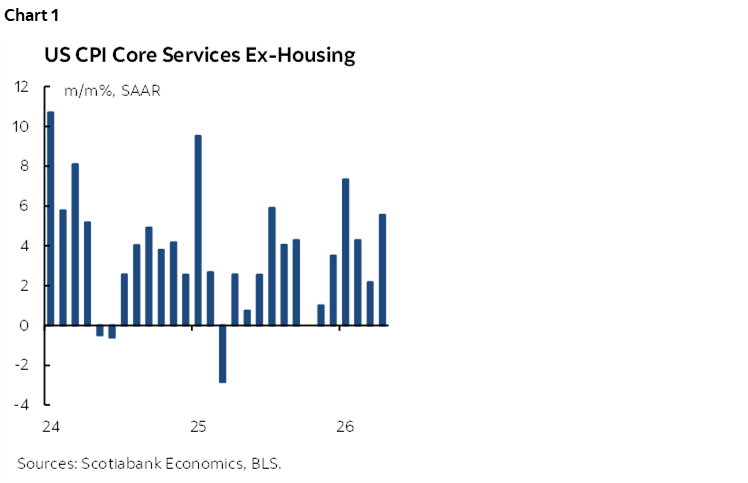

US CPI TO SET THE STAGE FOR WARSH’S ENTRY

Consensus expects core CPI to rise by 0.3% m/m which is also my estimate (8:30amET). Total CPI is expected to rise by 0.5% m/m (Scotia 0.4%). The results should lift y/y CPI inflation to over 4% with core approaching 3%. Key may be whether the cool core goods inflation in recent reports combines with some relief in core services inflation after the prior surge (chart 1).

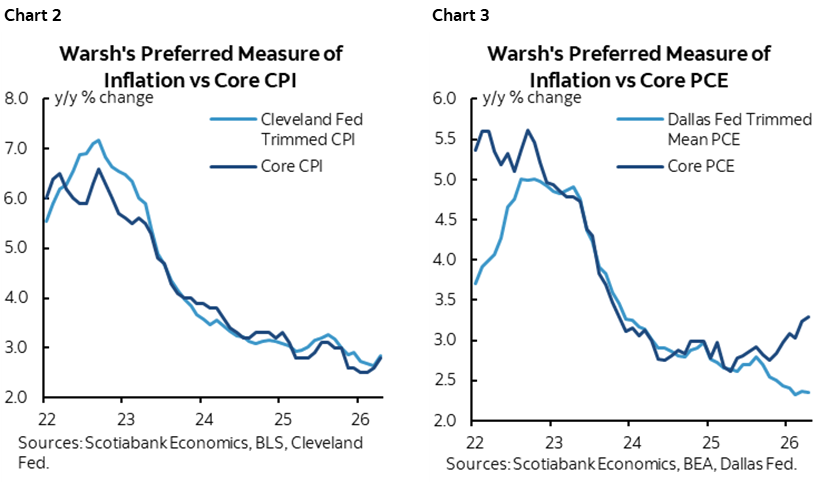

Then watch for the Cleveland Fed’s trimmed and median CPI soon afterward, given Warsh’s preference for central tendency measures. There has not been the spread between the core CPI and trimmed CPI measures (chart 2) that has arisen for core PCE versus trimmed PCE (chart 3). Warsh’s preference is toward trimmed PCE which arrives after core PCE inflation on June 25th.

A fuller CPI preview is in my weekly.

BANK OF CANADA — KEEP IT SHORT AND SWEET

No one expects the BoC to do anything this morning. The best advice is to issue a short statement and opening remarks by Governor Macklem (both at 9:45amET), hold a short presser (10:30amET), and say see ya next month with fresh forecasts at which point it will be see ya after summer in September. The BoC is monitoring all manner of developments that will take time and patience for now. See my weekly for a fuller preview.

PERU CONTINUES TO AWAIT ELECTION RESULTS

Our Peruvian clients and colleagues continue to monitor the ongoing election contest that may come down to overseas votes and a diaspora vote that may combine to overturn the slight lead by the left-wing candidate. The sol’s appreciation yesterday is banking on such a market friendly outcome as opposed to a turn to the left.

NORGES HIKE PRICING RAISED POST-CPI

Norway’s inflation was stronger than expected. Total CPI was up 0.2% m/m (0.1% consensus) and 3.1% y/y (3.1% consensus, 3.4% prior) but underlying CPI that excludes energy and taxes was up by 0.4% m/m (0.2% consensus) and 3.4% y/y (3.2% consensus). The krone is among the strongest crosses to the dollar this morning, while short-term yields climbed. Markets increased pricing for the chance of another rate hike after the 25bps increase on May 7th with about a one-in-four chance at the next week’s decision, 50–50 odds in August and a 25bps hike priced for September.

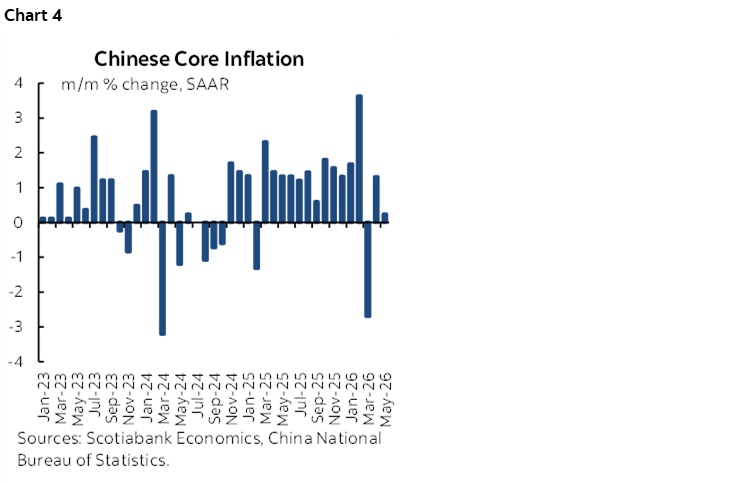

CHINA — MIRACULOUSLY NO INFLATION TO BE FOUND

It’s a miracle! Hallelujah! The world’s biggest importer of oil wants us to believe it’s the only country on the planet with no inflation in the aftermath of the war and its effects on broad commodity prices. If something’s too good to be true…

Anyway, China’s CPI inflation figures were a touch softer than expected in May. Total CPI was up 1.2% y/y with core CPI ex-food and energy up 1.1% y/y, both of which were a tick beneath consensus. Chart 4 shows the annualized m/m core inflation rates that have decelerated as the war erupted. Producer prices jumped 3.9% y/y (2.8% prior) in line with consensus but at about a four-year high.

So, one possibility is that firms are eating the input price surge in margins. Another is that they’re being told to by the state, particularly the SOEs. Another is that the data is made up. You pick.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.