ON DECK FOR MONDAY, JUNE 1st

KEY POINTS:

- Oil spikes as US-Iran war escalates

- Canada’s economy—why it’s not a recession…

- ...that would be patently irresponsible to call...

- …and the implications for the BoC

- Week ahead highlights

- Regular publishing resumes after travel

Regular publishing resumes after returning from a week of marketing in Asia; 7 flights including red eyes, 4 countries, almost two dozen meetings arranged by Scotia’s wonderful teams anchored out of Tokyo and Singapore. Over the years that I have known them they’re a great bunch of professionals and we had excellent discussions with markets clients in a region that plays a major role in driving appetite for financial products across Scotiabank’s core markets.

The fresh week is starting off in mixed fashion. Oil is up by about US$3/barrel in terms of WTI and Brent after the US and Iran exchanged blows and Israel continues to expand its war in Lebanon which makes a deal with Iran even less likely. Trump keeps talking about a deal that is simply not credible and sounds more like a vain attempt at controlling energy prices as Iran digs in against giving up uranium and control of the Strait. Iran remains aligned with the ‘managed irresolution’ strategy in a US election year during which the Trump administration has entered a conflict from which there doesn’t appear to be a credible exit.

Bonds are broadly cheaper with sovereign yields up by 2–5bps across maturities and markets. Stocks are mixed with N.A. futures clinging to small gains versus flat overall European cash markets. The dollar is broadly firmer, but mostly against lower-weighted crosses.

There were very light overnight developments other than war influences. There is some US data on tap for today including ISM-manufacturing (10amET) and construction spending (10amET).

What follows are my views on whether Canada is in recession, the BoC implications stemming from the GDP figures, and brief highlights of what’s on tap for the week ahead. Hectic travel and two blown weekends in transit mean I need time to come back with firmed up estimates for Friday’s US and Canadian jobs numbers.

CANADA’S ECONOMY—WHY IT’S NOT A RECESSION & BOC IMPLICATIONS

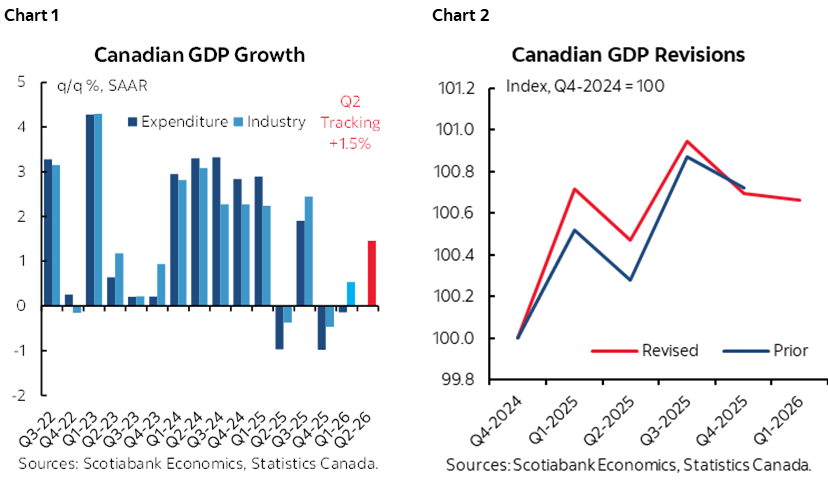

Friday’s GDP figures including revisions stunned everyone in consensus and at the BoC (charts 1, 2). I saw the figures after landing in Singapore while going through security and immigration in transit back to Canada. Consensus had forecast about 1½% q/q SAAR GDP growth with a trimmed range between about 1–2% and the BoC’s projection in the April MPR was 1½%. Instead, GDP was basically unchanged at -0.1% q/q SAAR. There were also negative revisions, such as Q4’s -1% q/q SAAR from -0.6%, but otherwise GDP was revised up over prior quarters yet GDP has contracted in three of the past four quarters.

Monthly GDP surprised a touch with a -0.1% m/m SA dip in March (consensus 0%, range 0–0.2%). April’s guidance pointed to 0.4% m/m SA growth. Monthly GDP landed at 0.5% q/q SAAR in Q1 versus the quarterly expenditure-based figure of -0.1%.

Clearly they’re not good figures but here’s why they don’t tick the recession box:

- Wimpcession: In the annals of recession talk there lie meaningful downturns. An annualized Q1 contraction of -0.1% q/q after a 1% drop in Q4 would be among the wimpiest recessions on record if we were to call it one. 1980Q2 and 1980Q3 were the closest rivals when GDP only contracted by about a quarter point in back-to-back fashion, then ripped higher for three quarters until a nasty recession truly set in over 1981H2 to 1982Q4.

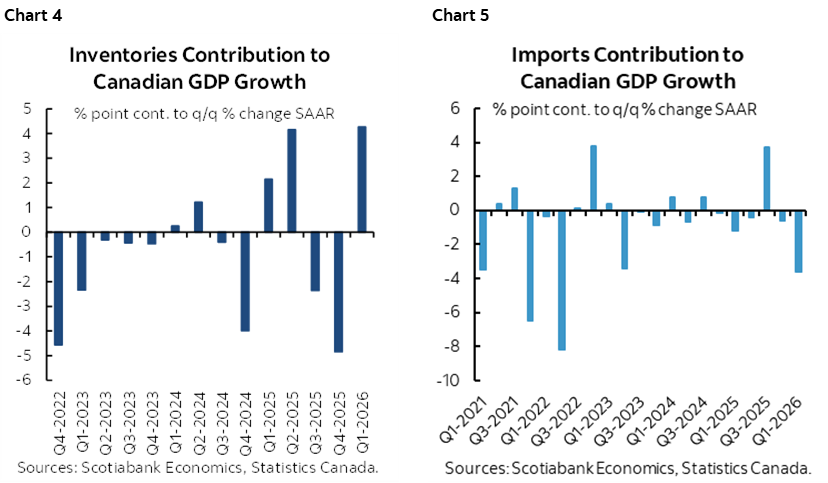

- Conflicting GDP accounts: Quarter-over-quarter expenditure-based GDP was –0.1% q/q SAAR but the monthly production-side GDP accounts posted a mild expansion of about 0.5% q/q SAAR after shrinking by the same amount in Q4. That flags inventory and trade drivers of the wedge between the accounts that distorted both quarters. In order to call a recession, I’d prefer to see both sets of accounts flashing red rather than calling it on inventories and imports.

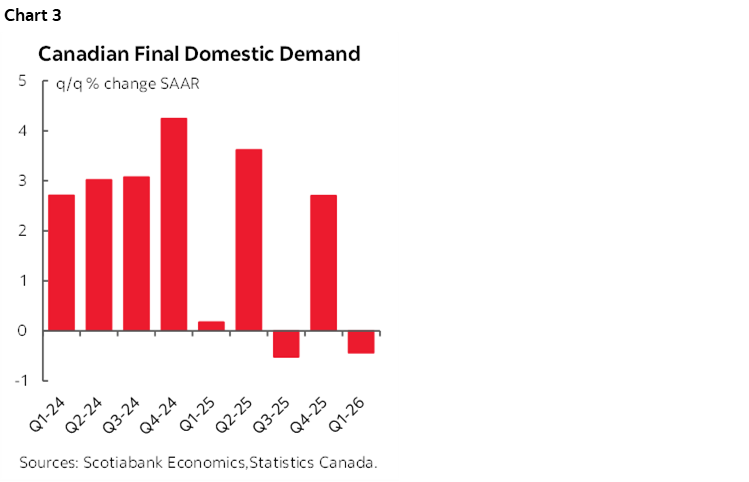

- Final domestic demand: The domestic economy contracted by -0.4% q/q SAAR after expanding by 2.7% in Q4 (chart 3). That’s not two consecutive quarterly declines in consumption, investment and government spending.

- Trade and inventory swings: Changes in these categories (charts 4, 5) reflect an ongoing cycle of wild amounts of order front-running followed by reversals due to Trump’s trade wars and the effects of Trump’s war with Iran. There are also important distortions I’ll touch upon in the next bullet point. Imports subtracted 3.6 ppts from Q1 GDP growth while inventories added 4.3% which reverses the prior quarter’s wild swings in both categories. This data is too volatile to merit ringing the alarm on the economy as companies are in a repeated cycle of trying to get ahead of expected price increases in the face of serial shocks, only to reverse the moves in subsequent periods.

- Gold: There’s gold in that recession call! Literally. Statcan flagged gold imports as being accountable for about half of the import drag effect on GDP growth in Q1. Excluding the affected categories, imports were up by less than half the reported pace in Q1. It would be irresponsible to make a recession call on the basis of surging gold imports that are idiosyncratic in nature versus reflective of underlying activity in the economy.

- Q2 tracking: It’s very tentative, but Q2 is tracking a rebound with 1½% q/q SAAR growth baked in thus far and based on Q1 and April while imposing no judgement on May and June for which we have very little data.

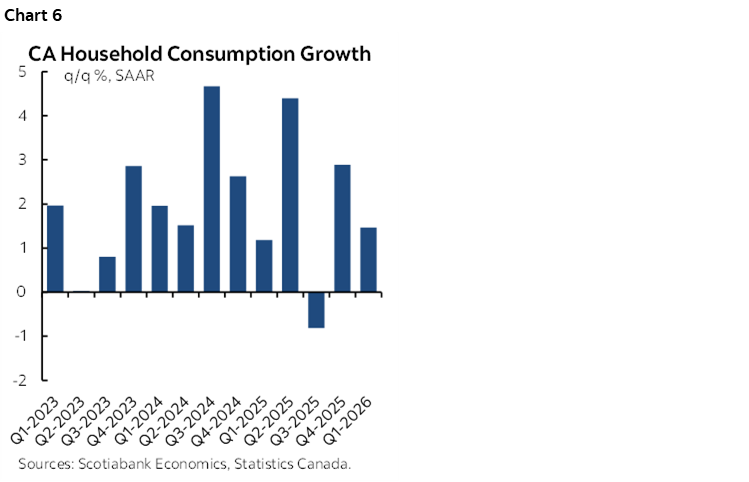

- Consumers: Consumer spending continues to expand with gains of 1½% q/q SAAR in Q1 after 2.9% growth in Q4 (chart 6). If there’s a recession, then someone forgot to tell consumers.

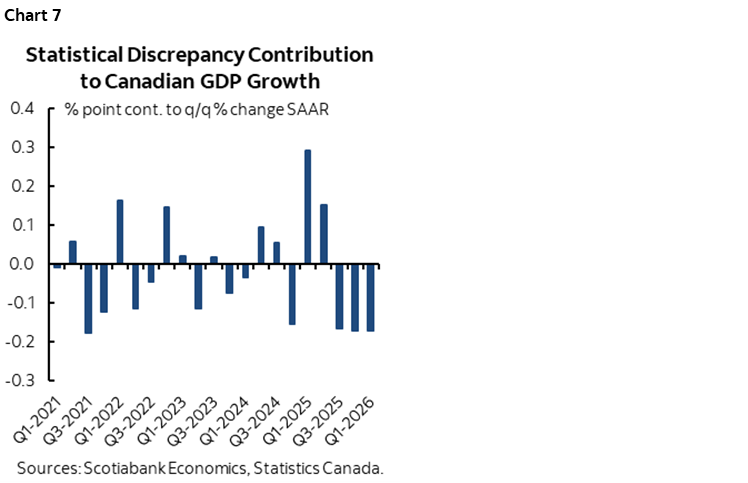

- Statistical discrepancy: This category knocked a weighted 0.2% q/q SAAR off of Q1 GDP growth. It’s the error term in the accounts. That was enough to make Q1 GDP barely negative and it has been unusually elevated for the past three quarters (chart 7). You wanna call recession on statistical error? Really??

- Other definitions: Normally you need an extended period of contraction in readings like jobs and industrial output to call a recession. We don’t have that at this point and there is a higher bar to calling recession on these readings than a handful of months.

- Unusual drivers: Even by Canadian standards, this was a horrible winter and a disappointing Spring. Heavy snow and cold may have dented economy activity and, if so, then coming out of hibernation could drive accelerations in categories like consumer spending and construction. We know that hours worked—a key GDP driver—were weak over recent months significantly due to adverse weather and sickness. Further, Canada is in the early days of falling population as the reversal of irresponsible mismanagement of immigration policy in prior years and it will take time for this required shock to work through the economy. I still expect that population shock to be a relatively subdued one—driven primarily by lower-impact temps—and relatively short-lived—since I believe it’s likely Canada will return to raising immigration targets within a couple of years after having curtailed the excess in categories like temporary foreign workers, international students and asylum seekers.

- Potential GDP: Most estimates of the Canadian economy’s potential GDP growth—the economy’s noninflationary speed limit—have moved lower over time toward the BoC’s 1.2% estimate for 2026. This reflects the negative population shock, trade tensions and productivity and investment challenges. If potential were much higher but actual GDP were shrinking then we’d have a bigger problem in terms of slack, but the economy’s nearer-term potential growth estimate itself has moved slower. I expect potential to pick up in future and we need to parse through the implications in our modelling of the demand and supply sides stemming from the GDP figures.

- Forward-looking developments: It would be rather unusual for a significantly commodity-dependent country like Canada to slip into recession in a widespread commodity boom. There are important lagging effects of the surge in commodities but normally it serves as a lagging positive effect on imported income through selling exports at more rapidly rising prices than paying for imports. The trickle-down effects on the overall economy are expected to be positive. Canada is also disbursing significant stimulus in June such as a sharp increase in GST rebates that may double q/q annualized disposable income growth.

Overall, while I have no problem calling recession if there is merit to doing so—like in the GFC when I led Scotiabank Economics to be the first Canadian shop to declare recession—I find it would be irresponsible to do so in this case and dwelling on a recession call risks causing one. We need to be careful toward the consequences. I wouldn’t want the Carney administration—along with the provinces—to spring the spigot and rain helicopter money down on households and businesses in reaction to these developments. The pressure to do so could perpetuate the past ten years of overly generous supports that delayed important adjustments in the economy toward other drivers and improved competitiveness. Be careful what you push the government toward doing versus the long-overdue need to extend the horizon of investment initiatives in the economy.

BOC IMPLICATIONS

Markets reacted to the readings by edging cumulative pricing for rate adjustments this year to just a 25bps hike by year-end with much of a hike starting to be priced in September and October BoC meetings. Markets foresee about 50bps of cumulative hikes into 2027.

We’ll issue a new global forecast update this week that refreshes our views across all major markets. The BoC will likely lean on the argument that GDP figures point to somewhat more slack than anticipated by them and everyone else as growth underperforms potential GDP growth that is likely around 1%. This will give them more room to assess forward-looking developments like the impact of the broadly based surge in commodities upon growth and inflation plus ongoing additions to fiscal policy contributions to growth.

I’m still of the view that the BoC hikes this year. We previously had Q3 tightening of 50bps and then +25bps in Q4 before stopping at 3%. I’d lean toward reversing that pattern with hikes no earlier than September into Q4. The BoC’s job is inflation control and that has a multitude of drivers.

Regardless, I’ll stand by our record versus consensus since we shifted to projected hikes by late 2026 in last November’s forecast while everyone else was talking cuts.

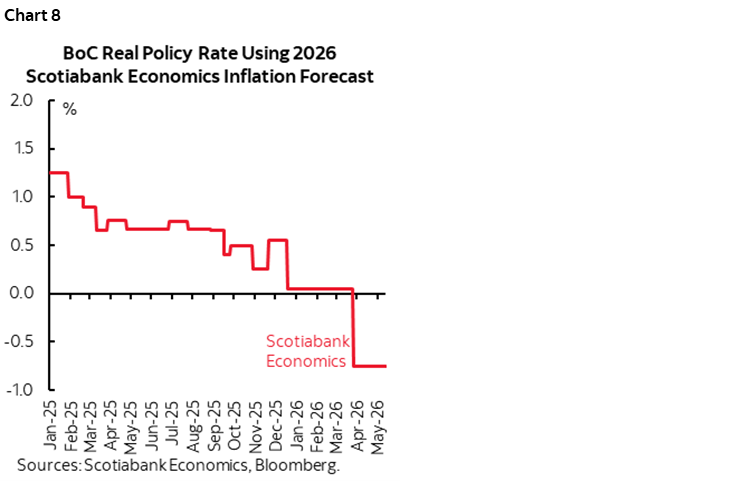

That begs the question, would they cut? They already have. Judging by the inflation-adjusted policy rate, the BoC has been passively taking out stimulus by looking through expected inflation resulting from pre-war and wartime influences on inflation risk. The real policy rate has dropped sharply (chart 8). It would be policy error to add to this by cutting the nominal policy rate. Every credible economist and macro model would say it’s the real policy rate that matters most.

WEEK AHEAD HIGHLIGHTS

I’m catching up after being away marketing for eight days and landing on Saturday evening so will have more to say about expectations in subsequent notes, but here’s a short outline of what’s on tap this week. Estimates have been submitted to polling groups for readings other than Canadian jobs and US nonfarm payrolls that I’ll share later.

- Canada: The focus will be upon Friday’s jobs report for May. Employment has fallen in three of the four months so far this year, albeit with several distortions along the way. Still, a Spring rebound would be nice! I’ll come back with estimates and arguments.

- US: We’ll get ISM-manufacturing for May (10amET) and construction spending in April (10amET) today. Tomorrow brings out JOLTS job openings in April plus vehicle sales in May. May’s ADP reading (Wednesday) will be followed by ISM-services during May plus factory orders in April and the Fed’s Beige Book of regional economic conditions. Thursday will bring out Challenge job cuts during May, and weekly claims. Friday is the big day with nonfarm payrolls and I’ll come back with estimates and arguments.

- Asia-Pacific: Australia updates Q1 GDP tomorrow night (ET). China refreshes private PMIs for May tomorrow night. The RBI is expected to hold at 5.25% on Friday just before Q1 GDP lands.

- Europe: The Eurozone CPI reading for May will arrive tomorrow morning with headline and core expected to accelerate after major countries released late last week. Sweden updates CPI on Thursday along with Switzerland. It’s a light line-up for the UK until next week.

- Latin America: Peru (today) and Colombia (Friday) will update CPI figures for May.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.