ON DECK FOR FRIDAY, JULY 17th

KEY POINTS:

- Equities continue to stumble on three main developments

- China’s AI swagger has western tech on the run…

- ...as the Epoch AI Capabilities Index gap may be narrowing

- Oil up as Iran war escalates with greater risks ahead...

- ...as the gasoline futures curve is at the highs, WTI futures closing in

- Trump’s silly election claims add concerns about retribution, confidence in November

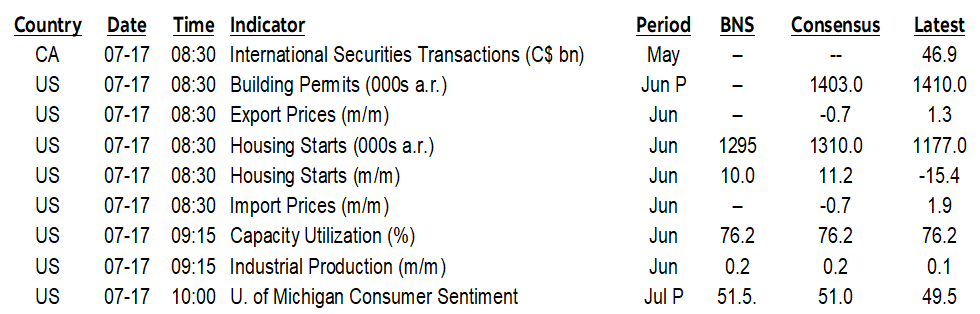

- US releases: UofM, starts, IP, terms of trade

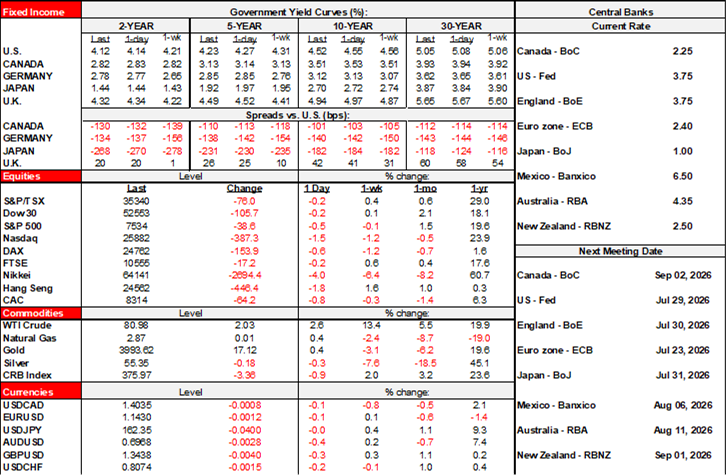

Stocks are ending the week on the back foot so far this morning. Asia-Pacific markets picked up where yesterday’s downdraft across US equities left off. The Kospi fell by another 6½%. Tokyo’s Nikkei 225 fell by 4%. Hong Kong fell by 1¾%. India’s Sensex was a rare winner with a gain of over 1%. European cash markets are down by up to ¾%. US equity futures are slipping by ¾% (S&P) to 1½% (Nasdaq). TSX futures are off by just ¼%.

Sovereign bonds are picking up some of the safe haven flows. US Treasury yields are down 2–4bps along with gilts and overnight moves in JGBs. EGBs are little changed. Canada’s curve is also rallying a touch with markets pricing 80% of a BoC hike by December. Some of the mixed sovereign bond performances can be attributed to higher oil prices that impact Europe more harshly than elsewhere; WTI and Brent are up by about 2% this morning.

The dollar isn’t really picking up safe haven effects itself which may reflect mixed idiosyncratic drivers of some crosses and perhaps a worthwhile reconsideration of past debates around the role of the dollar as a continued safe haven. CAD and NOK are outperforming on oil. The yen and euro are little changed. Crosses like sterling, the A$ and won are weakening the most.

As for drivers, there are three main factors worth flagging and a few others—like Starmer’s pending exit in the UK—worth monitoring. Each of them may have an element of risk du jour around them, meaning to be careful about going too far with sustainable market narratives.

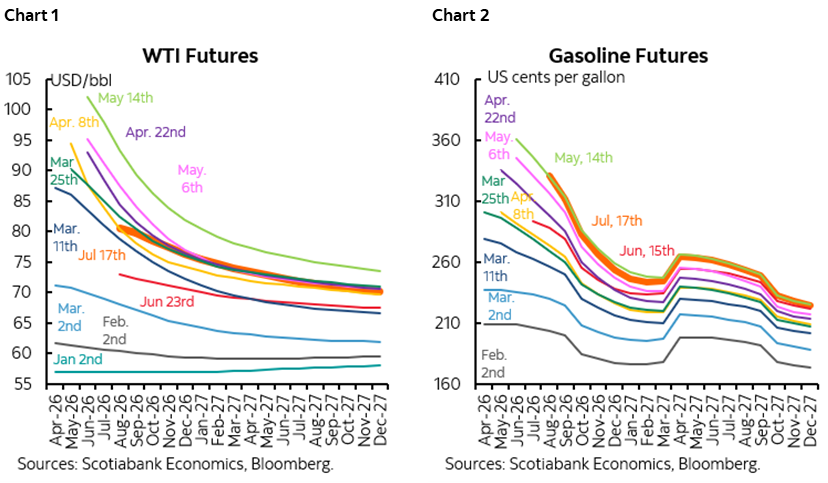

- Iran: Oil’s extra 2% gain reflects worsening attacks overnight ahead of Trump’s threatened escalation to begin bombing civilian targets next week. He has threatened this previously and backed down as debate about war crimes escalated. The catch-22 that emanates from a poorly contrived conflict that bypassed Congress and did not consult allies, let alone plan clear goals or an exit, is that Trump can’t let Iran win before his base (which so far, it has imo), but the affordability pressures stemming from escalation may doom the GOP in the midterms. Today’s WTI futures curve is creeping back toward prior highs especially further along the curve (chart 1) and gasoline futures are at their highs (chart 2).

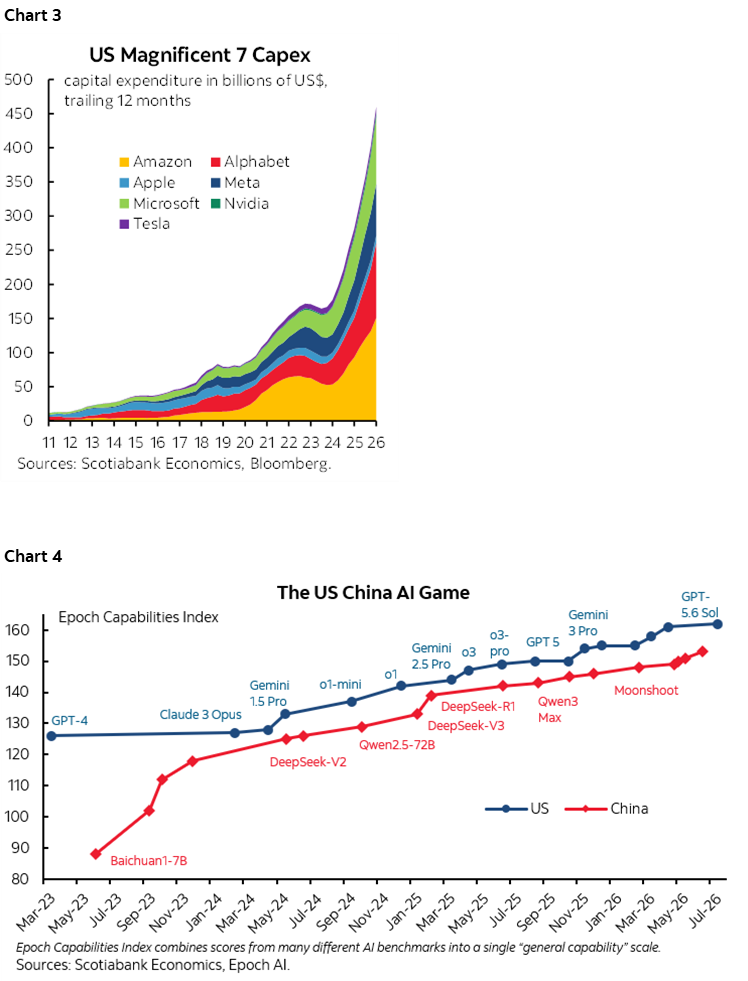

- China AI: A Chinese startup called Moonshot announced it had a new Kimi K3 model that it claims is on par with American AI offerings from OpenAI and Anthropic. It’s a replay of the prior market scare around China’s DeepSeek which markets ultimately shook off and which itself may be important guidance for today. Still, AI and AI-related stocks across the tech world are under negative pressure this morning. I liken the AI world to be like the embryonic stages of other industries, like autos 100+ years ago; some will survive and thrive, many won’t within overall excessive confidence in the sector as a whole. We’re likely to see a continued ping-pong match as firms jostle for the holy grail of AI supremacy. The massive surge in US AI spending is vulnerable if they get beaten (chart 3). The Epoch Capabilities Index has thus far been leaning toward American superiority (chart 4).

- Election confidence: Last evening’s speech by President Trump—if you could find a network willing to run it—lashed out at China for alleged voter interference among other claims, suggesting that US-China relations are about to take a renewed turn for the worse and how this could impact trade policy and other matters. Some fear Trump is paving the way for undermining US elections in November and what could ensue in the aftermath. In my view, Trump won 2016 with Comey’s help over Hillary’s emails, lost hands down in 2020 regardless of silly claims and parking lot antics, and won in 2024 due to serious dysfunction within the Democrats. There is one part of his electoral successes that have been reflective of true voter leanings and frustrations, one part a function of his masterful manipulation of facts and arguments, and another part owing to sheer luck. He clearly doesn’t see it that way, raising the specter of how he would treat potential defeat in November especially if the Dems take both chambers and raise impeachment risk.

Calendar-based risk is very light. There were no releases overnight. The US just updates a few relatively minor gauges this morning, the most consequential to markets being UofM consumer sentiment for July (10amET). Import and export prices during June will further inform the terms of trade facing the US economy (8:30amET), housing starts over the same month (8:30amET) and industrial production in June (9:15amET) are also on the docket. Starts should rebound, and utilities may crank up their contribution to total industrial production in order to drive a/c units across the country.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.