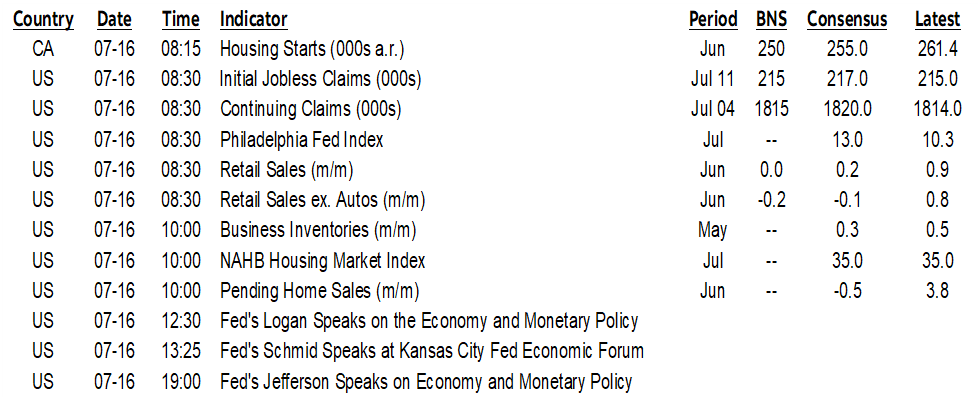

ON DECK FOR THURSDAY, JULY 16th

KEY POINTS:

- Stocks and bonds cheapen and this time it’s not because of oil and Iran

- BoK hikes with hawkish bias

- Mixed UK growth signals, dovish BoE talk drive sterling weaker

- US retail sales to inform Q2 consumer tracking

- US pending home sales, claims, Canadian housing starts due

- More Fed-speak: Logan, Schmid, Jefferson

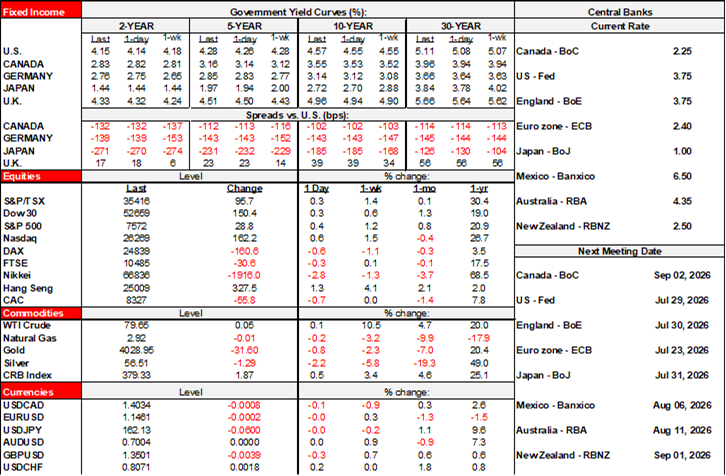

Bonds and stocks are starting the day in the red with minor losses and this time it’s not oil that’s the culprit as WTI and Brent are flat. Tech is leading some of the decline, but there is significant sector breadth to the equity softness. Sovereign bond yields are up by 1–2bps across US Ts, gilts, EGBs and JGBs. Stocks are off by up to ¾% across European cash markets and N.A. futures with indices across the Europe leading decliners. Currencies are little changed on balance with minor exceptions including a strong post-hike gain by the won to the dollar and a modest depreciation of pound sterling that probably had more to do with dovish BoE talk than data.

BoK Hikes with Hawkish Bias

Another central bank hiked its policy rate overnight. This time it was the Bank of Korea and it had an airtight case for raising its repo rate by 25bps to 2.75% in a unanimous vote. The bias was hawkish but noncommittal on timing a future hike as Governor Shin said “The next several policy meetings are all live. We’ll keep all options open and base our decisions on the incoming data.”

US Retail Sales to Inform Q2 Consumer Tracking

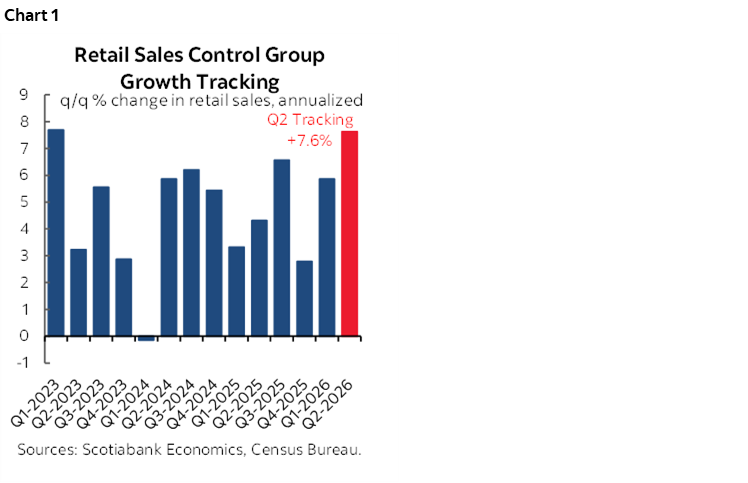

US retail sales during June will be refreshed at 8:30amET along with any revisions. The large prior gain in value terms of +0.9% m/m SA— of which half was in higher volumes—poses a sustainability challenge as does a dip in gasoline prices with somewhat of an offset from a mild gain in vehicle sales. Key will be the retail sales control group that excludes autos, gas, food and building materials and which speaks to core discretionary spending at retailers. The outcome will be used to inform how total consumer spending performed in Q2 with present tracking just under 2% q/q SAAR in volume terms. Retail sales in dollar terms are tracking about a 10% q/q SAAR gain in Q2 with the control group tracking a 7% gain (chart 1), but the volume of sales is tracking a 3% rise as higher prices dominate spending growth and probably at the expense of services spending.

More Post-Data Fed-Speak!

We’ll get more Fed-speak this morning from the likes of Dallas Fed President Logan (12:30pmET, voting, hawk), KC President Schmid (1:25pmET, nonvoting until 2028, hawk) and Governor Jefferson (7pmET, permanent voter). Yesterday’s remarks traded off what I interpreted to be patient remarks by NY Fed President Williams (permanent voter) against hawkish talk from Governor Cook who sounds ready to hike as soon as September in terms of her vote.

UK Economy, Dovish BoE-Speak Weigh on Sterling

The UK economy eked out modest growth in May that was led by services. GDP was up 0.1% m/m SA for a tick above consensus expectations. Services expanded by 0.3% m/m (0.1% consensus) with a mild upward revision. Construction output fell 0.8% m/m, industrial output fell 0.5% m/m, but manufacturing output stayed positive at 0.1% m/m. Trade was a winner, however, as exports grew by 2.8% m/m and were led by goods (7% m/m) but imports tumbled by 4.3% m/m entirely due to lower goods imports.

Bank of England Deputy Governor Breeden shared remarks this morning that have her sounding off against a hike in Bank Rate. She downplayed second-round effects of oil on inflation by flagging a soft economy and labour market slack: “Those two things mean that that shock is less likely to become embedded and lead to inflationary dynamics that we might need to lean against.”

Other minor stuff on tap includes Canadian housing starts in June (8:15amET), US weekly jobless claims (8:30amET) and US pending home sales during June (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.