ON DECK FOR WEDNESDAY, JULY 15th

KEY POINTS:

- Oil, earnings and central banks driving mixed markets

- BoC expected to stand pat

- Few things are more Canadian than labour strife impacting the BoC

- Recapping what Chair Warsh said in round 1 ahead of round 2 today

- China’s slowing economy

- US PPI to further inform PCE estimates

- Canadian home sales up again, other minor data on tap

- Earnings beating analysts’ expectations remains the safest bet in US markets

- Fed’s Cook to share her economic outlook

- Forest fires risk renewed turmoil across Canadian indicators

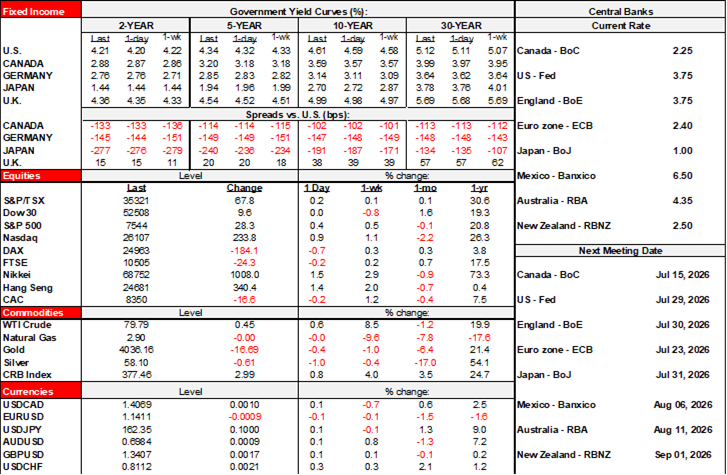

Oil, earnings and central banks are jostling with one another for the upper hand on market influences. Oil is winning with another small gain this morning. Sovereign bond yields are slightly higher again. Stocks are mixed with slightly firmer US equity futures, slightly lower TSX futures, and small losses across European markets. The dollar is mixed but mostly little changed. England-Argentina at 3pmET may be the day’s most watched development.

BANK OF CANADA—WHAT COULD BE MORE CANADIAN?

It’s a poignant reminder of pressures on its mandate that are emanating from labour market strife. I’m speaking in reference to the irony that the BoC will not be sharing its communications on an embargoed basis with media because of striking security guards and PSAC’s protests over replacement workers. How very Canadian, given the country’s one-third unionization rate.

As far as I’m concerned, this is a welcome development that could be habit forming. Too often, I find that the media interpretations by journalists are slanted, skewed, and often generally biased. Another example being a recent WSJ article on the BoC that falsely said no one expects the BoC to hike rates this year (we do!) while playing up dovish views in the article. Leave it to the street to make its judgements without select headlines driving the bots who are running markets these days. As always, I’ll cover it in real-time within chats for markets and management staff and clients.

The statement and Monetary Policy Report including fresh forecasts as well as Governor Macklem’s opening remarks will be released on its website at 9:45amET. The press conference has been delayed until 10:45amET—15 minutes later than usual—because of the same labour issue.

No policy changes are expected. Key may be refreshed forecasts. On guidance, Governor Macklem is commonly perceived as being dovish until a problem is staring him squarely ahead, so I expect little from the communications beyond wishing everyone a good summer and see you at the next decision in September. A full preview was available in my weekly which I won’t repeat at this late stage.

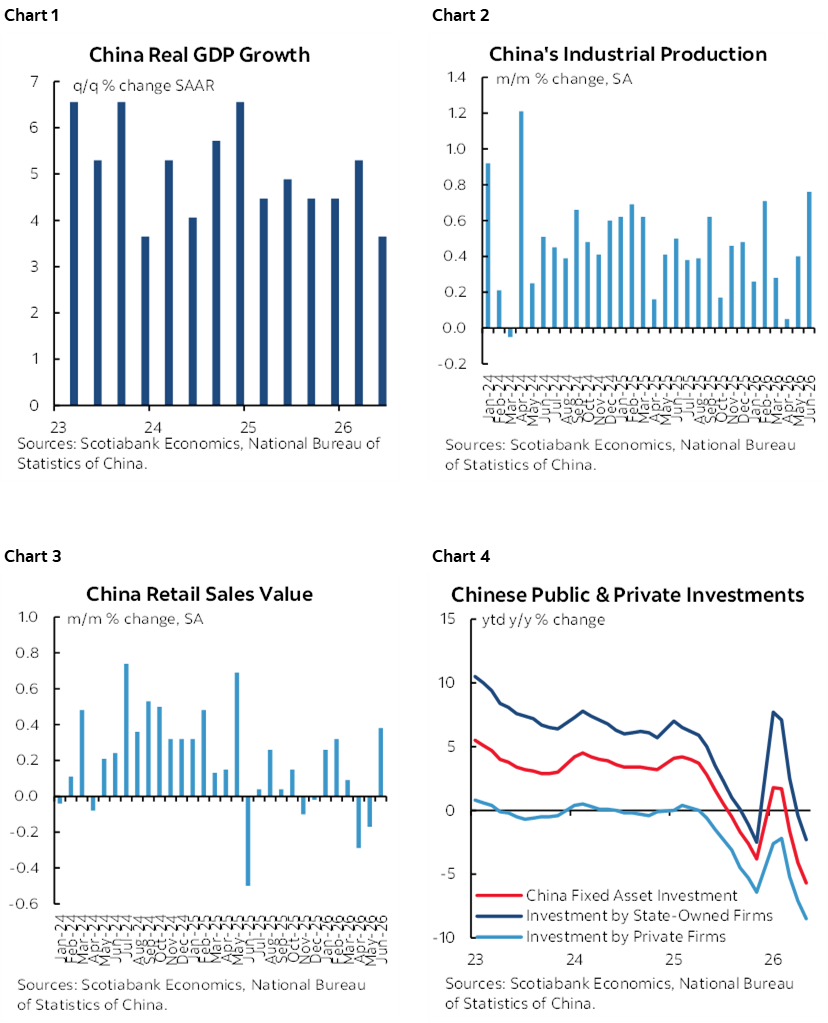

CHINA’S SLOWING GROWTH

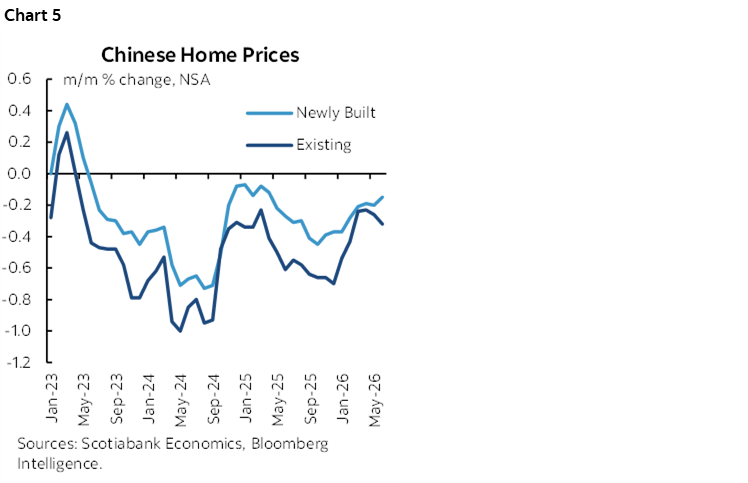

Overnight China data is shown in charts 1–5. China’s economy met expectations for slower GDP growth in Q2 (0.9% q/q SA nonannualized) but ended the quarter on a high note based on higher frequency readings. In year-over-year terms, GDP was two-ticks beneath consensus at 4.3% (5% prior) which extended the slowdown. Industrial output volumes in June grew by 5.3% y/y (4.6% consensus, 4.5% prior) and the value of retail sales also beat, rising by 1% y/y in June (-0.1% consensus, -0.6% prior). Property investment fared worse, however, and shrunk by -18% y/y ytd. Further, house prices continue to fall with new home prices down by -0.15% m/m and resales down by -0.3%—both extending the declines since mid-2023.

CANADIAN RELEASES—HOME SALES, MANUFACTURING, WHOLESALE, BRIDGEGATE

Canada’s housing market sprung back to life over the key Spring market. After a large 5.5% m/m SA rise in May, existing home sales might have been expected to retrench in June but they posted a mild 0.5% m/m SA gain. That makes it three consecutive monthly gains over April through June which is consistent with prior guidance that we could see a rebound. CREA reports that new listings fell 1.3% m/m and total months supply was unchanged at 4.8 while the sales-to-new-listings ratio increased to 50.2% (49.3% prior), signalling a tighter housing market in generally balanced supply and demand territory.

Canada will also refresh minor data on the value of manufacturing sales (1% m/m expected) but watch volumes stripped of price effects, plus wholesale sales, also for May, that are expected to slip in dollar terms and probably more in terms of volumes.

And on this, I’d repeat my first reaction—show us the deal. I want to know if the Moroun family was paid off one way or another because if so, Canada is feeding foreign corruption which is against the framework of rules and regulations that apply to businesses.

Lastly, extreme heat and storms are lighting up forest fire risk again this year with smoke blowing in from northern Ontario into Toronto today. Ontario’s fire map is lit up. Keep an eye on this across the country for disruptive effects on affected sectors like agriculture, energy and mining, tourism etc.

US—EARNINGS, PPI, FED-SPEAK

US earnings releases continue. We’ve already heard from BlackRock that beat (EPS US$13.91, consensus $12.66). Morgan Stanley also beat EPS expectations. Earnings are generally beating analysts’ expectations yet again (chart 6) either because they’re not very good, or because they have tended to do ever since SOX and other pieces of legislation made analysts more risk averse (chart 7).

This morning’s producer prices for June will help us firm up estimates for PCE and core PCE inflation due at the end of the month post-FOMC. Total prices are expected to be soft after the price large gain, with core prices ex-food and energy expected to post another modest gain. Key will be the categories that are included in PCE which may struggle to post another rise given large prior gains in airline passenger services and portfolio management fees.

Minor releases will include the Empire manufacturing gauge that kicks off a monthly round of regional reports on the path to the next ISM-manufacturing print (8:30amET) plus the Fed’s Beige Book of regional economic conditions (2pmET).

And no doubt Trump is eagerly awaiting Fed Governor Cook’s speech on the economic outlook at 1pmET. My hope is that it’s more sensible than Waller’s on Monday and that she holds no punches with an objective, lucid and cogent take on the outlook while under farcical pressure from the administration.

WHAT WE LEARNED FROM KEVIN WARSH’S TESTIMONY

Fed Chair Warsh conducts round 2 of the semi-annual testimony on monetary policy before Congress this time before the Senate Banking Committee at 10amET.

What did we learn from his testimony yesterday? The short answer is not terribly much beyond a Chair that genuinely sounds like he wishes to wait for the five task forces he set up to begin reporting back before having a framework of thinking that would lend confidence to acting. I still think that merits receiving OIS on nearer-dated contracts and then we’ll see.

Here are a few other takeaways along with my thoughts.

On Which Part of the Dual Mandate Concerns Him the Most

Warsh said "The labour market has been pretty much in balance, we've got some work to do on the inflation front." That sounded hawkish but in what form and how contestable his remark may be are worth exploring.

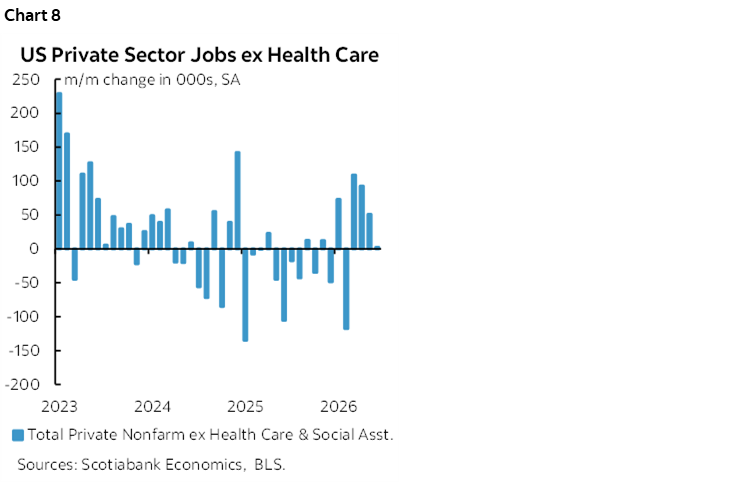

The first part is debatable imo. Job growth has slowed. The unemployment rate is stable as he frequently noted, but the household survey's jobs have fallen by 1.567 million since Inauguration Day and this has been offset by a 1.338 million drop in the HH survey's measure of the labour force. Further, private nonfarm payrolls excluding the health sector that marches to the beat of its own drummer has hardly been stable (chart 8). Weak job growth offset by crushing immigration policy and folks leaving the workforce is not a good sign for the US job market. Plus, real wages are weak and so has inflation-adjusted personal disposable income that has not grown for several quarters.

And on the second part of what he said about inflation, it's unclear if he's talking about addressing it with communication tools, maintaining the current slightly restrictive stance for longer, or hiking.

On Core Inflation Risks and Measures

When asked if he would respond to evidence that the Iran war’s effects on energy prices is spilling into core inflation, Warsh responded in the affirmative. As he perhaps should have. Except for a few reasons why not.

Like how so far, there is little pass through. Core PCE has averaged 0.3% m/m SA over the past three months during the war and pending June which may weaken toward the end of the month. PCE has a much lower weight on shelter. Core CPI has averaged 0.2% m/m SA over the past five months. Trimmed mean CPI was flat at 0% m/m SA last month with weighted median CPI up by just 0.2% m/m SA; I suspect that when we get trimmed mean PCE after PCE at month’s end that it will fall to a new 3-month rolling average just above 2% y/y.

The intimation is that what is being experienced today is more of a relative price shock than generalized inflation outburst with the Fed at risk of misinterpreting inflationary pressures in opposite fashion to how it did so when it misjudged breadth of pressures in the pandemic. Going forward, I believe a real wage squeeze after basically no real PDI growth for several quarters will sharply limit pass through. The supply side is not going through as widespread shocks this time. There isn't a clear demand surge either. If anything, the supply side may be expanding via AI.

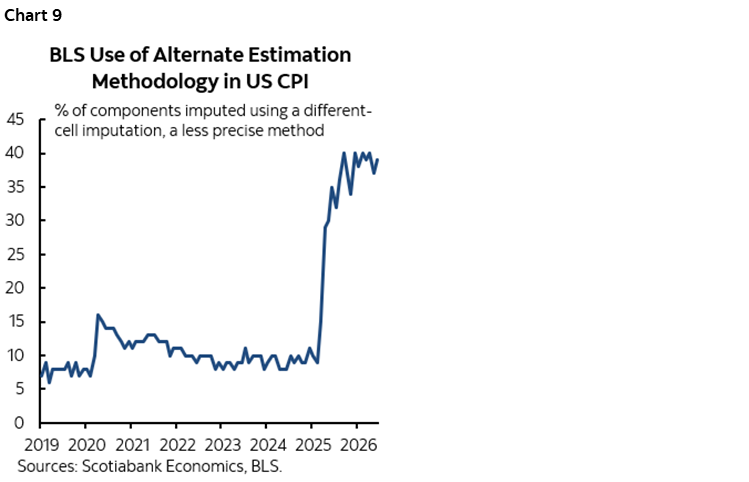

Further, during his testimony, the BLS released the share of the CPI basket that is estimated by proxy methods in the absence of real price data due to budget cuts and the failure to pivot toward new collection methods. The made-up share of the CPI basket is 39% and still very high (chart 9). The Fed is looking at poor quality data which is among the reasons why Governor Waller’s stance on Monday that hinged the July decision upon June CPI was so misguided.

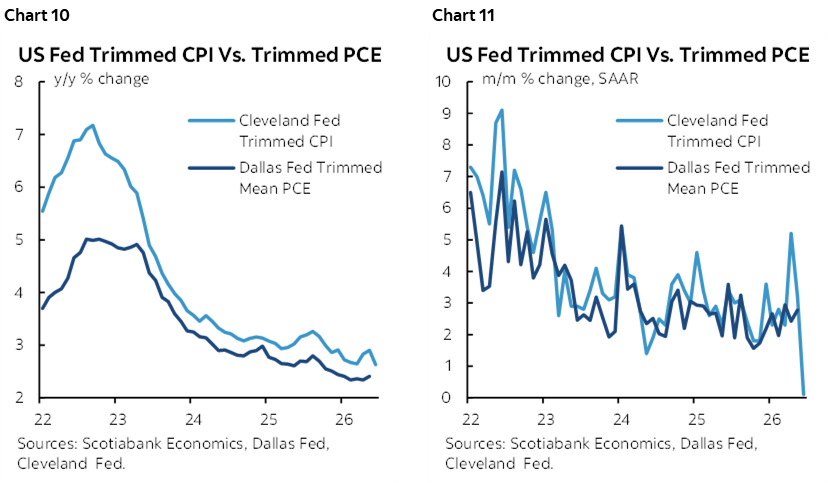

As a sidebar, note that trimmed mean CPI overstates trimmed mean PCE and the latter is likely to move lower at month-end (chart 10). And in m/m SAAR terms, TM PCE may see the bottom fall right out by month end (chart 11).

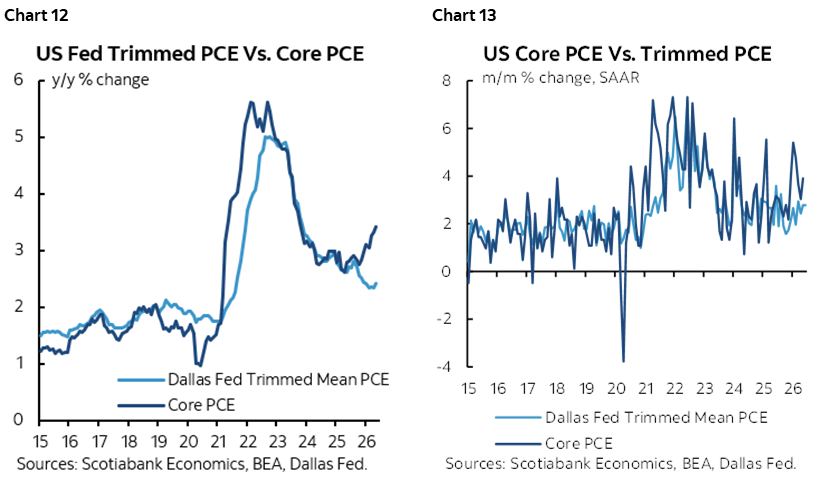

And charts 12-13 address whether core PCE turns up before TM PCE. On y/y comparisons, you'd be cherry-picking the sample to conclude as much. Sometimes core PCE turns higher before TM PCE, sometimes it doesn't. On m/m SAAR, the noisy pattern shows at best an asymmetric one-off cherry-picking bias drawn from the very different conditions of the pandemic but nothing clear by way of leading or lagging relationships between the measures over time.

A complicating issue is that Warsh said during his testimony that he does not have a preferred measure of inflation, whether trimmed mean or whatever, and that a recent WSJ story about his preference for trimmed mean PCE was false. He went on to say that the Fed needs new measures to understand underlying inflation and that none of the current measures capture this. Ok, like what kind of measure? It’s disturbing to hear the Fed Chair basically say that he doesn’t know what’s going on with inflation and therefore cannot judge one-half of his mandate while curiously sounding so confident about past inflation using the same metrics he disparages.

Let’s remind Mr. Warsh about what he has said on the issue in the past, like during his Senate confirmation testimony:

"The measures I prefer are looking at things that are called trimmed averages, where we take out all of the tail risks, all of the one-off items, and we ask ourselves whether the generalized change in prices is having second order effects on the economy. Again, they're not where they should be, but I think that the trend is quite favorable."

Contrast this to yesterday when he said he has no preferred measure of inflation. We have Kevin Warsh when seeking the approval of a dovish President while trying to get the job, versus Kevin Warsh the politician after he got the job.

This is a huge issue. I'm unsure about what he really thinks about the issue now. One possibility is that he is simply deferring to task force #5 that is charged with coming up with views on the inflation framework and the overlap with task force #3 that is looking at improving data sources. He doesn't wish to be perceived as guiding the outcome but may very well not have changed his personal view. Another possibility is that he has changed his mind upon consultation with others. The other possibility is that he wouldn’t be the first person I’ve seen to over-promise what he can do in order to get the job. We'll see how it all winds up.

Sloppy Commingling of Price Levels Versus Inflation

One issue I continue to find confusing about Warsh’s communications is when he mixes price level and inflation references in jumbled fashion. For instance, he said “my job is to take sticky prices and unstick them" as Warsh emphasized price levels again. He has repeatedly emphasized—and did so again yesterday—the five-year overshooting of the Fed’s inflation target and said he intends to fix that.

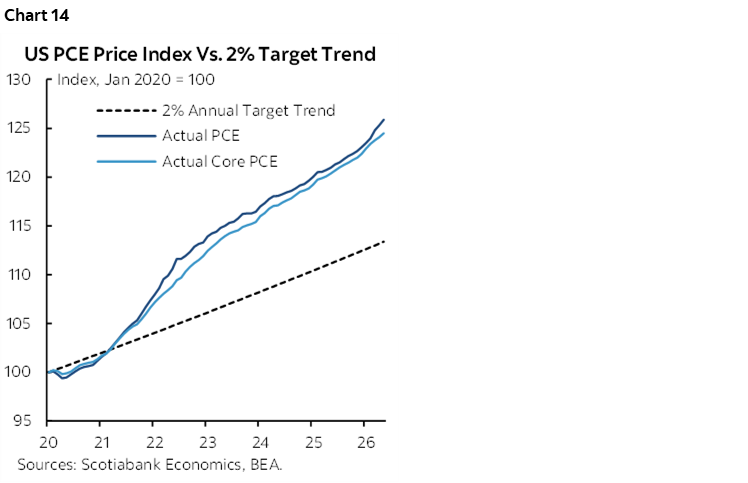

The Fed can't address and shouldn't address price levels. Chart 14 shows that the PCE price level is about 25%+ above a trend line set by achieving the 2% target each year and the core PCE price level is similar. I don't think Warsh is signalling a bias toward this, but his language is sloppy at times and when he talks about five years of overshooting being a problem he sounds like he has a retroactive policy bias that has waved the white flag on ever trying to forecast anything ever again.

The BoC went through all of this assessment of alternative regimes in a prior 5-year agreement renewal with the government. They rejected price-level targeting on multiple grounds. One issue is where do you start the trend which can be highly arbitrary. The other being the extraordinary damage you'd have to do to bring the level down to the trend. Bygones be bygones in a forward-looking sense on the 2% inflation target was the BoC’s default and I think that makes sense. Warsh says he is not trying to litigate the past, but he needs to choose his words more carefully and emphasize the future more than the past in his remarks

AI Uncertainty Merits Market Caution Pricing the Fed

On AI I found his comments to be more insightful. He said "This is a supply shock we are seeing in the US. We are seeing the capability growing at exponential rates, like a hyper Moore's Law. What are the consequences of this positive technology shock? I've asked 2–3 experts for their views over the next 3–6 months." He noted this is by far the biggest technology shock in his career. That may be understating it in my opinion.

The first takeaway on that comment is that 3–6 months reinforces his patience and leans against pricing any Fed action in the near-term OIS contracts. I think he means it when he says don't pre-judge the task forces despite markets that are pre-judging them.

Warsh was basically saying that he thinks a productivity boom lies ahead but can't say it with great confidence yet and wants to hear from the task force on the matter.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.