ON DECK FOR TUESDAY, JULY 14th

KEY POINTS:

- Iran and oil loom large over a big day for US markets

- Why you shouldn’t read much into Governor Waller’s latest guidance

- US bank earnings broadly beat expectations, share price reactions mixed

- US CPI takes on elevated significance

- Fed’s Warsh begins two days of testimony

- China’s exports soar

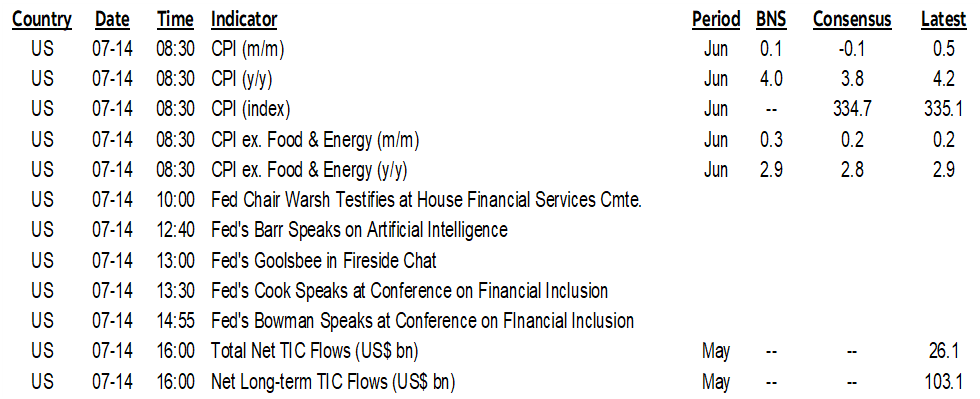

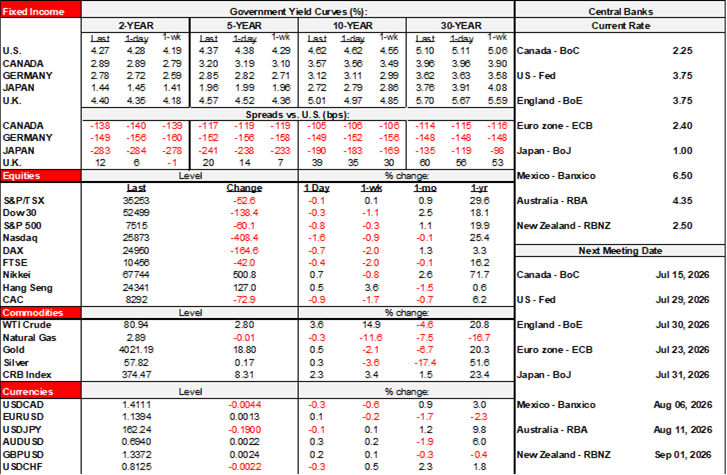

It’s the biggest day of the week for US market watchers, although the escalating conflict between the US and Iran is complicating the potential market reactions. Oil is up by another $3–4/barrel of WTI and Brent with both prices now into the $80s, taking the cumulative rise by WTI since the reescalation to about $12 for WTI and almost $15 for Brent. The whole futures curve continues to pivot higher (chart 1).

The knock-on effects are carrying yields on gilts and EGBs higher in bear flattener fashion as 2s cheapen by between 4–7bps. US Treasury yields are largely shaking it off as they focus upon this morning’s developments. The BoC is now fully priced for a December hike, although it’s largely a byproduct of a tight, lazy trading correlation between WTI futures and OIS pricing that implies there is nothing else you need to know other than oil. Stocks are under pressure everywhere. The dollar is losing ground against most majors, especially the commodity crosses like the Antipodeans, A$, CAD Krona etc.

US CPI — OVERSTATED SIGNIFICANCE

US CPI inflation for June arrives this morning with a bit more potentially at stake in terms of market reactions given Governor Waller’s speech yesterday (see below). Consensus lies between -0.3% m/m SA and +0.3% but with most estimates in the -0.1% and -0.2% buckets. Yet what matters is core CPI with most estimates in the 0.2% to 0.3% m/m SA buckets including Scotia’s 0.3%. A full preview of expectations was offered in my weekly including the caution about looking at super-supercore services inflation that would not only remove housing and energy services (supercore) but also World Cup related categories like airfare, lodging etc (super-supercore).

This highlights another issue with Governor Waller’s guidance about the importance of today’s reading—he would hike potentially on World Cup and other short-term influences. For instance, what if higher commodity prices squeeze real incomes and leave them with less to spend on other things in more broadly disinflationary outcomes?

CHAIR WARSH’S FIRST OF TWO DAYS OF TESTIMONY

How do you give forward guidance while sticking to your mantra of not believing in forward guidance? Walking this fine line may be challenging to Chair Warsh as he takes the hot seat before the House Financial Services Committee at 10amET. A lot of the banter will be political and stray from the Fed’s prime responsibilities, but key may be his reaction to CPI, whether his stance is similar to Governor Waller’s and how he views fresh risks to the dual mandate as energy and other commodity prices creep high again.

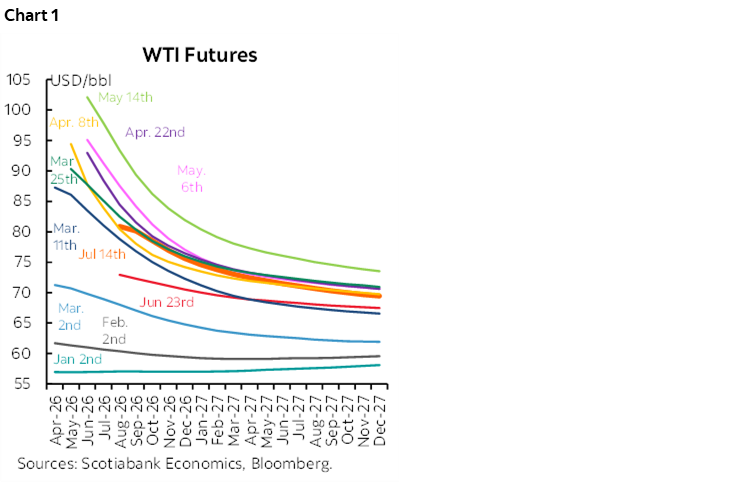

SOLID START TO US EARNINGS SEASON

The Q2 earnings season begins in earnest this morning with a wave of key US financials releasing (chart 2). Goldman Sachs, Bank of America, Wells Fargo, JP Morgan and Citigroup are all releasing into the pre-market. Results so far are very strong from each of them with Goldman and Citi pending at the point of publication.

CHINA’S EXPORTS SOAR

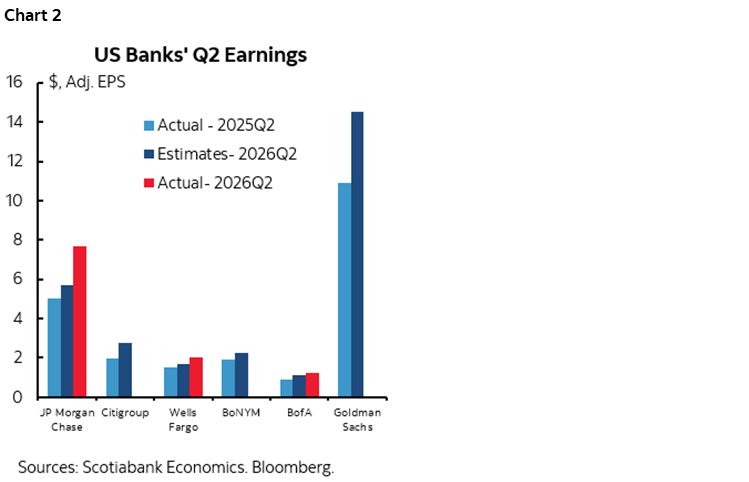

China’s exports soared last month. They were up by 27% y/y (19% consensus) is USD terms with imports also smashing expectations at +36% y/y (26% consensus). In yuan terms, exports were up 20.8% y/y with imports up 29.4%. China’s trade account continues to flourish and its surplus with the US may have bottomed (charts 3–5). Car exports sharply accelerated; they were everywhere when I was in Asia a couple of months ago and making large gains. Everything electric was higher.

HOW SERIOUSLY SHOULD WE TAKE GOVERNOR WALLER’S SUDDEN HAWKISHNESS?

There were a lot of issues with Fed Governor Waller’s speech yesterday in which he warned of the potential for imminent rate hikes, but one immediate caution is that he has a proclivity toward being too early, too misleading in terms of the FOMC consensus and frankly a tad erratic.

For example, in November 2023, he said that if inflation keeps falling “for several more months, three months, four months, five months, we could start lowering the policy rate just because inflation is lower. It is consistent with every policy rule. There is no reason to say we will keep it really high.” The FOMC did not begin cutting until 10 months later.

Or take last summer when Waller—who previously held hawkish views—turned toward being among the most dovish FOMC members and at a time when he was on Trump’s short list to be Fed Chair.

Or take this past January when he dissented against his colleagues and issued this statement explaining why he felt that the Fed wasn’t cutting enough. He said the labour market was weak, the Fed should look through some of the pressures on inflation as long as expectations are anchored, and said he favoured cutting toward 3% instead of 3.75% where the policy rate has since stood. Now he wants to hike.

In more substantive fashion, I find his guidance that a warm CPI reading this morning would prompt him to likely support a hike this month to be a tad absurd. There is nothing the Fed can do about current or backward inflation. The lagging effects of tightening could coincide with tighter fiscal policy as the BBB’s effects wane. Upon reading Waller’s full speech—and not just the hawkish headlines that dominated newswire pick up—I found he flip flopped back and forth in a way that makes his view on appropriate policy action much less clear than the headlines suggested. We could also ask why a candidate for Chair made such a speech the day before Chair Warsh’s Congressional testimony this morning. See my weekly for a further dive into the cautions against policy tightening.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.