ON DECK FOR MONDAY, JULY 13th

KEY POINTS:

- Oil edges higher after weekend fighting

- Don’t judge the week by today’s light developments

- Fed’s Waller on tap

- The Canada-US bridge deal could hurt future agreements

- Fresh maintenance round of forecasts from the Economics and FX Strategy teams

- Global Week Ahead—Double Jeopardy

Don’t judge the rest of this week’s market action by what you are seeing today. This is a bland start to a packed week, particularly in Canada with the BoC on Wednesday, and the US with CPI, Q2 earnings focused upon financials, and two rounds of testimony by Chair Warsh on tap.

For now, it’s a bit of the same pattern coming out of past weekends. The US and Iran spent the weekend attacking each other, oil moves up, bonds cheapen, and we remain on the slow grind toward a collapsed US-Iran MOU that any sensible person saw as one-sided and unsustainable while missing vital elements.

Oil prices are up by over a couple of bucks this morning. Sovereign bond yields are slightly higher everywhere. US equity futures are down by about ¼% (S&P) to 1% (Nasdaq) while TSX futures are flat, European cash markets are mixed and Asia-Pacific markets were mostly in the red and led by another 9% plunge by the Kospi. Currencies are mixed between small gains and losses to the USD among the majors.

Today’s calendar is very light. Fed Governor Waller speakers at 12:30pmET with text and moderated Q&A. Governor Bowman spoke on regulatory issues this morning.

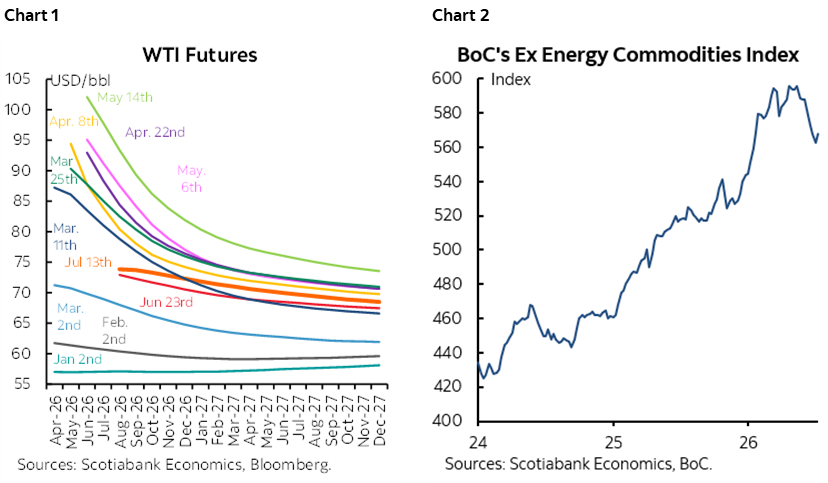

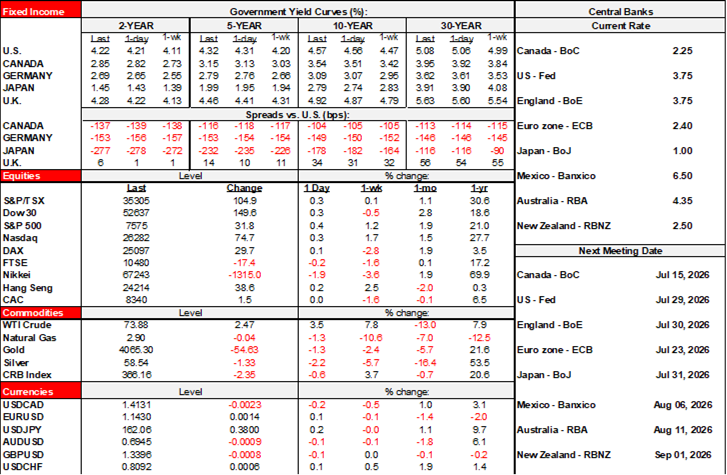

The world has changed a great deal since the BoC entered the year. WTI and Brent remain about US$17/barrel higher than at the start of the year and higher throughout the futures curve (chart 1) while multiple other commodity prices remain higher as indicated by the BoC’s commodity price index ex-energy that is off the peak but still much higher (chart 2). USDCAD is materially higher with CAD about 6–7 cents appreciated from the year’s low. Jobs are on the mend with gains in three of the past four months after falling three out of four to start the year with some overlap. The economy is rebounding. Trade remains an overstated risk. More fiscal policy stimulus was added at the end of April. Pre-war inflation drivers remain intact. And so forth. My full preview of this week’s decision, forecasts and broader communications is available in the Global Week Ahead.

Hooray, the new Gordie Howe bridge between Canada and the US will open on July 27th after a weekend deal between the US and Canada to address the Trump administration’s sudden refusal to allow it to open. That’s a plus for Commerce. It’s bad for credibility, faith in contracts and a system of law and order, the viability of making long-term deals with the US, and democracy. It’s blatantly unfair and commingles donor politics with commerce once again. Canadians have a right to know the full details, like was the Moroun family paid off somehow in the murky language of shared proceeds? Canada built the bridge, financed the bridge, and both the US and Canada signed the initial agreement stipulating that Canada would collect tolls until the investment was paid off after the US refused to chip in but Michigan welcomed the initiative. Years later, the US signature on the agreement is worthless—yet again—as the US demands a portion of the proceeds on an investment it never made and all seemingly prompted by the Moroun family that inherited a competing, aging, technologically obsolete bridge. Perhaps Canada’s willingness to pay a bribe was the correct thing to do in the short-term, but signing long-term deals with the US on anything has suffered an additional blow. Remember that on trade.

And as a reminder, please see the Global Week Ahead—Double Jeopardy that was sent on Friday (reminder here). Key topics include:

- BoC to wish everyone a pleasant summer as pressure builds

- Fed Chair Warsh to deliver two rounds of Congressional testimony

- Why Fed hikes could be policy error…

- …that risk putting its independence back on trial…

- …while imperiling what the taskforces could achieve

- US CPI and PPI to inform the Fed’s preferred inflation gauge…

- …and watch super-supercore CPI

- US Q2 earnings season begins in earnest

- BoK expected to hike

- China’s economy to post subdued GDP growth

- Global macro — US retail, light Canadian releases, UK data dump, Indian CPI

Lastly, we put out fresh macro forecasts this morning. They’re the same, only different, in what can be billed as a maintenance round with contributions from across all of the entire Economics and FX Strategy team members throughout the Americas which is our shop’s mandated focus. On rates, I pushed out the Fed cut call a bit to early next year from December, left the BoC call at -75bps over Q4/Q1, and Canada-US yield curves were tweaked as forecasts have generally been performing well.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.