ON DECK FOR FRIDAY, JULY 10th

KEY POINTS:

- Markets playing it safe ahead of a packed week

- Canadian jobs the last set up before the BoC

- NOK slips, Norges hike pricing reined in after CPI softens

The week is ending with much of the focus upon expectations for next week’s developments especially on Tuesday morning when US CPI, Chair Warsh’s testimony, and US bank earnings hit within the space of about 4–5 hours. Analysts have been firming up their earnings calls into the start of the Q2 season. Otherwise, the day’s focus will include Canadian jobs, perpetual negotiations and tension in the Middle East, and other light developments.

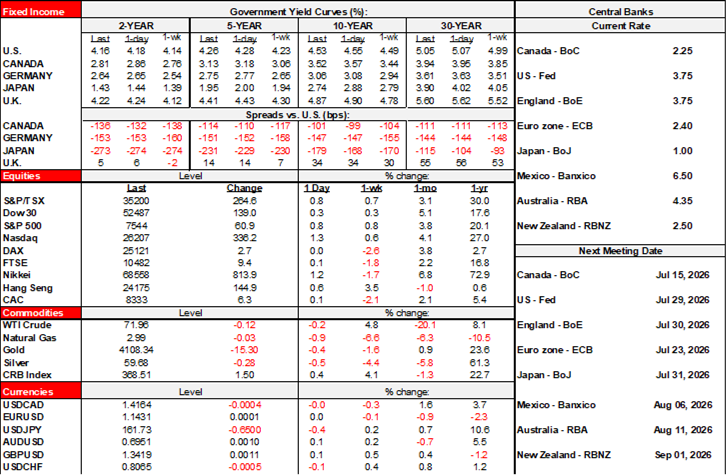

Sovereign bonds are slightly richer across major markets with Norway’s curve outperforming all others on a bull steepener move post-CPI that surprised lower (2.7% y/y, 3.1% prior and consensus) and turned pricing for the August decision by Norges into a coin flip. The dollar is little changed except for modest gains by the yen and NZ$ and a weaker NOK post CPI. Stocks are highly mixed around small gains and losses.

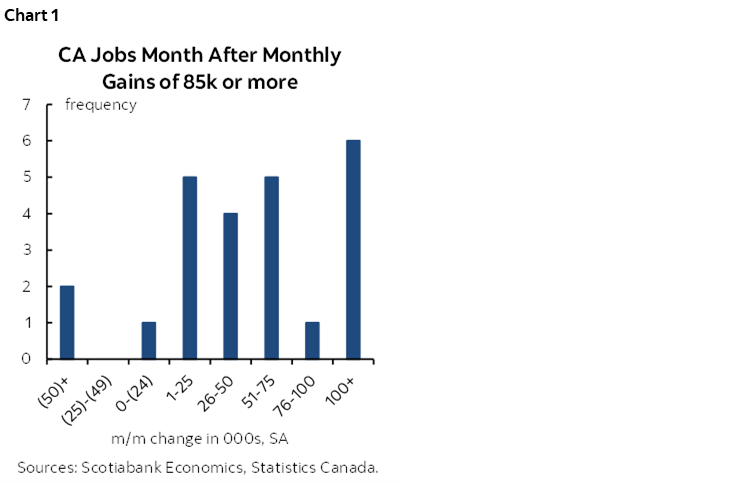

Canadian Jobs Will Segue to Next Week’s BoC

The main macro focus of Canadian market participants will be the Labour Force Survey for June (8:30amET). My guesstimate is a repeat gain of 10k that was submitted before knowing consensus would land at the same median number.

The range of estimates runs from 0k to 35k with an average of 12k. There is no real clustering of estimates within the range.

The unemployment rate is widely expected to hold around 6.6%.

Historically when Canada posts a large gain as it did in May (88k), the next month tends to be higher (chart 1). One reason is the LFS methodology that uses a rotating panel sample in which the same survey dwellings remain in the sample for six consecutive months with the first month dropping out as a new month’s sample is added. This can drive persistence in the readings because most of the same folks are being asked.

Other arguments behind the estimate were provided in last week’s weekly.

Also watch hours worked that are tracking a mild Q2 gain in support of rebounding GDP. A challenge to the hours figure is tha the prior month’s huge rise in full-time jobs (154k) and drop in part-time (-66k) may swap places this time in a manner that weighs on hours.

Wage growth may struggle to remain positive in m/m terms after the prior month’s large gain.

And then there are the usual reminders. It’s a wonky survey with sky-high statistical noise. The 95% confidence interval around estimated changes in employment is +/-57k. You could spin the CN Tower sideways and still fit it through such a range. Its noise factor is akin to the US household survey. Unfortunately, Canada’s payrolls survey is no better as it a) lags, and b) unlike the LFS, it is revised each month and very often by tens of thousands of jobs every time, thereby destroying any notion that payroll data is higher quality in Canada. Onto the mopping up.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.