ON DECK FOR FRIDAY, JANUARY 9TH

KEY POINTS:

- Global markets await payrolls, potential SCOTUS decision

- Nonfarm payrolls—overstated & unreliable, whatever happens

- Canadian jobs: pushing their luck for four in a row?

- SCOTUS IEEPA tariff decision could come today

- Why bribing Greenlanders could hilariously backfire

- Treasuries shake off Trump’s MBS announcement

Ready for some fabricated, totally made-up and arbitrary numbers that may well settle absolutely nothing? Welllll, step right up, we’ve got nonfarm payrolls coming up for you this morning. Canada also releases jobs, also for December and that also has its own set of issues. Previews for both were in my weekly. We might also get the SCOTUS IEEPA tariff decision this morning which has the potential to matter more.

Markets are driving slight USD strength into the numbers. US Ts are mildly cheaper across the curve as they rightly shake off Trump’s pledge to fleece Fannie/Freddie cash to buy US$200B of MBS which is a) modest in relation to about US$9T of outstanding agency mortgage bonds, b) not a net injection of cash into the financial system so can the QE talk, and c) a one-off, likely to be met by other investors reacting and quickly moving on. Equities are slightly higher with next week’s start to the Q4 and full year earnings season arguably more important than payrolls.

Overnight developments were very light and mostly constructive. BCRP held at a policy rate of 4.25% as widely expected. Germany registered solid growth in factory output in November (+0.8% m/m, consensus -0.7% with upward revisions) to back up the previous day’s strong factory orders, but exports fell 2.5% m/m (-0.2% consensus). French consumers spent less in November (-0.3% m/m) partly because of a small upward revision to a 0.5% gain in October. Spanish factories are doing rather well, with output up 1.0% m/m in November (-0.4% consensus) for a third straight gain.

NONFARM PAYROLLS — OVERSTATED & UNRELIABLE, WHATEVER HAPPENS

A batch of job readings for December land at 8:30amET. Consensus is at 70k for nonfarm payrolls with Scotia at 25k. The 90% confidence interval is within +/-136k and so pretty much all estimates are within the noise bands.

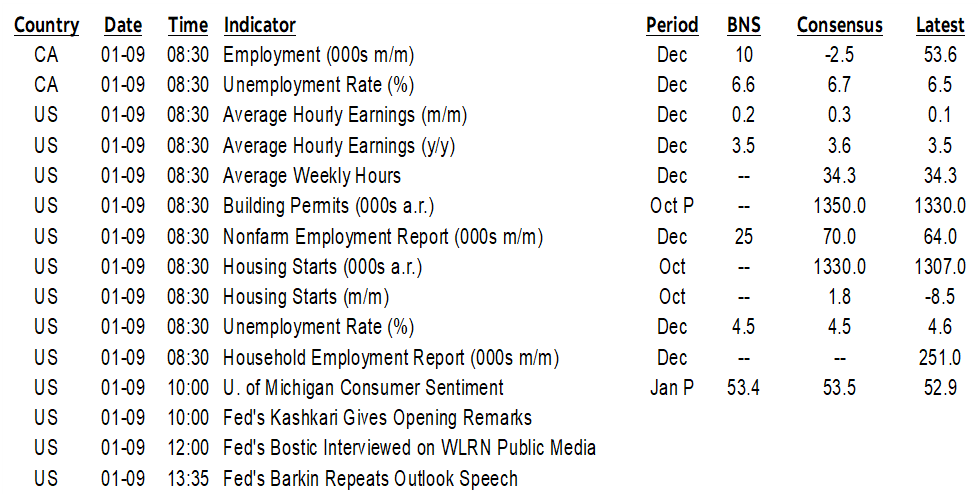

Details will matter enormously once again as we’ll have to dissect and examine things under the hood very carefully. Chart 1 is one example in that if we take health care out, then private sector jobs have fallen in four of the past six months and were flat in another.

Most alternative readings suggest something within this range, but nonfarm is it’s own beast. ADP private payrolls were up by 41k. Revelio’s measure posted a 71k gain. JOLTS job openings fell sharply with downward revisions. Challenger layoffs were at 35.6k. Consumer confidence jobs plentiful fell to the lowest reading since June, signalling less availability of jobs. Initial jobless claims have been reasonably well behaved while continuing claims have recently trended lower and point to a correlated dip in the unemployment rate.

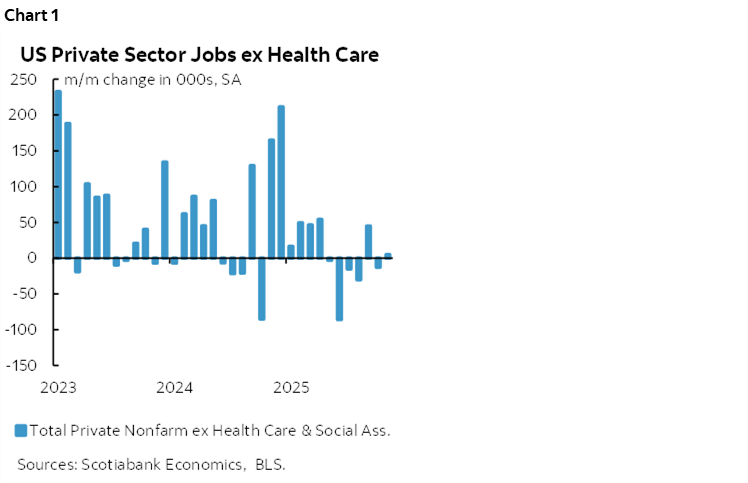

December is normally a down-month for seasonally unadjusted payrolls. What happens next depends upon how the BLS manages seasonal adjustments. In each of the three prior reports they have gone with historical all-time highs for monthly seasonal adjustment factors when comparing like months across time. If they do the same thing this time, then that could add some upside. Chart 2 shows scenarios for payrolls across differing seasonal adjustment factors and seasonally unadjusted readings.

And yet the arguments for how nonfarm payrolls are much weaker under the hood are likely to still apply. They were explained in my prior recap for payrolls (here). Take out healthcare hiring and private payrolls have been down or flat in six of the past seven months and healthcare hiring is vulnerable as subsidies expire. Adjust for benchmarking revisions that have yet to be incorporated and payroll levels are much lower by just under a million up to last March and by more since then. Adjust for fishy seasonal adjustment factors that went high in each of the three months since Trump started attacking the BLS after firing its Commissioner. We’re getting low quality jobs data out of the US for these reasons plus others like falling survey response rates.

The US will also refresh estimates for housing starts in October (8:30amET) and the University of Michigan’s consumer sentiment reading for January (10amET).

CANADA TO REFRESHES JOB MARKET ESTIMATES

Canada also updates jobs and related measures for the month of December on Friday at the exact same time as nonfarm payrolls (8:30amET).

Consensus is at -2.5k with estimates scattered from -16.3k from folks who clearly have a sense of humour in going beyond the decimal point, to +10k where I am. It’s a spin of the wheel for a noisy survey with a 95% confidence band of +/-57k around the estimates.

And whoop-de-doo. The BoC is clearly on an extended pause as it evaluates a material amount of data and new developments after cutting down to a real policy rate that is about zero or even negative, depending on the measure of inflation or inflation expectations that is used. After a string of massive employment gains, one report won’t sway them which leaves us with bi-directional trading noise but probably no direct policy implications.

Job growth has been running at a torrid pace over the past three months with gains of over 50k m/m in each of them. For two of those reports we’ve been hearing the next one must surely be down by a lot. Not. Yet there is the same hubris across consensus estimates now; maybe they’ll be right this time. Maybe not.

Historically, however, a trifecta of monthly gains over 50k has always been followed by….wait for it….another gain! Mind you, out of eight such occasions in the history of the Labour Force Survey, only two have been outside of the pandemic period.

Another reason for another possible gain is the LFS methodology’s practice of rotating out new household responses one month at a time over a rolling six-month period. The first month’s respondents get dropped and new respondents are added for the latest month. This heavily weights the survey to the same panel of respondents which can at times drive persistence.

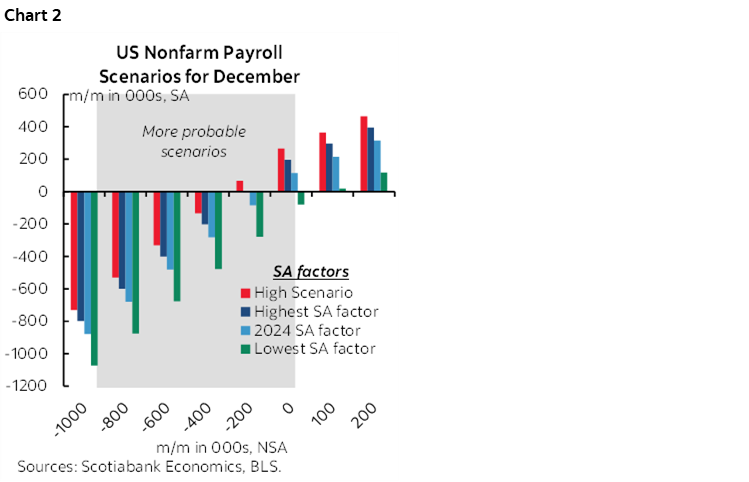

But it’s not all about technical excuses. Seasonally adjusted job postings have been on fire as marked by a steep upward trend since September that held in at high levels in December (chart 3).

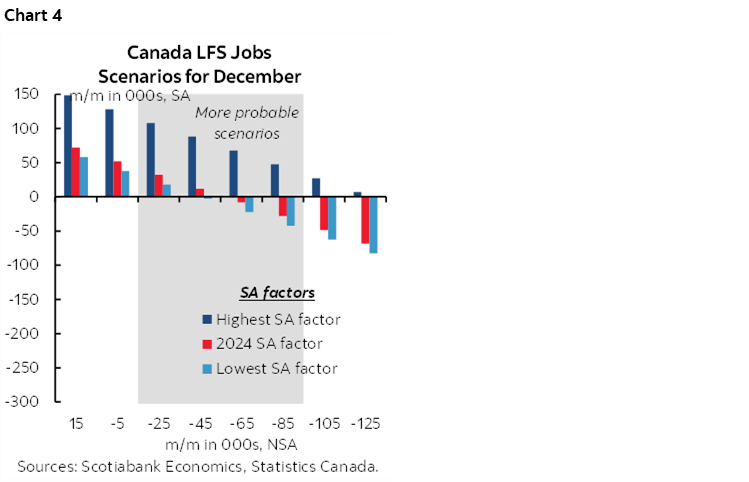

A further argument is that December is normally a seasonal down-month for employment with the sole exception being last December. Chart 4 shows scenarios around seasonally unadjusted changes married to varying seasonal adjustment factors. The pandemic and post-pandemic error has tended to employ lower than average SA factors for months of December which may tamp down the estimated change in jobs.

Also keep an eye on potential weather effects that may have to be considered for December and thereafter. Flooding in BC might be impactful in which case we would have to control for this effect under the hood. So may be the earlier and broader than normal flu season.

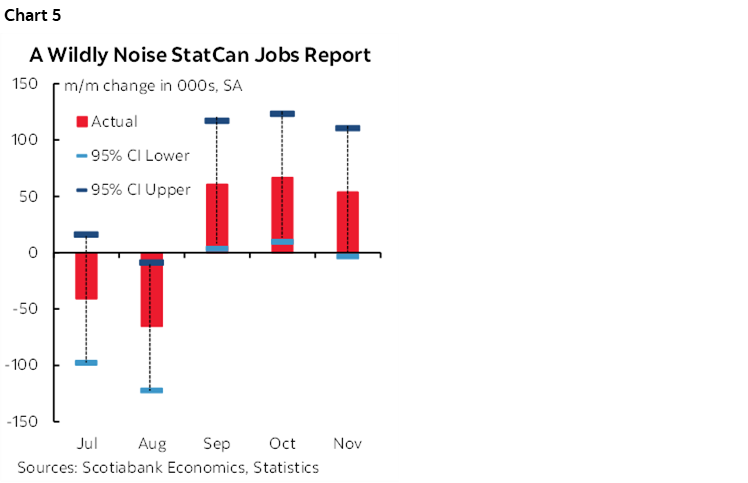

In any event, while it’s a noisy survey, one cannot credibly dismiss the three strong consecutive gains given the 95% confidence bands around their estimates would still have posted a positive trend and maybe even a much more positive one at that (chart 5).

SCOTUS IEEPA DECISION COULD LAND TODAY

It’s also possible that we get the SCOTUS IEEPA tariff ruling as soon as today when the Supreme Court is in session. The Court convenes at 10amET which is when they announce opinions. Ergo, if today is the day, then nonfarm fireworks—if any—could be followed by IEEPA reactions 90+ minutes afterward. Monday to Wednesday in each of next week and the week after are argument days and could also result in the announcement of a decision, or SCOTUS could insert another opinion day somewhere along the way. Get on with it! Then watch for the reactions by Trump including potential policy substitutes announced on the fly on social media.

WHY BRIBING GREENLANDERS WOULD HILARIOUSLY BACKFIRE

News reports indicated that the Trump administration is considering sending large payments to residents of Greenland to, well, bribe them into joining the US. The payments are thought to be in the US$10k–100k range per Greenlander. Given there are about 57,000 Greenlanders, the tally would be anywhere between over US$500 million up to just under $6 billion.

Except it won’t work. My instant reaction with staff and clients yesterday was to chuckle. Denmark would very reasonably see this for what it is—a blatant attempt at interfering with domestic politics. It could counter such a measure by announcing a 100% special levy on the proceeds upon receipt.

In that case, Denmark’s PM Mette Frederiksen could very well pen a kind letter of gratitude to President Trump on the Kingdom of Denmark’s letterhead that would go something like “Dear Don, thanks for filling our coffers. Please send more, looking forward to being debt free. Your pal, Mette.”

And that’s without considering the vulgarity behind thinking nationhood can be bought with bribe money, let alone what American taxpayers would think. Still, by most highly uncertain costing estimates, even $6B would be trying to buy Greenland on the cheap.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.